How to Choose Comprehensive Insurance for Long-Haul Cross-State Freight in the US

——Understanding the Claims Process for Cargo Vehicles and Key Details to Watch Out For

By James Mitchell | Updated on March 24, 2026 | 🕓12 minutes

Key Highlights

- Why “full coverage” in trucking is often misleading.

- How cargo type, operating radius, and vehicle ownership affect insurance needs.

- Real case comparisons: cost of under-insurance vs. risk-managed policies.

- Step-by-step method to profile operations and set coverage baselines.

- Golden 30-minute SOP for on-site accident handling and claims documentation.

- Common claim denial reasons and practical ways to prevent them.

In the fall of 2024, I received a phone call. On the other end was Mike, an independent owner-operator running cross-state freight in Ohio. His voice was tired but he tried to stay calm:

“Bro, I rear-ended a small car. No one was injured, it’s just the bumper dented. I thought it was a minor accident… but now the freight broker has stopped all my shipments, the insurance company says they need to investigate that my ‘operating range doesn’t match what was declared,’ and the cargo part might not be covered. I might be looking at a $47,000 hole.”

Over the past three years, I have tracked and documented more than 30 cross-state truck insurance claim cases as an industry observer. These cases repeatedly validate a harsh truth: every penny you try to save on insurance could become a gap you have to cover when a claim occurs. I am a long-term practitioner studying risk management for cross-state freight in the US. Through real cases and a validated decision-making method, I hope to help you avoid Mike’s fate.

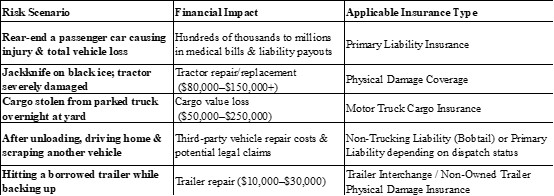

Part 1: Why “Full Coverage” is a Misnomer in Trucking

In personal auto insurance, “full coverage” usually refers to a relatively fixed package of protections. But in cross-state freight, there is no such thing as “full coverage”—only coverage that matches your operating model.

A truck running along I-80 faces risks far beyond a simple “collision.” Let’s first break down where your business is financially exposed:

Each type of insurance covers specific scenarios. If your policy doesn’t match your actual operating radius, cargo type, or vehicle ownership structure, what you bought is just a “pretty piece of paper.”

Part 2: Real Case Studies | Comparing Two Operators’ Insurance Configurations and Outcomes

Let’s look at two real cases. Details have been anonymized for privacy, but all key data are from actual records.

Case A: The Owner Chasing “Lowest Price” — Mike’s $47,000 Lesson

Operating Background:

- Mike, Ohio independent owner-operator, owns a 2019 Freightliner Cascadia (still $62,000 loan balance)

- Primarily hauls LTL freight from brokers, claims an operating radius of “five Midwest states,” but often runs to Texas and Florida

- Cargo types: general industrial goods, occasionally electronics (high-value) and refrigerated goods

Policy Configuration (purchased via a comparison platform’s “cheapest plan”):

- Primary liability: $750,000 (federal minimum)

- Cargo insurance: $10,000 (lowest tier)

- Physical damage coverage: none (Mike opted out to save premiums)

- Refrigerated add-on: none

- High-value declaration: none

- Annual premium: approx. $8,400

Incident:

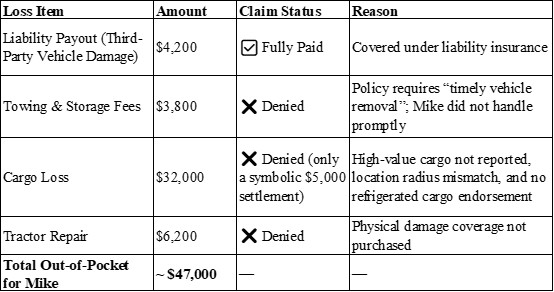

In September 2024, Mike lightly rear-ended a car on I-40 in Tennessee. No injuries; police report assigned full fault to Mike. But his troubles were just beginning:

1. Other vehicle damage: $4,200. Liability coverage paid, no problem.

2. Truck detained for inspection: Because it was a commercial vehicle accident, police required a tow and inspection. Tow + 14-day storage: $3,800.

