How to Choose Short-Term Commercial Vehicle Insurance for Cargo Safety (With Real Cases & Global Insights)

——Short-Term vs Long-Term Commercial Truck Insurance: A Practical Guide for Safer Cargo Transport

By Michael Reynolds | Updated on March 27, 2026 | 🕓15 minutes

Key Highlights

- What is the real difference between short-term and long-term commercial truck insurance?

- When should you choose short-term insurance instead of an annual policy?

- Why do claim denials happen even when you have insurance?

- How much liability coverage is enough for commercial transport?

- What is the safest insurance strategy for transport businesses?

On October 31, 2022, in New Brunswick, Canada, a trailer owned by WK & NN Trucking Ltd. was severely damaged after colliding with a loader. The accident itself was not complicated—liability was clear, and the loss was easy to estimate. However, when the vehicle owner filed a claim with Nordic Insurance Company of Canada, the response they received surprised everyone:

“The policy does not provide collision coverage, and direct property damage compensation does not apply.”

The loss had already occurred, the policy was in hand, yet the insurer refused to pay. Why?

Even more shocking, what appeared to be an ordinary denial case eventually turned into a prolonged legal battle. It was not until February 2025 that the court issued a ruling, and only after several months of delay was the insurance company allowed to submit its defense.

Stories like this unfold daily across the global freight industry.

Many transport operators believe that having insurance guarantees safety—until a claim is denied and they realize they have been effectively uninsured all along. Risks in commercial transportation go far beyond “fixing the truck after a crash.” What truly brings down a transport business is often cargo loss, third-party liability, and operational disruption.

Chapter 1: Short-Term Insurance — When Risk Is “One-Off”

What is short-term commercial vehicle insurance?

Short-term commercial vehicle insurance, as the name suggests, is a temporary insurance solution covering periods ranging from 1 day to 90 days. It is not a “cut-down” version of an annual policy, but a tool precisely designed to match temporary needs.

The essence of short-term insurance is that you only pay for the risks that are happening “right now.”

Case 1: Cross-border cold chain transport from Spain to Northern Europe

In 2020, a refrigerated semi-trailer lost control, overturned, and caught fire while traveling on Spain’s “Silver Highway.” The vehicle was transporting fresh fruits and vegetables from Huelva and Cádiz to multiple destinations in Finland, the Netherlands, Estonia, and Latvia, with a commercial value of €65,283.64.

After the accident, part of the cargo remained in the trailer while some was scattered on the ground. Following an emergency inspection, the entire shipment was deemed “unfit for human consumption” and was destroyed.

This was not a routine shipment—multi-country, multi-destination, cold chain, and high-value. Instead of purchasing an annual cargo policy, the shipper insured this specific trip with a cargo insurance policy.

After the incident, insurer INGO quickly initiated the claims process. Experts conducted a comprehensive evaluation of the damaged goods, reviewed technical reports of the refrigeration system, and verified whether transport conditions complied with food safety regulations. The investigation confirmed that temperature control had failed and packaging integrity was compromised, rendering the goods unsellable.

Outcome: The temporary cargo insurance policy was triggered, and the shipper received full compensation of 3.4 million Ukrainian hryvnia (approximately $85,000). A single accident did not lead to financial ruin.

Key takeaway: Cold chain logistics carries significantly higher risks than standard freight—equipment failure, temperature fluctuations, and thawing can destroy an entire shipment. For such “one-off, high-value, high-risk” transport tasks, short-term insurance is the most precise risk management tool.

Case 2: Temporary rental vehicle as a “backup player”

In 2024, a logistics company’s primary truck required major engine repairs. The company urgently rented a replacement truck for 15 days.

The issue was that the rental vehicle only had basic liability insurance, which was far from sufficient for commercial transport. Purchasing an annual policy was not cost-effective for such a short period. Ultimately, they chose a short-term truck insurance policy that included cargo liability and roadside assistance.

During those 15 days, the vehicle was involved in a minor collision while unloading. The short-term insurance covered all damages. Without coverage, the company would not only lose profit from the shipment but also have to pay for cargo damage out of pocket.

