How to Choose Short-Term Road Trip Insurance for Popular Routes in the US and Europe

——Comparing Coverage Options, Costs, and Practical Tips for Multi-Region Travel Protection

By Jonathan Miller | Updated on March 24, 2026 | 🕓 15–18 minutes

Key Highlights

- Understanding the difference between travel insurance (covers the person) and vehicle insurance (covers the car).

- Critical US vs Europe insurance considerations including medical costs, rental coverage, and credit card limitations.

- Practical strategies for optimizing coverage and minimizing costs.

- Step-by-step accident handling procedures for both medical emergencies and vehicle incidents.

- Real-world case studies illustrating cost-saving and emergency coverage benefits.

In April 2024, an American tourist rented a car for a day trip in Lisbon. On the way back, he discovered damage to the rear of the car. Confidently, he refused the rental company’s insurance—because his American Express card included Collision Damage Waiver (CDW). As a result, the rental company charged him €1,205, while the credit card company’s claim requirement was to provide a “repair invoice.” He made eight phone calls and waited eight months, eventually only receiving a refund after media intervention.

In the same year, another renter was not so lucky. He had a minor collision on a French highway, and Avis billed him $7,671 for “loss of use”—calculated as the maximum daily rental rate for a full 29-day rental period. Even though the accident was not his fault and his insurance theoretically covered “loss of use,” the rental company’s invoice only stated “29 days rental fee,” not “loss of use compensation,” causing the insurance company to reject the claim.

These two stories reveal a harsh truth: when driving in the US or Europe, mistakes in insurance configuration can cost thousands or even tens of thousands of dollars. The core issue is that most travelers cannot distinguish between “insurance for the person” and “insurance for the car,” and they are unaware of the huge gap between the two.

A. Core Concept Explanation: Travel Insurance vs Vehicle Insurance

Travel Insurance — Insures the Person

Travel insurance primarily covers you—the insured individual—including your health, personal property, and smooth progress of your trip.

Why purchase separately?

Non-US/EU residents have no local health coverage while traveling abroad. Medical costs in the US and Europe are among the highest in the world: in the US, an emergency room visit starts at around $1,500, with hospitalization at $5,000–$10,000 per day; in Europe, while somewhat cheaper, an acute appendicitis surgery with hospitalization can still cost €10,000–€20,000.

Recommended coverage limits (by destination)

For Schengen visa purposes, a minimum coverage of €30,000 is required, but this is only the minimum and insufficient for serious hospitalization costs.

Key coverage items

Accident medical expenses: Treatment costs for traffic accidents, falls, and other accidental injuries.

Acute illness medical expenses: Sudden illnesses (appendicitis, heart attacks, food poisoning). Make sure the policy covers this and check exclusions for “acute flare-ups of pre-existing conditions.”

Emergency medical evacuation: Helicopter rescue or air ambulance transport—critical in remote areas (US national parks, Alpine regions), with single-trip costs reaching $20,000–$50,000.

Personal liability: Coverage for injuries or property damage you cause to others (e.g., hitting a pedestrian).

Trip cancellation/interruption: Compensation for non-refundable expenses if unexpected events prevent continuation of the trip.

Cost reference (7–14 days short-term travel)

US: $50–$150

Europe: €30–€80

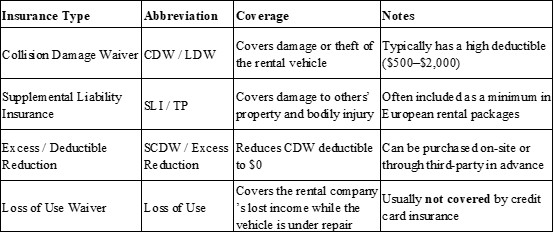

Vehicle Insurance — Insures the Car

Vehicle insurance covers the car itself and damages you may cause to third parties.

Core coverage for rental cars

Insurance configuration for personal/local vehicles

If you are driving your own car or a friend’s/local vehicle in the US or Europe:

Third-party liability: Legally required. Recommended coverage $300,000–$1,000,000 (US) or €1,000,000+ (Europe).

Collision damage coverage: Covers vehicle damage, not mandatory but strongly recommended.

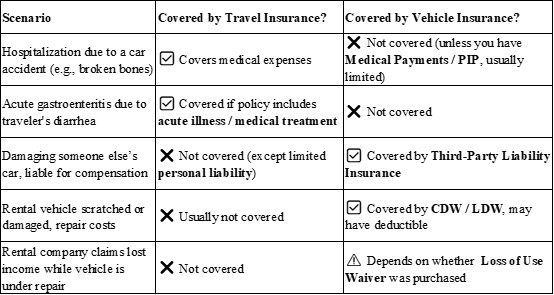

Passenger insurance: Covers medical costs for passengers in the vehicle—vehicle insurance pays first; travel insurance covers any excess.