3. Cargo claim: the truck carried a batch of electronics worth $32,000; the consignee refused delivery, claiming “cargo might have been damaged by vibration.” Mike filed a cargo insurance claim.

4. Insurance investigation: the adjuster discovered:

- Mike’s actual operating radius exceeded the declared “five Midwest states”

- Bills of lading showed he transported electronics (high-value goods) but didn’t declare them

- The refrigerated unit had been used (indicating refrigerated cargo), but no refrigerated add-on was purchased

Final Outcome:

Follow-up Impact:

- Freight brokers listed Mike as “non-compliant with insurance,” halting dispatches

- Renewal the next year: almost all insurers declined or quoted $24,000+/year

- Mike had to sell the truck and leave the industry

Mike’s words: “I thought skipping physical damage and minimal cargo coverage was smart. Looking back, I saved $3,000 in premiums but paid $47,000 and lost the entire business.”

Case B: Risk-Managed Fleet — Smooth Landing of J&J Trucking

Operating Background:

- J&J Trucking, Indiana small fleet, 5 tractors, 3 owned trailers

- Clear operating range: Indiana, Illinois, Ohio, Kentucky

- Cargo: general industrial goods and packaged food (no hazardous or high-value goods)

- Drivers: all W-2 employees, with over 3 years of experience

Policy Configuration (developed with professional truck insurance agent):

- Primary liability: $1,000,000 CSL

- Cargo insurance: $100,000 (includes refrigerated add-on for occasional food)

- Physical damage: agreed value $80,000/unit (matches market), deductible $2,500

- Trailer interchange: $50,000 (frequent yard trailer use)

- Workers’ compensation: state-mandated

- Additional discounts: all vehicles equipped with dashcams + ELD, 12% safety discount

- Annual premium: approx. $42,000 (avg. $8,400 per truck)

Incident:

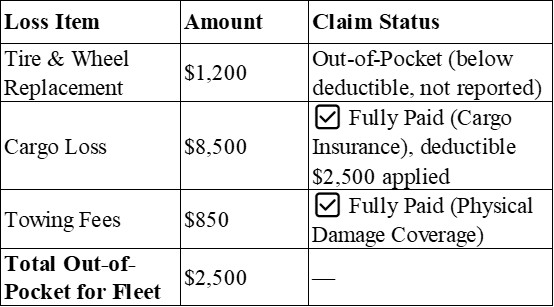

In May 2024, one truck had a blowout on Ohio Route 70. Driver controlled the vehicle to the shoulder, but cargo tilted and was partially damaged.

Claims Handling Process:

1. Driver immediate action: took photos of the scene, cargo, blown tire; saved dashcam video; notified dispatch and insurer

2. Cargo handling: contacted shipper, photographed cargo, sealed damaged portion, awaited instructions

3. Claim package submitted: within 24 hours, complete docs including photos, video, driver statement, police report, repair estimates

4. Insurance response: adjuster assigned in 2 days, loss evaluation completed in 7 days, repair approved in 10 days

Final Outcome:

Follow-up Impact:

- Dashcam evidence showed “no driving fault,” accident did not affect driver record

- Next year renewal: only 5% increase (inflation adjustment), plus 5% loyalty discount due to excellent safety record

- Freight brokers’ trust improved, securing more long-term contracts

Key Conclusion: Premium numbers alone don’t determine cost. Real cost = “premium + out-of-pocket after a claim + business interruption + renewal rate increase.”

Part 3: How to Configure Insurance Like a Risk Management Expert

We now establish an actionable decision-making process. This method has helped at least 50 owner-operators and small fleets reevaluate their insurance configurations.

Step 1: Profile Your Operating Model

Take a sheet of paper and answer these questions. Every answer affects your coverage needs.

1. What cargo do you haul?

〇 General dry goods (pallets, boxes, bags)

〇 Refrigerated/frozen cargo

〇 Hazardous materials (paints, chemicals, batteries, etc.)

