How to Choose Cost-Effective Auto Insurance for Daily Commuting in the City

——Smart Ways to Handle Minor Accidents, Speed Up Claims During Rush Hour, and Understand Typical Payout Timelines

By Emma Lawrence | Updated on March 24, 2026 | 🕓12 minutes

Key Highlights

- Choose the right insurance to save money on daily commuting.

- Must-have coverage includes liability and UM/UIM; optional coverage depends on car value.

- Use apps, partner repair shops, and your own insurance for fast claims.

How can city commuters choose auto insurance to save on premiums? What should you pay attention to when filing claims for minor accidents during your commute? How can you speed up claims in rush hour traffic? How long does a typical commuter accident claim take?

At 8 a.m., you are waiting at an intersection for the green light. The car in front suddenly brakes, and you lightly rear-end it. The surrounding traffic is dense, the signals are complicated, and the situation is disputed. You take out your phone but aren’t sure whether to report the accident immediately or whether the claims process will be complicated.

Global traffic data shows that about 70% of minor city traffic accidents occur during rush hours, often involving low-speed rear-end collisions, scrapes, and backing accidents. For commuters, choosing the right insurance, protecting yourself in minor accidents, and minimizing claims processing time are real concerns.

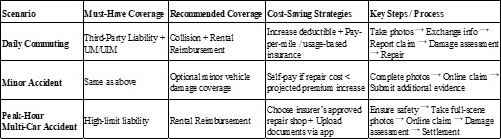

Part One: How to Choose Commuter Auto Insurance to Actually Save Money

The logic for urban commuting insurance differs from occasional driving. Commuting is characterized by: high frequency, low speed, complex traffic conditions, high probability of accidents but small individual losses.

1.1 Insurance Types Explained: Must-Have vs. Optional

Must-Have 1: Liability Insurance — Coverage Should Be High

Liability insurance covers bodily injury and property damage you cause to others and is mandatory in all regions. During rush hour, with dense traffic, a multi-car rear-end or injury accident can quickly exceed basic coverage limits.

Recommendations:

- U.S. market: $500,000–$1,000,000 minimum

- European market: €5–10 million (Liability coverage is generally higher)

- Asia-Pacific market: 1–2 million in local currency

Why high liability coverage for commuting?

Accidents often happen during commuting. If someone is injured, medical expenses, lost wages, and emotional damages can accumulate rapidly.

Must-Have 2: Uninsured/Underinsured Motorist (UM/UIM) Insurance

Many city vehicles are uninsured or underinsured. If the other party is fully at fault but has no insurance, this coverage pays for your losses. UM/UIM is particularly essential in North American urban commuting but less necessary in Europe and Asia, where comprehensive insurance or government-mandated coverage may suffice.

Recommended 3: Collision Insurance

Covers repair costs for your own vehicle. In city commuting, low-speed rear-end collisions and scrapes are the most common accidents. Without collision coverage, you bear the repair costs yourself.

Recommended 4: Rental Reimbursement

Commuting is a necessity. If your car is in the shop and you lack an alternative, daily taxi or rental costs add up. Rental reimbursement usually covers $30–50/day to offset these costs.

Recommended 5: Short-Route Commuting Protection

For fixed daily routes, this covers economic losses due to vehicle damage delaying work. Primarily available in North America, rare in Europe, and almost nonexistent as a standalone product in Asia/China. To indirectly cover commuting delays, combine collision insurance + rental reimbursement + car hire coverage.

Optional 1: Minor Damage Insurance (for older cars)

If your vehicle’s market value is low (e.g., under $5,000), collision insurance premiums may approach or exceed vehicle value. In this case, consider self-retaining the risk and dropping collision coverage to significantly reduce premiums.

Optional 2: Scratch, Glass, and Other Add-ons

High claim thresholds, significant premiums, and minor claims may affect future premiums. Commuters should focus on “major risk protection” rather than minor damage coverage.

1.2 Three Practical Ways to Save More

Tip 1: Pay-Per-Mile Insurance (PAYD) — A Commuter’s Friend

If annual mileage is low (e.g., under 10,000 miles / 16,000 km), consider PAYD. Policies track mileage via telematics or apps; drive less, pay less.

