What Are the Common Exclusions Often Overlooked in Cross-Border Rental Car Insurance for Europe?

——How to Choose the Most Affordable Short-Term Rental Insurance for Your European Road Trip

By Lucas Bennett | Updated on March 24, 2026 | 🕓 10–12 minutes

Key Highlights

- Core insurance types and how deductibles (excess) really work

- Cross-border driving rules and country-specific coverage differences

- 7 commonly overlooked exclusions that can void your insurance

- Real-world cases: what actually leads to claim denials

- Cost comparison: rental company insurance vs third-party coverage

Why Is Car Rental Insurance in Europe So Complicated?

The appeal of driving in Europe is undeniable—from Germany’s no-speed-limit autobahns, to the rolling hills of Tuscany in Italy, to the mountain passes of the Swiss Alps. Every stretch of road offers breathtaking scenery.

But cross-border driving also means dealing with: differences in traffic laws between countries, varying road conditions, language barriers, and complex insurance terms.

The deductible (excess) for car rental insurance in Europe typically ranges from €850 to €15,000. This means that even if you have insurance, you may still need to pay a significant amount out of pocket in the event of an accident. Worse, if you violate certain exclusion clauses, the insurance may refuse to pay anything at all.

Part 1: Basics of Cross-Border Car Rental Insurance in Europe

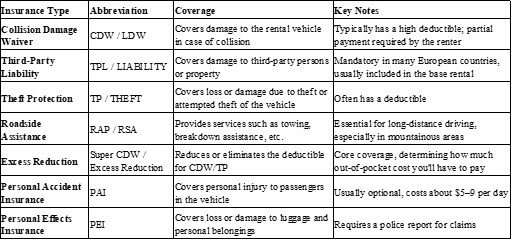

1.1 Common Types of Insurance

When booking through rental platforms or at the rental counter, you will typically encounter the following types of insurance:

Deductible / Excess

This is the threshold you must pay before insurance coverage kicks in. For example, if your deductible is €1,800:

² Repair cost €1,000 → You pay all

² Repair cost €5,000 → You pay €1,800, insurance pays €3,200

1.2 Cross-Border Applicability: Which Insurance Works in Different Countries?

Minimum Third-Party Liability Requirements (under EU legal framework):

² Germany: Unlimited third-party liability (mandatory, included in rental price)

² France: Typically requires a minimum of €5 million

² Italy: Requires €5–10 million minimum coverage

Deductible Differences (based on Hertz data):

² Most European countries: €850–€15,000

² USA/Canada: Typically €0

² Australia/New Zealand: AUD/NZD 5,900–7,900

If you plan to drive across borders, you must confirm in writing at pickup which countries are permitted. Some rental companies prohibit entry into Eastern European countries (e.g., Bulgaria, Romania) or specific islands (e.g., Sicily, Sardinia).

Driving into restricted regions will automatically void your insurance.

Part 2: Commonly Overlooked Exclusions — Each with Real Cases

2.1 Prohibited Roads: “The Cost of a Gravel Road”

A traveler in Tuscany was guided by GPS onto an unpaved gravel road. Stones damaged the suspension system. The rental company refused coverage due to “driving on prohibited roads,” resulting in a €3,200 bill.

Most contracts explicitly prohibit driving on:

² Gravel roads

² Off-road/unpaved routes

² Closed roads

² Agricultural roads

CDW (Collision Damage Waiver) only applies to approved public roads. Entering roads listed under “Prohibited Roads / Restricted Use” voids coverage.

How to avoid:

² Check the “Prohibited Roads” clause in your contract

² Use Google Street View to preview road conditions

² When in doubt, take a longer paved route

2.2 Water Crossing: “The Rainstorm Trap”

A traveler attempted to drive through shallow floodwater in southern France. The engine flooded, resulting in €6,800 in repairs. The insurer denied the claim as “driver negligence.”

Most policies exclude engine damage caused by water entry—even under Super CDW.

Typically, water reaching above the wheel hub is considered negligence.

How to avoid:

² Never drive through flooded roads

² Avoid underground parking during heavy rain

² Ask about flood/natural disaster coverage if driving in rainy seasons

2.3 Misfuelling: “The Fuel Cap Mistake”

A traveler in Germany mistakenly filled a petrol car with diesel. After a few kilometers, the engine failed. Repair costs exceeded €5,000, fully charged to the renter.

Almost all policies exclude “misfuelling” because it is considered driver error, not an accident.

How to avoid:

² Confirm fuel type at pickup

² Take a photo of the fuel cap label

² Ask: “Does Super Cover include misfuelling?” (some premium plans do)

2.4 Unauthorized Driver: “The Cost of Switching Drivers”

A couple traveling in Europe switched drivers mid-trip without registering the second driver. After an accident, the insurer denied all claims. Total loss: €15,000.

Insurance only covers drivers listed in the contract. Any unregistered driver voids coverage—even if not at fault.

How to avoid:

² Add all potential drivers as “Additional Drivers”

² Cost: €5–15/day/person

² Ensure they meet license requirements (usually 1–2 years minimum)

2.5 Parking Damage & Theft: “The Paris Scratch”

A traveler parked on the street in Paris and returned to find scratches. The rental company denied coverage due to “unsafe parking conditions.”