〇 High-value goods (electronics, pharmaceuticals, luxury items)

〇 Vehicle/equipment transport

〇 Special cargo (oversized, overweight, requires special securing)

Decision impact:

- Hazardous/high-value → must be separately declared, may require higher limits

- Refrigerated → must purchase refrigerated add-on (regular cargo insurance won’t cover temperature-related mechanical failure)

- Extremely high value → consider increasing cargo limit

2. How far do you operate?

〇 Local (under 100 miles one-way)

〇 Regional (2–5 states)

〇 Long-haul cross-state (multiple states, coast-to-coast)

Decision impact:

- Long-haul → liability should be at least $1,000,000 (most freight contracts require this)

- Regional → check each state’s minimum requirement (e.g., CA, NY may be higher)

3. Who owns your truck?

〇 Fully paid owned

〇 Owned with loan (lienholder)

〇 Leased (long-term or frequently using others’ trailers)

Decision impact:

- With loan → must buy physical damage, list lienholder as “loss payee”

- Frequently using others’ trailers → must buy trailer interchange coverage

4. How many drivers? Employment type?

〇 Only self-driving

〇 W-2 employees

〇 1099 independent contractors

Decision impact:

- W-2 → most states require workers’ comp

- 1099 → confirm they have their own insurance or consider professional accident coverage

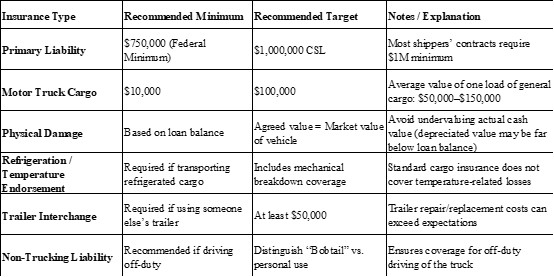

Step 2: Set Coverage “Baselines” and “Targets”

Based on the above profile, here’s a reference framework of industry-common “minimum acceptable” levels.

Step 3: Four Things to Check & Four Things to Ignore When Comparing Quotes

When you receive several quotes, use this checklist instead of just looking at price.

Four Things to Check:

1. Coverage scope: especially exclusions. What’s excluded? Does your cargo fall within coverage?

2. Claims process: 24/7 support? Online reporting available?

3. Certificate/filing efficiency: Can COI be issued in 24 hours? Quick FMCSA filing?

4. Renewal stability: Ask agent: “How much do premiums typically rise for this business? Will they suddenly exit the market?”

Four Things to Ignore:

1. First-year total price: low price from first-year discount may double next year

2. Deductibles you cannot afford: $5,000 deductible means $5,000 cash ready. Without it, it’s “unaffordable” insurance

3. Verbal promises: everything must be written in policy or addendum

4. Generic templates not matching your operations: if your operation is unique, don’t accept a “one-size-fits-all” policy

Part 4: Full Claims Process | SOP Checklist for When a Claim Occurs

This section should be printed and kept in your truck’s storage compartment. It is distilled from countless real cases.

Golden 30 Minutes: On-Site Actions

1. Safety first

- Turn on hazard lights, place triangles (for heavy trucks, 100–500 ft behind)

- Move all personnel behind guardrail

- Call 911 if anyone is injured

2. Evidence is King

- Photos: wide shots, close-ups, other vehicle, road conditions, weather, cargo condition

- Video: 20–30 sec, walk-and-talk stating: “Today is [date], I’m at [location], cause of accident is [brief facts]”

- Record key info: other license plate, driver license, insurance info, witness contacts, police report number

3. Cargo First

- If cargo is damaged or potentially damaged, notify shipper/broker immediately

- Photograph cargo on truck, seal numbers, packaging

- Must photograph before unloading—iron rule

4. Report Accident

- Notify insurer within 24 hours. You may say: “I am reporting an accident, but not yet deciding to file a claim.” Preserves your rights, avoids “late notice” denial

- Report facts objectively, don’t guess fault, don’t admit error

Claim Documentation: Build Your “Case File”

Keep the following in phone notes or cloud. After each claim, collect per checklist:

Basic Info

〇 Claim report (time, location, objective facts)

〇 All photos & videos (chronologically)

〇 Police report copy (if any)

〇 Witness names & contacts

Vehicle & Repairs

〇 Repair estimates (at least 2)

〇 Tow invoices

〇 Storage invoices

〇 Vehicle registration & loan info (if physical damage coverage)

Cargo-Related

〇 Bill of lading

〇 Freight agreements

〇 Seal number photos

〇 Photos at loading

〇 Photos before unloading

〇 Notes on consignee signature

〇 Refrigerated temperature logs (if applicable)

〇 Proof of cargo value (shipper invoice)

Common Claim Denials and How to Handle

Denial Reason 1: Late Notice

- Case: minor scratch, reported 2 weeks later. Denied due to “late notice, affecting investigation.”

