Cross-Border Freight Vehicle Insurance in North America: Key Claims Considerations

—— Lessons Learned from Real-World Case Studies and How to Avoid Common Mistakes

By John Whitman | Updated on March 25, 2026 | 🕓15–18 minutes

Key Highlights

- Overview of cross-border freight insurance risks in the U.S., Canada, and Mexico.

- Core insurance types: Liability, Cargo, Physical Damage, and Cross-Border Endorsements.

- Step-by-step claims process from incident to payment.

- Real-world cases illustrating common pitfalls and lessons learned.

- Regional and regulatory differences affecting claims.

- Practical tools, checklists, and strategies to avoid delays or denial.

Cross-border freight in North America (U.S., Canada, Mexico) forms an economic artery connecting three countries, but it is also a route full of hidden risks. When an accident occurs, you are not just dealing with damaged vehicles or cargo; you also face:

Differences in regulations among three countries: U.S. states have varying requirements for accident reporting, Canada emphasizes document compliance, and some regions in Mexico even require notarized documents.

Insurance coverage gaps: A seemingly complete policy may become worthless if it lacks a “cross-border endorsement.”

Multi-party liability chains: Shippers, carriers, brokers, customs, and insurance companies… claims may get stuck depending on who holds the responsibility.

Based on real claims cases, firsthand experiences from Reddit and industry forums, and operational rules of the North American insurance market, this article systematically breaks down the entire claims process for cross-border freight vehicle insurance—showing you how to prepare, avoid denial, and speed up payment.

Part 1: Types of Insurance and Coverage — Buying the Right Policy Is Just the First Step

1.1 Liability Insurance

Coverage: Pays for bodily injury or property damage to third parties caused by your truck. This is mandated by the U.S. Federal Motor Carrier Safety Administration (FMCSA), usually with a minimum limit of $750,000, but most shippers require coverage over $1,000,000.

Typical case: A Reddit user shared on r/FreightBrokers that after hiring a carrier, an accident occurred, but the carrier’s insurance refused to pay, claiming the driver was not listed on the policy. This left the shipper at risk of third-party lawsuits, ultimately forcing them to use their own legal team to recover losses.

Key lesson: The driver roster must match the insurance policy. Driver turnover is high in cross-border operations, but any driver not listed on the policy can be grounds for denial.

Solution: Regularly update the driver list with your broker and request written confirmation.

1.2 Cargo Insurance

Coverage: Protects the cargo in transit from accidents, theft, natural disasters, and other risks. This is not federally required, but almost all reputable shippers/brokers demand it.

Typical case: A U.S. carrier transporting cargo to Canada had goods stolen at a Canadian customs warehouse while awaiting clearance. When filing a claim, the insurer only covered the U.S. portion, denying losses in Canada due to the lack of a cross-border endorsement. The company had to cover tens of thousands of dollars out of pocket.

Key lesson: The geographic scope of cargo insurance must be explicitly annotated. A policy covering only “domestic U.S.” operations is ineffective in Canada and Mexico.

Solution: Explicitly require the endorsement “Territory: USA, Canada, Mexico, including cross-border operations.”

1.3 Physical Damage Coverage

Coverage: Pays for physical damage to your vehicles (tractors and trailers) due to accidents, fire, theft, etc. For long-haul cross-border transport, this is the core coverage to protect your assets.

Typical case: A Canadian trucker shared on r/Truckers that his vehicle caught fire due to a mechanical failure in Mexico, resulting in a total loss. His U.S. insurer eventually paid, but the process took nearly four months because the insurer had no direct adjusters in Mexico and required third-party translation and notarization.

Key lesson: Cross-border roadside assistance and damage assessment capability are more important than premium cost.

Solution: When purchasing, ask whether the insurer has a partner adjuster network in Mexico and provides cross-border towing service.

1.4 Cross-Border Endorsement

What it is: A specific endorsement that explicitly includes the U.S., Canada, and Mexico, and cross-border transport within the policy’s geographic scope. Without it, your policy may legally cover only “domestic transport.”

Typical case: The Canadian customs theft case above is a classic lesson: “No cross-border endorsement, no coverage for cross-border loss.”