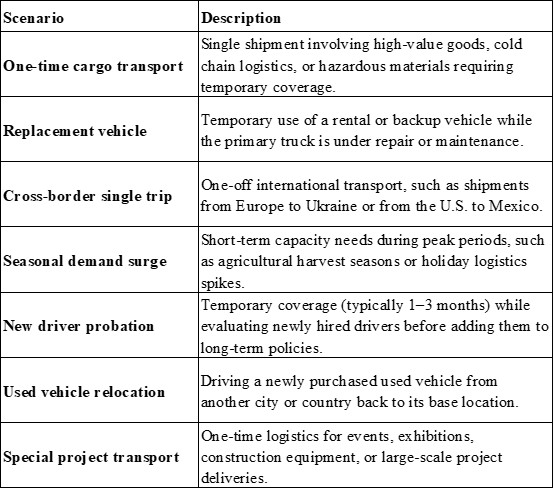

Seven typical scenarios for short-term insurance

Three major pitfalls of short-term insurance

Pitfall 1: Coverage gaps

Multiple short-term policies may leave “gaps” in coverage. Even a single day without insurance means 100% exposure to loss.

Pitfall 2: Low coverage limits

Some short-term policies reduce liability and cargo limits to lower premiums. For high-value cargo or major accidents, these limits may be insufficient.

Pitfall 3: “Definition traps” in policy wording

In short-term policies, the interpretation of a single term can determine the outcome of a claim. The 2022 WK & NN Trucking case is a classic example—where the insurer claimed the policy “did not provide collision coverage,” forcing the owner into litigation. Understanding policy wording before purchase is far more important than arguing during claims.

Chapter 2: Long-Term Insurance — Making Risk “Predictable”

If short-term insurance is a “tactical tool,” long-term insurance is the “strategic foundation.” For fleets and transport businesses with stable operations, long-term insurance is an essential risk management system.

Core structure of long-term insurance

Based on industry practice, a comprehensive long-term commercial vehicle insurance plan should include four layers:

Layer 1: Mandatory liability insurance (legal baseline)

This is the “entry ticket” for operating legally. In most countries, coverage limits are relatively low and insufficient for major accidents.

Layer 2: Commercial third-party liability insurance (first line of defense)

This is the core protection against third-party losses. In a 2022 case in Connecticut, USA, a box truck collision left Wanda Gomez seriously injured. The jury awarded $5.7 million, with total compensation nearing $7.5 million after legal costs and interest.

Insight: For long-haul fleets, liability limits should be at least $1 million. For urban delivery fleets, even higher limits are recommended due to frequent exposure to dense traffic.

Layer 3: Physical damage insurance (asset protection)

Covers vehicle damage from collisions, rollovers, fire, and natural disasters. For new or nearly new vehicles, full coverage is recommended.

Layer 4: Cargo insurance (key differentiator)

This is what distinguishes commercial transport insurance from standard auto insurance. Coverage varies significantly depending on cargo type.

Case 3: $750,000 denial — the cost of delayed notification

In March 2022, a serious accident occurred in Connecticut, USA. A box truck driven by Keith Claiborne collided with another vehicle, severely injuring Wanda Gomez. In January 2023, Gomez sued the driver, his employer City Line Distributors LLC, and leasing company Penske Truck Leasing Co.

City Line’s insurance structure included:

Primary insurer: Old Republic Insurance Co.

Umbrella policy: Everest National Insurance Co., with $10 million coverage

The issue: Everest was never informed of the lawsuit.

In June 2024, Gomez proposed a $2 million settlement. City Line declined. In January 2025, the jury awarded $5.7 million, with total compensation nearing $7.5 million.

City Line attempted to appeal but failed. It was not until July 2025—after the judgment and appeal—that Everest first learned of the case.

In August 2025, Everest filed suit seeking a declaratory judgment that it had no obligation to pay, citing breach of the policy’s notification clause.

Key takeaway: Notification obligations in long-term policies are critical. If insurers are excluded from the litigation process, even a $10 million policy can become worthless.

Case 4: The dispute over the definition of “operation”

In 1992, the U.S. Fifth Circuit Court of Appeals ruled on a key case involving Western American Specialized Transportation Services, which frequently leased trucks to supplement its fleet.

Lloyd’s of London issued a cargo insurance policy containing an exclusion clause requiring that vehicles be “operated” by the insured or its full-time employees.

The dispute centered on the meaning of “operation.”

The insurer argued it meant “driving.” Since independent contractors drove the trucks, claims were denied.

Western argued it meant “control and management.” The court agreed with Western, stating that requiring a corporation to physically drive vehicles was absurd.

Key takeaway: Definitions in long-term policies are critical. A single term can determine millions in claims.

