Why Are Hazardous Materials Transport Claims Denied?

——Real Cases, Hidden Pitfalls, and How to Get Paid Without Disputes

By Jonathan Carter | Updated on March 24, 2026 | 🕓18–22 minutes

Key Highlights

- Real-world hazardous materials transport incidents: success vs. failure

- Analysis of why insurance claims are denied

- Common pitfalls: policy clauses, disclosure, operational compliance

- Jurisdictional differences: USA vs. Canada vs. Europe

- Best practices for claim success

- High-risk profiles for denied claims

- Required documentation and contact points for claims

A tanker transporting gasoline overturned on a highway in northern New York State.

The cargo value wasn’t high—about 4,300 gallons of gasoline and diesel. But the fuel leaked into a nearby reservoir, contaminating the local drinking water supply. Local environmental authorities intervened and mandated cleanup. The final bill: nearly $3 million in environmental remediation costs.

The insurance company denied the claim.

Reason: “Total pollution exclusion clause.”

This is not a fictional cautionary tale. It is a real case that happened in North Salem, New York, in 2019, involving a Performance Trans tanker overturn. Cleanup costs have reached nearly $3 million to date, and the dispute over insurance coverage went all the way to the U.S. First Circuit Court of Appeals.

The problem wasn’t the severity of the accident itself but a gray area between a single “exclusion clause” and a “special hazards endorsement” in the policy that determined who would ultimately bear nearly $3 million in costs.

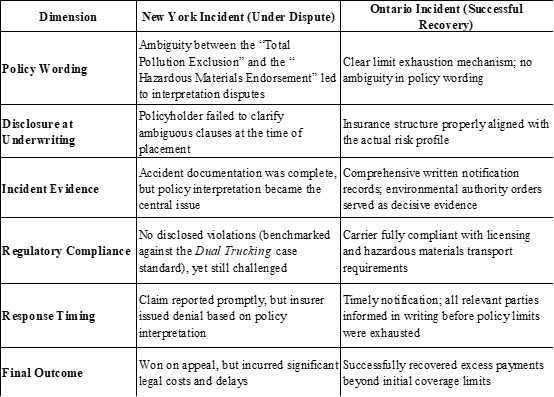

1: Two Cases, Two Outcomes

Case 1 – Failed Case: North Salem, New York Tanker Overturn

Cargo transported: Gasoline and diesel (approx. 4,300 gallons), UN 1202/UN 1203, flammable liquids Class 3

Accident details: On February 19, 2019, a Performance Trans tanker overturned while traveling in North Salem, New York. About 4,300 gallons of gasoline and diesel leaked onto the roadway and into a nearby reservoir, causing severe environmental pollution.

Insurance coverage:

Primary coverage: Utica Mutual, limit approx. $1 million

Excess coverage: General Star (subsidiary of Gen Re), limit $5 million

Denial logic:

When cleanup costs exceeded the $1 million primary policy limit, Performance Trans filed a claim with General Star’s excess coverage. General Star denied the claim, citing the “total pollution exclusion” clause in the policy.

Performance Trans argued that the excess policy contained a “special hazards endorsement,” which should cover such an accident.

Court ruling:

District Court (trial level): Supported General Star, holding that the policy was unambiguous and the exclusion applied

First Circuit Court of Appeals: Reversed the trial court, finding that the “special hazards endorsement” was ambiguous, with at least three reasonable interpretations

The appellate court noted: “Massachusetts law clearly states that when two reasonable interpretations of a policy exist, any ambiguity must be resolved in favor of the insured.”

Final loss:

Cleanup costs: nearly $3 million (at the time of judgment)

Legal costs: years of litigation

Time cost: accident occurred in 2019, appellate ruling issued in December 2020

Mistakes made:

1. Insufficient understanding of policy clauses: ambiguity between the “special hazards endorsement” and the “total pollution exclusion” was not clarified at the time of purchase

2. Insurance coverage gap: primary coverage ($1 million) was clearly insufficient relative to actual risk

3. Reliance on post-fact judicial remedy: although they ultimately won on appeal, it consumed significant time and legal costs

Case 2 – Successful Case: Formaldehyde Tanker Overturn, Ontario, Canada

Cargo transported: Liquid formaldehyde (approx. 30,000 liters), classified as a pollutant

Accident details: In May 2012, a Transport Donia Banville tanker overturned near North Bay, Ontario, Canada. About 30,000 liters of liquid formaldehyde leaked into a residential area and municipal drinking water supply system.

