Which Insurance Coverage is Best for Long-Distance Cross-State Driving in the US?

——Essential Add-Ons to Consider and How to Prepare for Claims After an Accident

By Ethan Walker | Updated on March 23, 2026 | 🕓10–12 minutes

Key Highlights

- Liability vs Collision vs Comprehensive

- Best Add-Ons for Cross-State Road Trips

- Roadside Assistance

- Rental Car Reimbursement

- MedPay vs PIP

- Cost vs risk trade-off explained

- GAP, Mechanical Breakdown, Glass Coverage

- Accident Handling & Claims Preparation

Let me start with my own story. Last summer, my friends and I planned a road trip from Los Angeles to Seattle, about 1,200 miles in total. Before we set off, I naïvely thought, "I have insurance, it should be fine." But one rainy night in Oregon, I suddenly realized—I had no idea what my policy covered, nor did I know if coverage would change once crossing state lines.

The trip ended safely, but when I returned, I spent two weeks researching and realized just how many pitfalls I almost stepped into. After discussing this with friends, I found out that nearly everyone had similar confusion.

I heard someone share his experience: "I thought I had full coverage, but after being rear-ended in Arizona, I realized my policy didn’t include UM (Uninsured Motorist) coverage. The other driver was an uninsured tourist renting a car, and my insurance company told me I’d have to pay the $12,000 repair bill myself. In the end, I had to scrape together the money to get my car fixed. That trip was the darkest moment of my life.”

Now, I’ve gathered my own experience and those of others online to explain how to get the right insurance for a cross-state road trip, which expenses are worth paying for, which you can skip, and how to handle claims smoothly if something goes wrong.

1. What Does "Full Coverage" Really Mean? — A Story That Made Me Rethink My Policy

1.1 What is "True Full Coverage"? The Lesson I Learned from My Car Being Hit

Let’s talk about my neighbor John in New York. Last year, he drove from New York to Florida, and before leaving, he thought "minimum liability insurance will be enough, I’m a careful driver." But when he reached a small town in Georgia, he parked his car in a hotel parking lot overnight, and the next morning he found a tree had fallen on his car due to a storm.

“I was in total shock,” John told me. “I called my insurance company, and they asked if I had comprehensive coverage (Comprehensive). I said no, I only bought liability. They told me liability only covers damage to others, and this tree incident is considered an act of nature, so I’d have to pay for repairs myself.”

In the end, he spent almost $4,000 on repairs, and his whole trip was ruined. Now, he tells everyone: when doing a long road trip, always buy comprehensive coverage—it seems unnecessary until you really need it.

From that moment, I’ve kept a simple rule when buying car insurance: liability + collision + comprehensive coverage makes up the real "full coverage."

What do these three cover? Here’s a simple breakdown:

- Liability insurance: Covers the damage to others’ property and medical expenses when you cause the accident. This is legally required.

- Collision insurance: Covers damage to your own vehicle regardless of fault.

- Comprehensive insurance: Covers non-collision-related losses, such as storm damage, theft, or fire.

If you’re driving across state lines, you can’t afford to skip any of these, especially comprehensive coverage. People often think they won’t need it if they usually park in their own garage, but during a road trip, you'll be in unfamiliar areas with far more risk.

1.2 Why UM/UIM Is the Best Add-On I Ever Bought

Next, let me share a real case I found on the ConsumerReports.org forum. One user shared her experience:

“Last summer, my family and I drove from Portland to San Francisco. We stopped at a red light on Highway 101, and suddenly, a car rear-ended us with great force. The impact completely crushed our car’s trunk, and my child and I had to go to the ER. To make matters worse, the driver got out and admitted he didn’t have insurance.”

“I was horrified, thinking that I’d have to cover all the repair and medical costs. But when I called my insurance company, the claims agent told me that my policy included UM (Uninsured Motorist) coverage, which covered the situation. In the end, my insurance company paid over $15,000 for repairs and medical expenses. I later found out that if I hadn’t had UM coverage, I would’ve had to pay for everything myself.”

What is UM/UIM? In simple terms:

- UM (Uninsured Motorist): Covers your damages if the other driver doesn’t have insurance.

- UIM (Underinsured Motorist): Covers the gap if the other driver’s insurance is not enough to cover your damages.

After looking into it, I found that about 15% of drivers nationwide are uninsured, and in some states, that number can be as high as 30%. That means one out of every six cars you encounter could be uninsured.

My advice: your UM/UIM coverage should be the same amount as your liability coverage. For example, if your liability coverage is $100,000/$300,000 (single person/single incident), your UM/UIM coverage should match that. It only costs a few extra dollars each month, but it could save you thousands or even tens of thousands of dollars in a crisis.