Key lesson: Cross-border endorsements are not automatically included; they must be requested and confirmed in writing.

Solution: Make “cross-border endorsement required” a mandatory request in every purchase or renewal communication.

Part 2: Full Claims Process — From Incident to Payment

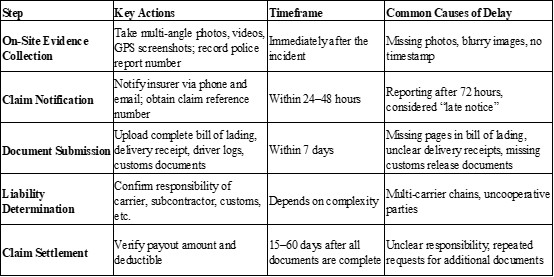

2.1 Seven-Step Claims Process

Step 1: Accident/Cargo Loss Occurs

When a vehicle collision, cargo damage, theft, or any event potentially leading to a claim occurs, the primary task is to ensure personnel safety and, where possible, secure the scene. If third-party property damage, injury, or incidents in certain U.S. states or Mexican regions are involved, immediately contact law enforcement or customs to obtain official records.

Step 2: Evidence Collection at Scene

Take photos and videos from multiple angles with timestamps, showing license plates, damage details, and the overall environment. Save GPS logs or electronic logbook data and record witness information. If customs inspection is involved, document with photos. Completeness at this stage directly affects claim approval.

Step 3: Report the Claim

Contact your insurer within 24–48 hours by phone to obtain a claim number and confirm via email. Keep written records. Notify brokers, shippers, and partners. Late reporting may be deemed “failure to notify,” increasing denial risk.

Step 4: Collect and Submit Documents

Within a week, systematically organize and submit claim documents. Core files include: complete bill of lading (BOL), delivery receipts, driver logs, GPS logs, police reports (if any), customs release documents (for cross-border). Ensure clarity, no alterations, and completeness. Document completeness is the foundation for claim processing.

Step 5: Liability Determination

The insurer determines the responsible party based on investigation, contract, and regulations. Multi-modal or multi-carrier shipments complicate this, sometimes requiring a third-party adjuster. Uncooperative parties are the most common reason for delays.

Step 6: Claim Review

After preliminary liability determination, the insurer reviews all submitted documents to verify coverage, damage amount, and exclusions. Missing or unclear materials may require supplementation. Efficiency depends on prior preparation; repeated supplements significantly extend the timeline.

Step 7: Settlement Payment

Once approved, the insurer confirms the final payment amount, deducts the agreed deductible, and pays. Disputes can initiate review procedures. From incident to payment, cases with complete materials and clear liability usually resolve within 30–60 days.

2.2 Key Points and Common Delays at Each Stage

2.3 Typical Smooth Claims Timeline

Day 1: Accident at U.S.-Mexico border; driver takes photos, reports to authorities, saves GPS logs.

Day 2: Dispatcher calls and emails insurer, receives claim number.

Day 5: Submit complete BOL, delivery receipts, police reports, and driver logs.

Day 20: Insurer completes liability determination (carrier fully responsible), confirms payment.

Day 35: Payment received after deductible deduction.

Key factors for speed: Complete evidence chain, timely reporting, insurer experienced with cross-border claims.

Part 3: Real-World Case Analysis — Lessons from Actual Disputes

Case 1: Denial Due to Incomplete Documents

Source: Reddit r/FreightBrokers

A freight manager submitted over 50 claims in three months. One cargo damage claim, where the carrier accepted responsibility, was denied.

Problem: The insurer cited only one reason—BOL missing the second page, making the submission “incomplete,” unable to verify the link between damage and transport.

Resolution: The manager repeatedly communicated with the claims adjuster, even providing the carrier’s written responsibility confirmation, but the insurer insisted on “incomplete documentation as a legitimate denial reason.”

Outcome: Denied. The manager had to pursue legal action against the carrier.

Lessons:

BOLs, delivery receipts, and other key documents must be complete, clear, and unbroken.

Insurers may use any document flaw as a legitimate denial, not just delay.

Solution: Establish a departure document checklist; drivers photograph every page at loading/unloading and upload to the cloud to catch missing pages beforehand.