Key reminder: they are not interchangeable

Travel insurance covers the person, vehicle insurance covers the car—both are essential.

B. Destination Differences: US vs Europe

🇺🇸 Key Points for US Road Trips

High medical costs

The US has the highest medical costs globally. An uninsured emergency visit can easily exceed $5,000; hospitalization can range $20,000–$50,000. Therefore, travel insurance medical coverage should not be less than $500,000, with $1,000,000 being safer.

Rental car insurance features

- Basic rental packages often exclude third-party liability; it must be purchased separately.

- CDW deductibles are usually high ($500–$2,000).

- Loss of Use is a common dispute—the rental company calculates the “loss” during repair at the maximum daily rate, often not covered by credit card insurance.

State law differences

Insurance requirements vary by state. For example:

- California: recognizes foreign licenses; minimum third-party liability required.

- Texas: requires International Driving Permit (IDP) and higher liability coverage.

Credit card insurance applicability

US credit card rental car coverage generally works well domestically, with smoother claims.

🇪🇺 Key Points for European Road Trips

Schengen visa requirement

Traveling to the 26 Schengen countries requires travel insurance with at least €30,000 coverage and global emergency assistance.

Rental car insurance features

Basic rental packages include minimum third-party liability (usually €1,000,000–€5,000,000).

CDW deductibles are high, but Super CDW (SCDW) or third-party excess reimbursement can be purchased in advance at a fraction of the rental company’s price.

Cross-border travel: check coverage validity—France to Italy is usually fine; entering non-EU countries (UK, Croatia, Morocco) may require extra coverage.

Credit card insurance limitations

Europe has a high incidence of credit card rental disputes:

- Some countries (Italy, Ireland) limit coverage based on engine size.

- Luxury cars, convertibles, and large SUVs are often excluded.

- Rental companies may not provide the “repair invoice” required by credit card insurers.

- Claims processing can take months.

UK specifics

Post-Brexit, the UK has right-hand drive vehicles. Short-term driving with an IDP is usually allowed, but insurance must cover right-hand drive risks.

C. Practical Tips and Cost Optimization

1. Purchase sequence and combination strategy

Optimal combination:

- Purchase travel insurance in advance (with $500K/€50K medical + emergency evacuation)

- Confirm credit card rental coverage (destination coverage, primary/secondary, Loss of Use included)

- Purchase third-party excess reimbursement (ERI / Excess Reimbursement) online in advance

- At the rental counter: decline CDW/SCDW upsell, but ensure third-party liability is sufficient

Why this configuration?

A Which? survey shows that on-site SCDW averages £177/week, while equivalent third-party ERI coverage costs £23–£38—4–12 times cheaper, often with broader coverage.

Tip: Purchase travel insurance before departure; post-departure purchase is usually ineffective.

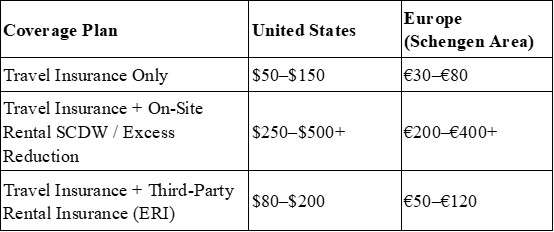

2. Cost reference

7–14 days short-term road trip insurance total cost (USD/EUR):

Money-saving key: Purchase third-party excess reimbursement online rather than at the rental counter.

3. Accident handling procedures

Medical emergency

- Seek immediate care and contact your 24-hour travel insurance emergency hotline—do not promise to pay large amounts yourself.

- Keep all documents: diagnoses, prescriptions, receipts, medical reports.

- For evacuation (e.g., helicopter), authorization from the insurance company is required, or the claim may be denied.

Vehicle accident

- Take photos: six angles covering damages, license plate, odometer, and surrounding reference points.

- Report to the police: obtain accident report including witness info.

- Contact rental company: notify within 24 hours for instructions.

- Submit claim: include police report, rental contract, repair invoice, and payment receipts.

Key reminder: 78% of insurance claim denials occur because full accident photos were not taken. Ensure comprehensive documentation before moving the vehicle.

D. Case Studies: Real Scenarios vs Policy Terms

Case 1: Minor highway collision in France—how third-party ERI saved €1,200

Emma rented a car in France and purchased €25 ERI in advance from a third-party platform, covering €2,000 deductible.