- North America: Metromile, Allstate Milewise, etc.

- Europe: Some insurers offer telematics-based mileage plans.

- Best for: Fixed 5-day weekly commuters with low total mileage and stable driving habits.

Industry data: PAYD can save low-mileage drivers 20–40% on premiums.

Tip 2: Increase Deductibles

Deductible = portion of costs you pay. Raising deductible from $250 to $500–$1,000 can reduce premiums 10–20%.

Caution: Don’t exceed what you can afford to pay easily without affecting cash flow.

Tip 3: Bundling & Discounts

Bundling car insurance with homeowners or renters insurance often yields 15–25% multi-policy discounts. Multi-car, safe-driving, prepayment, and automatic debit discounts can stack. Most discounts multiply, not add. Example: $2,400 premium → 20% × 10% = 28% savings, not 30%. Proper stacking can yield 30–50% total savings.

Local insurance usually enables faster claims and better access to local discounts. Comparing policies every 1–2 years is a universal global cost-saving strategy.

Part Two: Minor Accidents During Your Commute — Three Key Claims Tips

2.1 Case: Claim Denied for Not Photographing Registration

Mr. B was rear-ended during morning rush. The other driver was cooperative, and Mr. B thought a simple phone photo and exchanged numbers were enough. Next day, the other driver claimed, “You backed into me.” The insurer required the other party’s registration and license info, which Mr. B didn’t have. Initial claim denied, took two weeks and repeated follow-ups to retrieve compensation.

Even minor accidents require complete evidence.

2.2 “Golden Three Principles” for On-Site Handling

Principle 1: Photograph First, Move Second

Many are rushed by traffic behind them, snap a few shots, and move. Critical evidence is lost. Must capture:

- 4 wide-angle shots: front, back, left, right, including lane markings, signals, surroundings

- Close-ups of contact points and damages

- Opponent info: license plate, registration, driver’s license, insurance

- Road condition evidence: traffic lights, signs, surveillance cameras

Principle 2: Call the Police — Even for Minor Accidents

Many countries require police reports if injuries occur, responsibility is disputed, or vehicles are immovable. Even if not legally required, filing a report protects you. Police accident reports are strong evidence for claims.

Report deadlines differ: Germany — liability claims within 1 week, accident insurance within 48 hours. Most regions: report within 24 hours, no later than a few days post-accident. Delays may lead to insurer questioning authenticity or denying claims.

Principle 3: Risks of Settling Privately and Correct Methods

Private settlement risks:

- Other party reneges; insurer claims “hit-and-run”

- Underestimating total costs; repairs exceed expectation

- Injuries incur ongoing medical costs

If settling privately, at minimum:

- Written agreement: state “mutually agreed, one-time settlement, no further liability” (legal effect depends on local law; does not remove liability for injuries)

- Photos: both parties’ documents, plates, handwritten agreement

- Payment memo: note “accident settled, no further liability” (legal in most countries; serves as civil evidence but cannot replace insurance or legal requirements, especially for injuries or criminal liability)

2.4 Common Claim Denial Traps

Trap 1: Repairing Without Authorization

Do not repair before insurer assessment; otherwise, claim may be denied for “unable to verify loss.”

Trap 2: Incomplete Evidence

Photos, documents, accident report are essential.

Trap 3: Misrepresentation

Fatal trap. Example: In New Zealand, a couple filed two separate accidents as one claim. Insurer discovered misrepresentation; claim denied, policy canceled, recorded in claims database, future insurance difficult.

Part Three: Rush Hour Accidents — How to Claim Fast

3.1 App Claims + Online Assessment, Paid Next Day

Ms. C had a minor intersection collision during morning rush, other party fully at fault. She used the insurer’s app to upload photos, documents, and scene images. Automated assessment completed, payment received next day — under 24 hours.

Not exceptional: insurer data shows online claims average 0.39 days, fastest case completed in 7 minutes.

3.2 Three Core Strategies for Fast Claims

Strategy 1: Use Insurance App / Online Reporting

Most insurers offer apps. Upload photos and details for remote assessment; avoids waiting for an adjuster. Can reduce processing time 30–50%.