2. Which Add-Ons Are Actually Worth Buying? The Honest Truth After My Own Experience

2.1 Roadside Assistance — The Day I Got a Flat Tire in Colorado

Last year, I drove from Denver to Utah to visit Arches National Park, and on a highway in Colorado, I suddenly got a flat tire. There was no nearby town, and my phone signal was spotty. I tried for a while but couldn’t get the spare tire on. Fortunately, before I left, I’d bought the roadside assistance add-on for about $50, and within 20 minutes, a tow truck arrived and took me to the nearest town to get a new tire. The tow fee alone saved me at least $300.

For cross-state driving, I think roadside assistance is the most cost-effective add-on. It usually covers:

- Towing (with a mileage limit, like 10 miles free, with extra charges beyond that)

- Tire change (if you can’t do it yourself)

- Fuel delivery (if you run out of gas)

- Lockout service (if you lock your keys in your car)

If you already have AAA membership, roadside assistance might already be included, so you don’t need to buy it again. But if you don’t have AAA, this add-on is a lifesaver for long road trips. In remote areas, just one tow fee can cover the cost of years of this insurance.

2.2 Rental Car Reimbursement — The Incident in Boston That Saved Me from Being Stranded

On a TripAdvisor forum, I found a post from a user sharing their experience:

“I rented a car in Boston and drove to Maine. While backing up at a gas station, I scraped a pillar, cracking the rear bumper. The rental company said it would take about four days to repair the car. I panicked, thinking, ‘How will I get back to work without a car?’ Then I remembered I had purchased rental car reimbursement insurance, which reimbursed up to $40 per day for a total of $1,200. I rented a similar car for four days, and it hardly cost me anything.”

Rental car reimbursement insurance is simple: if your car is in the shop for repairs due to a covered accident, the insurance will pay for a rental car, so you can still get around.

Note:

- There’s usually a daily limit, typically $30-$50 per day.

- There's also a total limit, usually $900-$1,500.

- It only applies if your car is in the shop for an insurance-covered incident.

If your trip requires constant use of your car (for example, if you're visiting several cities or staying in remote places), it’s worth getting this add-on. However, if you’re just driving one-way to your destination and public transport is convenient, you might not need it.

2.3 MedPay/PIP — The “Lifesaver” Money That Many People Overlook

Here’s a real story I came across on Reddit's r/Insurance:

“Last year, I was driving from Texas to New Mexico, and I got rear-ended by someone running a red light in Albuquerque. While the other driver’s liability insurance covered most of the medical bills, there were still over $1,000 in out-of-pocket expenses and several weeks of lost wages that weren’t covered. I later learned that if I had bought PIP (Personal Injury Protection), these expenses would have been reimbursed. I ended up paying nearly $4,000 out of pocket just because I didn’t want to pay for a small PIP policy.”

MedPay and PIP differences:

- MedPay: Covers only medical expenses, not other costs.

- PIP: Covers medical expenses, lost wages, and even personal services like home care.

Note: Some states are "no-fault" states, where PIP is mandatory. States like Florida, Michigan, New York, New Jersey, and Pennsylvania require PIP. If you’re driving through these states, make sure your coverage is sufficient.

If you already have good health insurance, you might be able to get MedPay with a low limit. But if you have a high deductible health insurance plan or are driving through a no-fault state, I recommend buying PIP. It may cost you an extra $10-$20 a month, but in the event of an accident, it could save you thousands.

3. My Add-On Purchasing Strategy — Which Expenses Are Worth Paying, Which You Can Skip

3.1 How to Choose Your Deductible? I Did the Math

First, what is a deductible? It’s the amount you pay before the insurance kicks in. For example, if your deductible is $500 and the repair costs $2,000, you pay the first $500, and the insurance company pays the remaining $1,500.

I used to think that the higher the deductible, the more money I saved, so I chose a $1,000 deductible. I figured I’m a careful driver. But one time, when my car was rear-ended in a parking lot, repairs cost $1,200, and the insurance only paid $200, leaving me with the $1,000 deductible to pay.

After calculating, I realized that I spent more on the policy than the $1,000 I saved on the deductible. Now, I’ve lowered my deductible to $500, and it feels much better because I don’t have to worry about a large out-of-pocket expense.

I did a simple "break-even analysis":

Assuming a $100 difference in premium between the $500 and $1,000 deductible:

- If you go three years without an incident, you save $300.

- But if you have one incident in three years, you pay an extra $500.

If you have a solid emergency fund (at least enough to cover $1,000-$2,000), you might opt for the higher deductible to save on premiums. But if you don’t have enough funds, a lower deductible is safer.

3.2 Which Add-Ons I Think You Can Skip

GAP Insurance: This is useful if you finance your car and owe more than it’s worth. But financial expert Dave Ramsey suggests: instead of buying GAP insurance, pay a higher down payment or pay off the loan faster. If your loan amount doesn’t exceed 80% of the car’s value, you probably don’t need GAP insurance.

Mechanical Breakdown Insurance: This covers repairs for mechanical failure, but after doing the math, I realized the premiums usually exceed the repair costs. My solution is to save for an “emergency car repair fund” by setting aside $50-$100 a month. It’s cheaper in the long run than paying for this insurance.