While reversing at a highway service area, she lightly scraped the rear bumper. Upon return, the rental company charged €1,200 from her credit card. After submitting rental contract, repair invoice, and payment proof to the third-party insurer, she received full reimbursement within two weeks.

Had she purchased SCDW on-site, she would have paid ~€199 with less coverage.

Case 2: Helicopter rescue—$48,000 emergency covered by travel insurance

A Canadian tourist experienced severe chest pain while hiking in Grand Canyon National Park. A helicopter transported him to Las Vegas hospital, diagnosed with acute myocardial infarction.

Costs: helicopter $48,000, hospitalization $127,000, total $175,000.

He had pre-purchased $1,000,000 travel insurance covering emergency evacuation and acute illness. The insurer settled directly with hospital and rescue company; the tourist paid only a $250 deductible.

In remote road trips, emergency evacuation coverage can be a lifesaver.

E. Comprehensive Recommended Strategy: Standard Configuration for Non-US/EU Residents

Optimal plan (by priority):

First layer: Travel insurance (mandatory)

- Medical coverage: US ≥$500,000 / Europe ≥€50,000

- Must include: acute illness coverage, emergency medical evacuation, 24-hour global assistance

- Recommended: personal liability, trip cancellation/interruption, lost luggage

- Purchase time: before departure

- Cost: $50–$150 / €30–€80

Second layer: Vehicle insurance — rental scenario (mandatory)

- Third-party liability: confirm sufficient coverage (Europe ≥€1,000,000)

- CDW: accept basic deductible but—

- ERI: purchase in advance via third-party platform ($10–$20/day) covering deductible

- Credit card rental coverage: supplemental, not replacement; confirm:

Covers destination country

Does not exclude luxury/specific vehicles

Requires refusal of rental CDW

Includes Loss of Use

Third layer: Vehicle insurance — personal/local vehicle (optional as needed)

- Third-party liability: recommended $500,000+ / €1,000,000+

- Collision damage coverage: strongly recommended

- Passenger insurance: if absent, ensure each passenger has adequate travel insurance

Plan in advance, configure separately, and decline on-site upsells. This saves hundreds of dollars and ensures coverage when truly needed.

Appendix: Quick Reference Tables

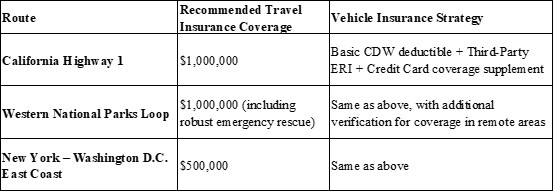

Recommended configuration for popular US routes

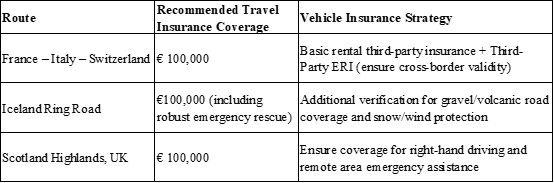

Recommended configuration for popular European routes

References

1. Allianz Global Assistance. (2023). Travel insurance coverage guide. Retrieved from [https://www.allianztravelinsurance.com]

2. American Express. (2024). Car rental insurance benefits. Retrieved from [https://www.americanexpress.com/benefits/rental-car-insurance]

3. Which? Consumer Reports. (2023). Car rental insurance comparison: SCDW vs ERI. London, UK: Which? Publications.

4. US National Safety Council. (2022). Costs of motor vehicle accidents and emergency care in the US. Retrieved from [https://www.nsc.org]

5. European Consumer Centre. (2023). Cross-border car rental insurance disputes in Europe. Brussels, BE: ECC Network.

About the Author

Jonathan Miller

Jonathan is a travel insurance analyst and freelance writer specializing in international travel risk management. With over 8 years of experience in both US and European travel insurance markets, he provides practical guidance for travelers, including expatriates and short-term tourists. He has consulted for rental car platforms, insurance brokers, and travel publications, helping readers optimize coverage for multi-country road trips.

Editorial Transparency Statement

This article is independent and research-based. The author has no direct financial interest in any insurance provider mentioned. Recommendations are based on publicly available data, industry reports, and real-world examples shared by travelers. Third-party products referenced (e.g., ERI, credit card insurance) are used illustratively and not endorsed for commercial gain.

Disclaimer

The information in this article should not be considered professional insurance, legal, or financial advice. Insurance coverage, exclusions, and eligibility vary widely depending on the provider, jurisdiction, and individual circumstances.

Recommended for you