Insurance coverage:

Intact Insurance covered Transport Donia Banville with a $5 million liability limit

Zurich insured the cargo owners (ARC Resins, Tembec) and the transportation arranger (G3)

Key to successful claim:

After the accident, Intact, as the carrier’s insurer, immediately intervened and began paying cleanup costs. When costs approached the $5 million limit, Intact repeatedly notified Zurich in writing between July and September 2012, indicating that coverage was nearly exhausted and Zurich should assume payment for further cleanup costs.

Zurich initially refused, claiming that its insured had not received a mandatory cleanup order from the Minister of the Environment.

Intact continued paying, and total costs eventually reached approx. CAD 7.96 million—about CAD 2.96 million above its policy limit.

In May 2014, Ontario’s Ministry of the Environment issued a mandatory order, declaring all parties involved (carrier, cargo owners, consignees, transport arrangers) in violation of Section 93 of the Environmental Protection Act regarding cleanup obligations. Zurich then began paying cleanup costs on behalf of its insured.

Claim outcome:

Intact sued Zurich and other parties to recover the CAD 2.96 million excess. Although the case is still procedurally ongoing, the key success factors are clear:

1. Complete evidence chain: Intact retained all written notifications showing timely warning to other responsible parties before policy limits were exhausted

2. Clear regulatory intervention: the mandatory order became critical evidence in allocating responsibility

3. Multi-party liability: under Ontario’s Environmental Protection Act, both “persons with control over the pollutant” and “owners of the pollutant” share cleanup obligations—meaning the carrier was not solely responsible

Reasons for success:

1. Timely reporting and notification: immediate reporting and repeated written warnings before coverage limit exhaustion

2. Clear statutory liability framework: Ontario law explicitly provides shared cleanup responsibility

3. Maintaining complete communication records: all notifications documented in writing

2: Comparative Analysis — What Made the Difference

3: Insurance Company “Audit Logic” — What They Actually Look At

3.1 First question: Does it fall within the “covered risk”?

Insurance companies first confirm whether the policy type covers the accident.

Standard cargo insurance does not cover hazardous materials risks. U.S. FMCSA requires minimum liability limits of $5 million for high-risk hazardous materials (e.g., Division 1.1, 1.2, 1.3 explosives; Division 2.3 Zone A toxic gases). Ordinary auto insurance limits in California DMV (30k/60k/15k USD) are not applicable for commercial hazmat transport.

Importance of the special hazards endorsement: The New York dispute centered on whether it covered pollution losses. Without this endorsement at the time of purchase, General Star’s denial may never have escalated to litigation, as it would not have been within coverage in the first place.

3.2 Second question: Were policy conditions violated?

This is a high-risk area for denials. Insurers will examine:

Truthfulness of application:

Was the insured fully disclosing prior violations?

Were any environmental warning letters concealed?

Were statements on the application “materially” accurate?

Dual Trucking case caution: In July 2012, Dual Trucking leased land in Montana for operations. The state’s environmental agency received a complaint alleging unauthorized disposal of oil and gas exploration waste. A warning required them to hire an environmental consultant and plan cleanup within 15 days.

In October 2012 and October 2013, Dual Trucking applied for two environmental liability policies from Admiral Insurance, failing to disclose the warning letter. Later, multiple violation notices were issued, but the insured did not amend the policy application.

Outcome: Admiral Insurance had no obligation to pay, as the policy had been voided for misrepresentation, even though the accident itself was unrelated.

Key takeaway: Concealing any information the insurer would consider material can void the entire policy, even if unrelated to the accident.

3.3 Third question: Does a pollution exclusion apply?

This is the most specialized denial check for hazardous materials transport. Almost all standard liability policies contain pollution exclusions.

Burroughs Diesel case: On October 14, 2016, over 5,000 gallons of hydrochloric acid leaked in Laurel, Mississippi. Acid formed a mist cloud, damaging buildings, vehicles, inventory, and equipment. Travelers denied the claim citing the pollution exclusion. Burroughs argued the exclusion did not cover “smoke” damage.