Glass Insurance: I used to buy it, but then I realized replacing a windshield costs $300-$500, while the annual premium for glass insurance was $50-$100. If you’re not replacing the glass every year, you might as well pay out of pocket.

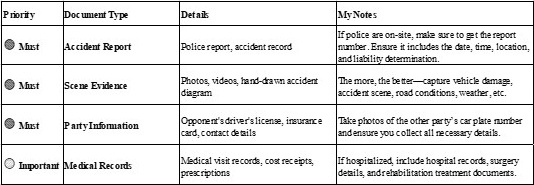

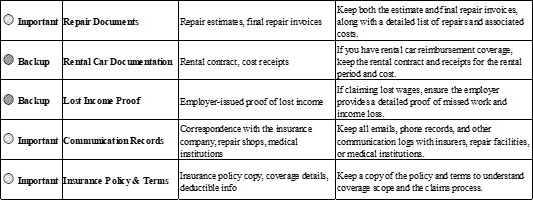

4. What to Do If an Accident Happens? My Claims Document Checklist

4.1 How Should I Handle the Accident Scene?

I had an accident in San Francisco once, and the other driver immediately denied responsibility, saying, “You swerved into my lane.” Instead of arguing, I took pictures of the scene, recorded the location of nearby security cameras, and found a witness in a nearby store. In the end, I got the police report, and when I submitted all this evidence, the insurance company immediately sided with me.

I later asked a friend who works in claims about the process, and he gave me a checklist of what to do at the scene. I’ve organized it here:

Step 1: Safety First

If anyone is injured, call 911. Move the vehicle to a safe place, and if it can’t move, turn on your hazard lights and put out warning triangles.

Step 2: Gather Information (This is crucial)

- The other driver’s license: Take a photo or write down their name, address, and license number.

- The other driver’s insurance card: Make sure to take a picture, especially the policy number and insurance company contact.

- The other driver’s license plate: Take clear photos.

- Accident scene: Take photos from multiple angles—damage to the vehicles, road conditions, weather, and traffic signs.

- Witnesses: If anyone saw the accident, get their contact info.

A Tip I Use: Now that phones have memo or notes functions, I created an “Accident Record” template with all the information I need to ask the other party. Before heading out on a trip, I review it, so if anything happens, I won’t be caught off guard.

Contact the Insurance Company as Soon as Possible

My advice: the sooner, the better. If it’s safe at the scene, call immediately. If not, make sure to call that same day, no later. Some people share their experience of waiting two days before calling, and the insurance company questioned why they didn’t report it sooner. Although the claims were processed in the end, it added delays and extra steps.

Here’s My Current Insurance Setup for Your Reference

Core Coverage:

- Liability Insurance: $100,000/$300,000 (Single/Per Incident)

- UM/UIM: $100,000/$300,000 (Matching the Liability Coverage)

- Collision Insurance: $500 Deductible

- Comprehensive Insurance: $500 Deductible

Add-On Insurance:

- Roadside Assistance: Must-buy

- Rental Car Reimbursement: Buy for long road trips, can cancel otherwise

- PIP: Mandatory in No-Fault States

Monthly Premium:

Approximately $150-$180 (Depending on car model and driving record)

At the end of the day, insurance is about preparing for the unknown. You might drive for ten years without an accident, or you might get rear-ended by an uninsured driver on the first day of your trip. The point of insurance is not to use it, but to ensure that if you do need it, you’re not financially ruined.

Wishing you safe travels and happy driving!

References

1. National Association of Insurance Commissioners. (2024). Auto insurance consumer guide. Retrieved from [https://content.naic.org]

2. Consumer Reports. (2023). What does car insurance cover?. Retrieved from [https://www.consumerreports.org]

3. AAA. (2023). Your guide to roadside assistance coverage. Retrieved from [https://www.aaa.com](https://www.aaa.com)

4. Kaiser Family Foundation. (2023). Health insurance coverage and out-of-pocket costs in the U.S. Retrieved from [https://www.kff.org]

About the Author

Ethan Walker

Ethan Walker is a U.S.-based automotive insurance researcher and long-distance driving enthusiast. With years of personal experience in cross-state road trips across the United States, he specializes in breaking down complex insurance policies into practical, real-world guidance for everyday drivers.

Editorial Transparency Statement

The content is intended for informational use only and does not constitute legal or insurance advice. Insurance policies, coverage requirements, and claim procedures may vary by state and provider. Readers are encouraged to consult licensed insurance professionals or official policy documents for specific guidance.

No insurance companies or financial institutions have influenced the content of this article.

Disclaimer

The information in this article should not be considered professional insurance, legal, or financial advice. Insurance coverage, exclusions, and eligibility vary widely depending on the provider, jurisdiction, and individual circumstances.

Recommended for you