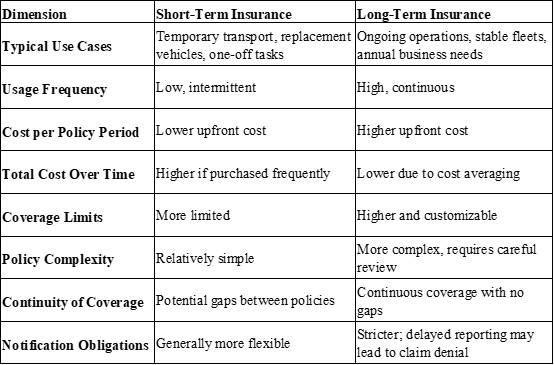

Chapter 3: Short-Term vs Long-Term — A Decision Table

Practical strategy: the optimal combination

For most transport businesses, the optimal solution is:

Long-term insurance as the foundation + short-term insurance as a supplement

Long-term foundation: Covers baseline risks year-round

Short-term supplement: Addresses high-value or high-risk scenarios

Chapter 4: Pitfall Avoidance Guide — Five Common Reasons for Claim Denial in Short-Term and Long-Term Insurance

1. Delayed Notification (The Most Critical)

Issue: After an accident occurs or a lawsuit notice is received, the policyholder fails to notify the insurance company within the time specified in the policy.

Consequence: A $7.5 million judgment, with the insurer denying coverage on the grounds of “late notification.”

Prevention: Establish an “immediate notification” mechanism. For any potential claim, lawsuit, or accident, notify all relevant insurers at the earliest possible moment (including primary insurers and umbrella insurers). Do not assume that “if the primary insurer knows, the excess insurer will automatically know.”

2. Misunderstanding of Key Terms

Issue: Does “operation” in the policy mean “driving” or “control”? Does “collision coverage” apply to specific types of accidents?

Consequence: Claim denial by the insurer, requiring litigation to resolve, often taking months or even years.

Prevention: At the time of purchase, request written clarification from the insurer on key policy terms (such as “operation,” “collision,” “full-time employee,” and “independent contractor”). If possible, incorporate these definitions directly into the contract.

3. Incorrect Carrier Classification

Issue: Declaring as a “common carrier” during underwriting while actually operating as a “private carrier” (or vice versa), leading to misapplication of liability standards.

Consequence: In the Philippine case, the carrier argued it was not a common carrier, yet the court still held it liable—simply because it failed to prove that it had exercised due diligence.

Prevention: Accurately disclose your operational model. If your transport business serves a single client exclusively, clearly inform the insurer and confirm whether the policy still applies under such conditions.

4. Undeclared Cargo Type (Cold Chain / Hazardous Goods)

Issue: Transporting refrigerated goods, hazardous materials, or high-value cargo without proper declaration, or insuring them as ordinary goods.

Consequence: In the Spanish case, refrigerated goods were destroyed in an accident; the shipper received compensation only because cargo insurance was in place. Without it, the loss would have been total.

Prevention: Accurately declare cargo type during underwriting. For cold chain transport, confirm whether the policy covers spoilage due to refrigeration system failure. For hazardous materials, verify whether additional coverage requirements apply.

5. Overloading or Route Deviation

Issue: Overloading the vehicle or significantly deviating from the declared transport route.

Consequence: The insurer may deny the claim on the grounds of “material increase in risk without disclosure.”

Prevention: Strictly adhere to approved load limits and designated routes. If routes must change temporarily, notify the insurer promptly and confirm whether additional premium is required.

Chapter 5: Practical Recommendations — How to Build Your Insurance System

Step 1: Assess Your Operational Risk Profile

Long-haul vs urban delivery: Long-haul operations require high liability limits and cargo insurance; urban delivery must focus on frequent minor collisions and bodily injury risks

Standard vs specialized cargo: Cold chain, hazardous materials, and high-value goods require dedicated insurance solutions

Tractor vs trailer: Confirm whether the trailer requires separate insurance (as clarified by European court rulings)

Owned fleet vs leased fleet: For leased vehicles, verify the scope of existing coverage and purchase short-term supplementary insurance if necessary

Step 2: Build a Three-Layer Structure — “Base + Enhanced + Scenario-Based”

Base layer: Mandatory liability insurance + third-party liability insurance (recommended starting at $1 million) + physical damage coverage

Enhanced layer: Umbrella liability insurance (especially in the U.S. market), cargo insurance (based on cargo value), and business interruption insurance