Strategy 2: Claim Through Your Own Insurance First

Many wait for the other driver’s insurer. They have no obligation to respond quickly. Using your own collision coverage first, then subrogation against the other driver, is faster and less hassle.

Strategy 3: Choose Partner Repair Shops

Assessment speed affects claim timeline. Partner shops provide one-stop assessment + repair fastest. Independent shops may require adjuster visit, extending timeline.

Part Four: Commuter Accident Claim Timeline — How Long Until Paid?

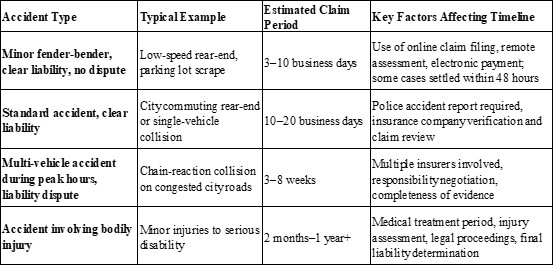

4.1 Reference Timeline by Accident Complexity

4.2 Key Variables Affecting Timeline

Variable 1: Injury Involved

Most critical. Pure vehicle damage: 2–4 weeks. Even a “complaint of pain” extends to 2–6 months due to medical assessment, negotiation, or litigation.

Variable 2: Lawyer Involvement

U.S. data: 57% of cases involve lawyers within 24 hours, 72% within 14 days. Lawyer involvement increases duration; settlements can be 34× higher than non-litigation cases.

Variable 3: Liability Clarity

In rush hour multi-car accidents, insurers spend time determining responsibility. Dashcam footage can reduce “weeks” to “days.”

Variable 4: Repair Costs

2025 data: repair costs up 3.2%, mainly labor-driven. Higher repair costs complicate assessment, extending claims. Developed countries: labor and parts dominate; timeline impacted. Developing countries: labor low, repair distribution uneven; timeline affected more by process efficiency than cost.

Part Five: Commuter Auto Insurance Selection and Claims Summary Table

The essence of auto insurance is not “buying peace of mind” but “buying certainty.” Choose the right coverage, handle accidents correctly, and use proper claims processes. What you save is not just premiums, but time and energy.

References

1. National Highway Traffic Safety Administration (NHTSA). (2022). Urban traffic accidents and low-speed collisions statistics. Washington, D.C.: U.S. Department of Transportation.

2. Allstate. (n.d.). Milewise: Pay-per-mile car insurance. Retrieved March 25, 2026, from https://www.allstate.com/milewise

3. CarGurus. (n.d.). What to do after a car accident: A step-by-step guide. Retrieved March 25, 2026, from https://www.cargurus.com

4. claimjusticeusa.com. (n.d.). How long does a car accident claim take? Retrieved March 25, 2026, from https://www.claimjusticeusa.com

5. insuranceclaimsexplained.com. (n.d.). The importance of evidence in car accident claims. Retrieved March 25, 2026, from https://www.insuranceclaimsexplained.com

6. Metromile. (n.d.). Pay-per-mile car insurance. Retrieved March 25, 2026, from https://www.metromile.com

About the Author

Emma Lawrence

Emma Lawrence is an urban mobility and auto insurance consultant with over 8 years of experience analyzing city traffic patterns, commuter risk management, and insurance claims optimization. She has worked with both private insurers and municipal traffic safety agencies, helping develop practical strategies for reducing claims costs and improving policy efficiency. Emma regularly writes for transportation journals and online publications focused on commuter safety and cost-effective insurance solutions.

Editorial Transparency Statement

This article is based on publicly available data, industry reports, and professional experience. It is intended for informational purposes only and does not constitute legal or financial advice. The author has no direct affiliation with specific insurance providers mentioned and has disclosed all sources used for statistics, case studies, and examples.

Disclaimer

The information in this article should not be considered professional insurance, legal, or financial advice. Insurance coverage, exclusions, and eligibility vary widely depending on the provider, jurisdiction, and individual circumstances.

Recommended for you