The Fifth Circuit disagreed, stating that “smoke” in ordinary meaning refers to gaseous byproducts of combustion. Acid mist was not considered smoke. Pollution exclusion applied; Travelers was not liable.

Key conclusion: Pollution exclusions are the most common denial reason in hazardous materials claims. Policies must explicitly state what pollution risks are excluded and what exceptions exist. Do not assume any accident is automatically covered.

3.4 Fourth question: Was there gross negligence?

In the Ontario formaldehyde case, courts noted the accident resulted from the carrier’s negligence but did not constitute gross negligence.

Distinction:

Ordinary negligence: driver misjudgment causing overturn → typically covered

Gross negligence: knowingly operating a damaged tanker, unqualified driver, misclassifying cargo → triggers exclusion

4: Denial Trigger Checklist — What Insurers Focus On

High-risk factors based on cases and industry practice:

4.1 Application-related (most fatal)

Failure to disclose prior violations → policy voided, all claims denied

Failure to disclose environmental warning letters → policy voided

False answers regarding compliance → policy voided

Concealing known pollution → policy voided

4.2 Policy clauses

Pollution exclusion applied (Burroughs Diesel)

Ambiguity between “total pollution exclusion” and endorsements (Performance Trans) → litigation needed

No pollution liability coverage → environment cleanup costs self-paid

4.3 Operational compliance

Driver lacks Hazmat CDL → federal violation, denial risk

FMCSA hazmat regulations not followed → triggers exclusions

Incorrect hazardous materials classification → policy may be invalid

4.4 Evidence

Late reporting → denial or partial payout

No official accident report or on-site photos/videos → difficult proof

Cleanup costs not approved by insurer → denial or partial payment

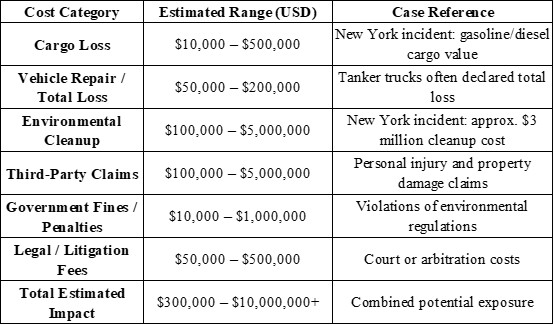

5: Cost Breakdown — How Much Does a Hazardous Materials Accident Really Cost?

Typical tanker overturn & spill accident costs:

New York real case:

Cleanup cost: ~$3 million

Primary coverage: $1 million

Coverage gap: ~$2 million (core dispute with excess insurer)

Ontario real case:

Cleanup cost: ~$7.96 million CAD

Primary coverage: $5 million CAD

Excess payment: $2.96 million CAD (carrier insurer paid first, then recovered from other responsible parties)

6: Cross-Border Differences — U.S. vs. Canada vs. Europe

U.S. (DOT/EPA framework)

Regulatory strength: federal + state; FMCSA sets minimum liability $0.75–5 million

Key differences: strict disclosure obligations; failure to disclose environmental warning can void policy (Dual Trucking)

Pollution exclusion: almost universal, courts tend to uphold (Burroughs Diesel)

Claims timeline: 2–8 months; litigation can take years

Canada (provincial environmental law framework)

Regulatory framework: provincial Environmental Protection Acts, shared cleanup responsibility

Key differences: Section 93 of Ontario Act explicitly shares liability among owners, carriers, and consignees

Multi-party recovery: carrier insurers can recover excess payments from cargo owners or arrangers

Claims timeline: 3–12 months, longer if liability complex

Europe (ADR framework)

Regulatory strength: very high; ADR imposes uniform standards on vehicles, packaging, drivers, routes

Tunnel restrictions: vehicles may be prohibited from tunnels depending on cargo hazard class; insurer may disclaim coverage if violated

Environmental liability: EU Environmental Liability Directive requires “polluter pays,” cleanup costs potentially unlimited

Claims timeline: 3–6 months; multi-country coordination may extend timeline

Realistic claims timelines:

Simple single-party accident: 2–4 weeks

Environmental pollution: 3–12 months

Multi-party injury/litigation: 1–5 years

7: What Could Have Changed the Outcome

Looking at New York and Ontario cases, clear action guidelines emerge:

If New York’s Performance Trans had done the following:

At purchase:

1. Request written clarification: does “special hazards endorsement” cover pollution?

2. If ambiguous, demand explicit wording covering pollution in the policy

3. Increase primary coverage from $1 million to a risk-matched level (e.g., $5 million)

After accident:

1. Seek legal advice immediately if excess insurer denies claim

2. Keep all communication records with insurers

Expected outcome: Ambiguities may have been removed at purchase stage or resolved faster after denial.