Scenario layer: Cold chain coverage for refrigerated goods, pollution cleanup coverage for hazardous materials, and country-specific clauses for cross-border transport

Step 3: Establish a Claims Response Mechanism

Immediate notification: Notify all relevant insurers (primary + umbrella) within 24 hours of any incident

Settlement decisions: When receiving a reasonable settlement offer, communicate promptly with insurers. Rejecting a reasonable settlement without valid justification may result in denial of coverage for excess amounts

Documentation retention: Preserve accident scene photos, police reports, proof of cargo damage, temperature logs (for cold chain), repair estimates, and other relevant records

Step 4: Use Technology to Reduce Premiums

Install intelligent monitoring systems (such as AEBS and ADAS) to qualify for premium discounts

Implement a driver safety scoring system linked to renewal incentives

For larger fleets, negotiate group-based no-claims bonus adjustments

Conclusion: Insurance is Risk Management, Not a Cost

Returning to the opening question: why was WK & NN Trucking’s claim denied?

Not because insurers “don’t pay,” but because of a mismatch between policy definitions and the accident.

Insurance selection is fundamentally about understanding and pricing risk.

Short-term insurance = tactical tool

Long-term insurance = strategic foundation

The optimal strategy is combining both.

Before signing your next policy, ask yourself:

1. What are the risks of this transport task?

2. Does the policy precisely cover those risks?

3. Can I notify all insurers within 24 hours if a claim occurs?

If you can answer these clearly, you won’t discover—after a multimillion-dollar judgment—that you’ve been uninsured all along.

FAQ

1. Is short-term commercial truck insurance more expensive than long-term insurance?

On a per-day basis, yes. However, for temporary or infrequent operations, it is often more cost-effective than purchasing a full annual policy.

2. Can I rely only on cargo insurance without vehicle insurance?

No. Cargo insurance protects the goods, but without liability and vehicle coverage, you remain exposed to third-party claims and physical damage losses.

3. Do leased or rented trucks automatically have sufficient insurance?

Usually not. Rental agreements often include only basic liability coverage. Additional short-term insurance is often necessary for commercial operations.

4. Does cross-border transport require special insurance?

Yes. Different countries have different liability rules, coverage requirements, and legal interpretations. You may need country-specific endorsements or separate policies.

5. What is umbrella insurance, and do I need it?

Umbrella insurance provides additional liability coverage beyond your primary policy limits. It is highly recommended in high-litigation environments such as the United States.

6. Can insurers deny claims due to technical wording in the policy?

Yes. Courts have repeatedly shown that policy definitions and wording can determine whether a claim is paid or denied.

References

1. WK & NN Trucking Ltd. v. Nordic Insurance Company of Canada (2025, Canada)

2. Everest National Insurance Co. v. City Line Distributors LLC (2025, United States)

3. Morey v. Western American Specialized Transportation Services, Inc. (1992, United States Court of Appeals, Fifth Circuit)

4. INGO Insurance Company Cold Chain Cargo Claim Case (2025, Ukraine)

5. Spanish Supreme Court Ruling on Tractor–Trailer Liability Allocation (2025, Spain)

6. FGU Insurance Corp. v. G.P. Sarmiento Trucking Corp. (2002, Philippines)

7. International Road Transport Union (IRU). (2024). Global Guidelines on Road Freight Risk Management.

Note: The above cases and examples are derived from publicly available court decisions and industry claim reports. They are provided for informational and educational purposes only.

About the Author

Michael Reynolds, FCII, CRM

Michael Reynolds is a commercial insurance specialist and transport risk consultant with over 15 years of experience in the global logistics and freight industry. He holds the Fellowship of the Chartered Insurance Institute (FCII) and is a certified Risk Manager (CRM).

Michael has advised trucking companies, freight forwarders, and cross-border transport operators across North America and Europe, with a focus on liability structuring, cargo risk mitigation, and claims strategy.

Editorial Transparency Statement

This article is based on publicly available court decisions, industry reports, and insurance practice insights. All case references are used for educational and analytical purposes.

The content is independently researched and written without influence from insurance companies, brokers, or commercial sponsors. No compensation was received for the inclusion of any specific case, company, or insurance product.

Disclaimer

This article is intended for informational purposes only and does not constitute legal, financial, or insurance advice.

Insurance coverage, policy wording, and legal obligations vary significantly by jurisdiction and individual circumstances. Readers should carefully review policy terms and consult licensed insurance professionals or legal advisors before making any decisions.

Recommended for you