Case 2: Carrier Non-Cooperation Causes Claims Deadlock

Source: Reddit r/FreightBrokers

A shipper hired a carrier, and cargo was damaged in transit. The carrier’s insurer initially agreed to handle the claim but later denied, citing “driver not listed on the policy” and “carrier uncooperative.”

Problem: The carrier disappeared, refused to provide logs or accident reports. The insurer stated, “Cannot determine liability without cooperation.”

Resolution: The shipper paid the cargo owner first, then considered suing the carrier. Consulting a lawyer revealed the contract lacked a “cooperation obligation” clause, and litigation costs could exceed compensation.

Outcome: Some suggested using the shipper’s cargo insurance for interim payment, allowing subrogation later, provided the policy grants this right.

Lessons:

Non-cooperative carriers are a common reason for delays or denial.

Solution: Include “cooperation obligation” and penalty clauses in contracts. Consider “contingent cargo insurance” as a backup if carrier coverage fails.

Case 3: Undefined Liability Causes Indefinite Delay

Source: Reddit r/Insurance

Cargo shipped via multi-modal transport (truck + rail) from Mexico to Canada was damaged. The shipper filed a claim.

Problem: The insurer put the claim on hold “waiting for liability confirmation.” Multiple carriers in Mexico, U.S., and Canada shifted responsibility, refusing written acknowledgment.

Resolution: Shipper repeatedly contacted all three carriers over three months with no response. Insurer could not process the claim without liability confirmation.

Outcome: Claim indefinitely delayed. Shipper accepted partial settlement, far below actual loss.

Lessons:

Multi-party cross-border shipments require pre-defined liability allocation.

Solution: In contracts, define a “first leg carrier” or “BOL-issuing carrier” as the single point of contact responsible for coordinating full liability, avoiding multi-party coordination chaos.

Part 4: Regional and Regulatory Differences — Cross-Border Is Not Just “Adding Another Leg”

United States

Regulations vary by state. For example, California and Texas require police reports after accidents, or claims may be denied. Interstate carriers benefit from MCS-90 endorsements providing mandatory coverage. Drivers should immediately report to police and obtain report numbers, confirming the policy includes MCS-90.

Example: A driver in Texas had a minor scrape but did not report it; insurer denied third-party repair costs due to “no official record.”

Canada

Insurers require high document compliance. BOLs, driver logs, cargo lists must be complete and unaltered; customs release documents are often key. Driver logs should match GPS logs; retain customs release proof.

Example: Cargo in Ontario warehouse damaged due to temperature, but lack of customs release time records led insurer to deny, claiming “cargo not in transit.”

Mexico

Some states (Chihuahua, Sonora) require notarized or officially translated documents. U.S. insurers process Mexican incidents slowly. Always confirm Mexican partners and carry Spanish translation tools.

Example: A U.S. driver in Sonora delayed claim 5 months due to lack of notarized local documents.

Border Ports/Customs

Damage during inspections or delays often denied as “unknown cause” or “outside transport.” Buy “customs delay insurance” or “cargo interruption insurance” and document inspections.

Example: Electronics inspected at U.S.-Mexico border were improperly resealed, causing moisture damage; insurer denied, citing “customs actions not carrier responsibility.”

Part 5: Common Claims Mistakes and Prevention Strategies

Mistake 1: Incomplete Documents

Real case: BOL missing second page caused denial.

Prevention: Create departure document checklist; photograph and upload all key documents.

Mistake 2: No Cross-Border Endorsement

Real case: U.S. cargo stolen at Canadian customs, coverage denied.

Prevention: Require “Territory: USA, Canada, Mexico, including cross-border operations” in writing; verify before each trip.

Mistake 3: Undefined Multi-Carrier Liability

Real case: Three carriers denied responsibility, claim delayed indefinitely.

Prevention: Define “first leg carrier” or “BOL-issuing carrier” as single point of contact; include cooperation and penalty clauses.

Mistake 4: Late Reporting

Real case: Driver reported 10 days late; insurer required proof of immediate notification, delaying payment 3 weeks.

Prevention: SOP to report within 24–48 hours via phone + email; retain records.