What Ontario did right:

At purchase:

Intact’s carrier policy fully covered risks

After accident:

Immediate intervention and cleanup payments

Written notification to all other responsible parties before policy limits exhausted

Maintain complete communication record

Use Ministry’s mandatory order as key evidence for liability allocation

Core success factors:

Written notifications: multiple written alerts to Zurich before limit exhaustion, forming evidence chain

Statutory liability framework: Ontario law clearly shares responsibility

Regulatory backing: mandatory order served as authoritative proof

Insight: Even if carrier is the primary responsible party, cargo owners, consignees, and transport arrangers may share cleanup responsibility. Key is written evidence and regulatory endorsement.

8: Who Is Most Likely to Be Denied? Which Mistakes Are Fatal?

Highest-risk groups:

1. “Selective amnesia” insureds: forget to disclose prior violations, warnings, or environmental issues. Dual Trucking shows this is the deadliest error → policy void

2. “Ambiguous clause tolerance” insureds: accept vague exclusions or endorsements without clarification. Core issue in New York case

3. “Underinsured” insureds: primary coverage far below potential risk. NY case: $1M vs. $3M cleanup cost

4. “Post-fact handler” carriers: do not report promptly, do not keep evidence, attempt private settlement → catastrophic in hazardous materials transport

9: Key Documents & Contacts for International Hazardous Materials Claims

Required when reporting:

Insured name

Policy number

Insured contact (name, phone, email)

Vehicle year, brand, last 6 digits of VIN

Claimant name & phone

Accident description

Special emergency cases: For pollution emergencies, report simultaneously to dedicated response centers (e.g., Spill Center).

Key documents checklist:

Material Safety Data Sheet (MSDS/SDS)

Transport documents (Bill of Lading)

Official accident reports (police/environment agency)

Driver Hazmat CDL

Vehicle inspection & compliance certificates

Cleanup invoices and contracts

Conclusion

Hazardous materials transport claims are rarely denied because of the accident itself — they are denied because risk was misrepresented or policy ambiguities were not clarified beforehand.

In hazardous materials transport, compliance is not a cost—it is the only passport to insurance recovery. And compliance begins with the very first question on the insurance application.

References

1. Land Line Media. (2021). Dual Trucking withheld information, taking insurer off the hook for hazmat violation

2. Freberg Environmental. (2025). Claims – Hazardous Materials and Waste Hauler Claims Reporting

3. Courthouse News Service. (2017). Insurer Doesn’t Have to Cover Wastewater Company’s Explosion

4. Court of Appeal for Ontario. (2022). Intact Insurance Company v. Zurich Insurance Company Ltd., 2022 ONCA 485

5. SoCal Truck Insurance. (2026). How Commercial Truck Insurance Requirements Change By Cargo Type

6. Business Insurance. (2020). Gen Re loses pollution dispute with trucker

7. RT Specialty. (2020). Travelers unit wins pollution ruling against trucking firm

About the Author:

Jonathan Carter

Jonathan Carter is a logistics risk management consultant and insurance analyst with over 12 years of experience in hazardous materials transport and commercial insurance. He has worked with multinational transport companies to optimize insurance coverage and risk mitigation strategies.

Additional credentials: Member of the Chartered Insurance Institute (CII, UK), frequent contributor to transport and insurance journals.

Editorial Transparency Statement:

This article is provided for informational and educational purposes only. The content reflects verified case studies, legal precedents, and industry practices. The author and publisher have no commercial affiliation with insurance providers, and the article does not constitute insurance advice or solicitation. Readers should consult their own insurance professionals for specific guidance.

Disclaimers:

All information for reference only and does not offer, advertise, or sell insurance products.

The content is not a substitute for professional advice. Always consult a licensed insurance advisor or legal professional for guidance specific to your situation.

Laws, regulations, and insurance requirements vary by jurisdiction and may change over time.

Recommended for you