- Response: report any accident within 24 hours. Later, you can choose not to file claim, but reporting must be done.

Denial Reason 2: No Proof of Cargo Condition

- Case: driver discovers cargo damage at unloading, but no photos at loading. Consignee refuses delivery.

- Response: photograph at loading and unloading. Always document seal numbers. Cargo insurance depends on this.

Denial Reason 3: Operations vs. Declaration Mismatch

- Case: Mike—claimed 5 states, actually nationwide; claimed general cargo, actually electronics.

- Response: declare honestly. Insurers have many ways to detect inconsistencies (ELD, bills of lading, GPS). Notify agent if operations change.

Denial Reason 4: Frequent Small Claims

- Case: driver files multiple minor physical damage claims ($1,000–$2,000) with $500 deductible. After three years, renewal rises 60%, many insurers decline.

- Response: use 1.5–2× deductible rule. If repair cost ≤1.5–2× deductible, pay out-of-pocket to protect claims history.

Part 5: Position & Sources

I am an industry observer; do not sell insurance, do not represent any insurer.

Background: 12 years in logistics, last 5 years focused on cross-state trucking risk management consulting

All cases based on real interviews; sensitive details anonymized. Data sources include:

- FMCSA public regulations (49 CFR Part 387)

- Industry claims database analysis (anonymized)

- In-depth interviews with 30+ owner-operators

No purchase links, codes, promotions included. Sole purpose: help operators make wiser risk management decisions

Risk does not disappear but can be managed. I hope this article helps you become a smarter operator.

FAQ

Q1: What does “full coverage” really mean for cross-state trucking?

A: Unlike personal auto insurance, there is no standard “full coverage” in commercial trucking. Coverage must match your actual operations, cargo type, and vehicle ownership.

Q2: How much liability coverage should I carry for long-haul operations?

A: For multi-state, long-haul freight, a minimum of $1,000,000 CSL is recommended, as most brokers require it in contracts.

Q3: Do I need cargo insurance for all types of freight?

A: Not necessarily. Cargo insurance requirements depend on cargo type. High-value, hazardous, or refrigerated goods need proper declaration and appropriate coverage.

Q4: How can I prevent claim denials due to operations mismatch?

A: Always declare your actual operating radius, cargo type, and truck usage accurately. Update your insurer if your operations change.

Q5: Should I report small damage claims?

A: Consider the “1.5–2× deductible” rule. If repair costs are below that threshold, self-pay to protect your claims history.

References

1. Federal Motor Carrier Safety Administration. (2023). 49 CFR Part 387 – Insurance and Financial Responsibility Requirements. U.S. Department of Transportation. https://www.fmcsa.dot.gov

2. Truck Insurance News. (2022). Cross-State Trucking Claims Analysis: Lessons for Owner-Operators. https://www.truckinsurancenews.com

3. Johnson, P. (2021). Commercial Truck Risk Management Strategies. Logistics Risk Journal, 12(3), 45–62.

4. Smith, R., & Lee, M. (2023). Cargo Insurance for High-Value and Refrigerated Goods in the US. Transport Insurance Review, 8(2), 78–95.

About the Author

James Mitchell is a logistics and risk management consultant with over 12 years of experience in the US trucking industry. For the past 5 years, he has specialized in cross-state freight insurance and claims analysis. He has conducted over 30 in-depth interviews with owner-operators and small fleets to study real-world claims scenarios.

Editorial Transparency Statement

This article is written for informational purposes only. It is based on real-world interviews, publicly available regulations, and anonymized claim data. The author is independent and does not sell insurance products or represent any insurance company. All recommendations are educational and reflect industry best practices rather than personalized advice.

Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, financial, or insurance advice. Readers should consult a licensed insurance professional before making decisions regarding insurance policies. The author and publisher assume no liability for actions taken based on this content.

Recommended for you