Mistake 5: Carrier Non-Cooperation

Real case: Carrier disappeared, insurer denied claim.

Prevention: Select reputable carriers; contract clause: non-cooperation equals acknowledgment of liability; consider contingent cargo insurance.

Part 6: Practical Guide and Tool Recommendations

6.1 Document Management Tools

TMS (Transportation Management System): e.g., McLeod, TMW; centralize orders, BOLs, delivery receipts.

Cloud Storage: Google Drive or OneDrive; drivers photograph every page, upload immediately, name by “date + route + vehicle.”

GPS Log Storage: Use ELD (Electronic Logging Device); save at least 6 months (required for claims).

6.2 Claims Time Management

0–24h: Scene documentation and claim report.

1–7d: Collect and submit all documents.

7–30d: Follow up on liability determination, supplement documents.

30+d: If unpaid, escalate to claims manager or start dispute process.

6.3 Risk Protection Tools

GPS Trackers: Record route to prove transport continuity.

Dash Cameras: Record accidents to avoid liability disputes.

Remote Temperature Monitoring: For cold-chain cargo, temperature logs are crucial evidence.

Part 7: Appendices — Practical Tools and Templates

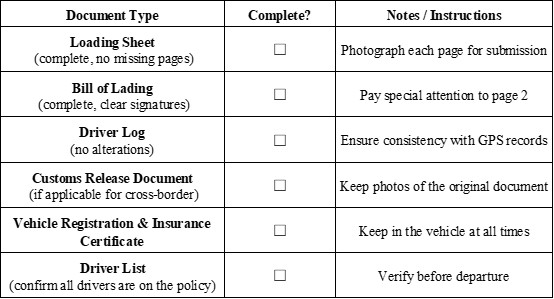

Appendix 1: Departure Document Checklist (Driver/Dispatcher Self-Check)

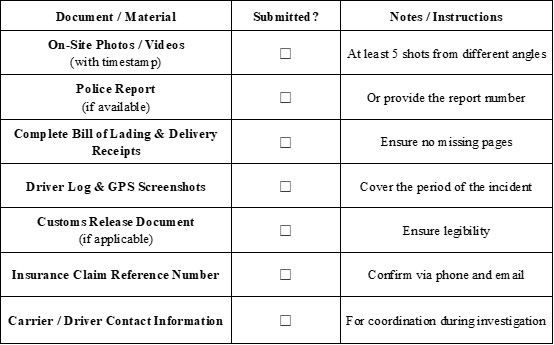

Appendix 2: Claim Submission Materials Checklist

We hope these real cases, practical strategies, and tool lists help you face future incidents with confidence—submitting a complete evidence chain that makes it difficult for insurers to deny.

Insurance is a risk transfer tool, but its effectiveness depends on understanding its boundaries. Cross-border freight risk management begins before purchase and is perfected through daily operational management.

References

1. Federal Motor Carrier Safety Administration. (2023). Commercial Motor Vehicle Safety Regulations. U.S. Department of Transportation. [https://www.fmcsa.dot.gov]

2. Transport Canada. (2022). Commercial Vehicle Insurance Guidelines. Government of Canada. [https://tc.canada.ca]

3. Seguros Mexico. (2021). Cross-Border Cargo Insurance Practices in Mexico. Retrieved from [https://www.segurosmexico.com]

4. Reddit r/FreightBrokers & r/Truckers. (2019–2023). Real-world user discussions on freight claims.

5. McLeod Software. (2022). Transportation Management Systems for Document Compliance. [https://www.mcleodsoftware.com]

About the Author

John Whitman

John Whitman is a logistics and insurance consultant with over 12 years of experience in North American freight operations. He has worked with cross-border carriers, shippers, and brokers, advising on risk management and insurance compliance. John is also a frequent contributor to industry forums and publications focused on freight insurance and claims best practices.

Editorial Transparency Statement

This article was written based on publicly available information, industry guidelines, and firsthand accounts shared on professional forums. It has been independently researched and does not receive sponsorship, advertising, or endorsement from insurance providers. The content is intended to educate and inform readers about cross-border freight vehicle insurance practices.

Recommended for you