Common restrictions include:

² Must park in legal, safe areas

² Some policies require secured parking for theft coverage

² Minor damage without a responsible party may not be covered

How to avoid:

² Use secured indoor parking in cities

² Keep parking receipts

² Confirm coverage for unattended parking situations

2.6 Traffic Violations: “The High-Speed Consequence”

A driver in Germany traveled at 180 km/h but failed to maintain safe distance, causing a rear-end collision. Insurance denied the claim due to “serious traffic violation.”

Common exclusions include:

² DUI or drug driving (absolute exclusion)

² Excessive speeding (30+ km/h over limit)

² Fatigue driving (over 4 hours without rest)

² Failure to maintain safe distance

How to avoid:

² Follow local traffic laws

² Even on German autobahns, recommended speed is 130 km/h

² Use navigation apps with speed alerts

2.7 Gross Negligence: “The Hidden Killer Clause”

In September 2025, a traveler renting in Sicily was charged €22,180 after an accident. The rental company claimed “gross negligence,” despite no such finding in the police report.

After legal disputes, the renter eventually paid only the €1,800 deductible.

“Gross negligence” is one of the most controversial clauses. Rental companies may interpret behavior (e.g., poor observation) as negligence and void coverage.

How to avoid:

² Choose large international rental brands over small local firms

² Purchase independent third-party excess insurance

² Keep all communication records

² Check Google reviews for claims reputation

Part 3: Short-Term Rental Insurance Strategy — Maximum Coverage at Minimum Cost

3.1 Match Needs with Coverage

For short trips (1–14 days), core needs typically include:

3.2 Rental Company vs Third-Party Insurance

Rental Company Insurance (counter purchase):

✅ Pros: Easy claims, “return and go” convenience

❌ Cons: Expensive (2–3× higher than third-party)

Third-Party Insurance (pre-booked online):

✅ Pros: Affordable (€15–25/day)

❌ Cons: Requires upfront payment and reimbursement process

2025 Price Reference:

² Daily: €15–25

² Weekly: €45–70

² Monthly: €90–150

Cost-saving strategy:

Buy basic insurance (high deductible) + third-party excess insurance → €10–20/day, over 50% cheaper than zero-excess plans at the counter.

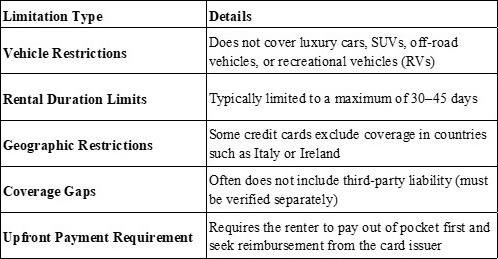

3.4 Credit Card Insurance: “Looks Free, Comes with Limits”

Many premium credit cards offer rental insurance, but with significant limitations.

Recommendation: Use credit card insurance as a supplement, not primary coverage. Always confirm terms with your bank before travel.

3.5 Recommended Cost-Effective Combinations

For short intercity road trips (such as driving between Paris, Brussels, and Amsterdam for 3–7 days), choosing “basic rental insurance + third-party excess insurance” is usually sufficient. These routes typically have well-developed road conditions and clear traffic regulations, with a relatively low probability of serious accidents. By using third-party insurance to offset a high deductible, you can keep daily costs around €10–15 while maintaining solid coverage—making it a highly cost-effective option.

For rural or mountainous driving scenarios (such as in Tuscany or the Alps for 7–10 days), risks increase significantly. Narrow roads, sharp turns, gravel surfaces, and sudden weather changes can all raise the likelihood of accidents or breakdowns. In this case, it is recommended to add roadside assistance insurance on top of “basic insurance + third-party excess coverage.” Although the daily cost increases to €15–25, a single towing or rescue service in remote areas can easily exceed the total insurance cost—making this coverage a true “lifesaver.”

For long-distance, multi-country road trips (such as traveling through Germany, Austria, Italy, and France over 10–20 days), the overall risk exposure increases due to varying traffic laws, complex road conditions, and longer driving durations. In this scenario, it is often more practical to choose the rental company’s zero-excess full coverage (commonly referred to as “Premium Protection”). Although the daily cost is higher (€25–45), the key advantage is convenience—after an accident, you can typically return the vehicle without dealing with complicated claims, saving both time and stress.

Finally, if you are a frequent renter (renting a car three or more times per year), an annual excess insurance policy is usually the most cost-effective long-term option. With an annual premium of around €80–150, it not only reduces the cost compared to purchasing coverage for each trip but also provides continuous protection across multiple cross-border or domestic journeys—making it especially suitable for travelers who frequently drive in Europe or take multi-segment trips.

Final Pre-Pickup Checklist

〇 Confirm “Excess €0” or “Zero Excess” in contract

〇 Record a full vehicle inspection video

〇 Verify cross-border permissions in writing

〇 Confirm fuel type (take a photo)

〇 Register all drivers

〇 Check rental company reviews (avoid ratings below 4.0)

Final Reminder

The core logic of European rental car insurance is this:

You are buying probability of coverage—not zero risk.

Those small-print exclusion clauses are often the rental company’s legal way to limit payouts.

Understanding the terms, choosing the right insurance combination, driving carefully, and keeping proper documentation—these four steps are the key to truly stress-free driving in Europe.

FAQs

1. Is zero-excess insurance always worth it in Europe?

Not necessarily. For short trips in low-risk areas, combining basic insurance with third-party excess coverage is often more cost-effective. Zero-excess plans are more suitable for long or complex cross-border trips.

2. Does my credit card rental insurance cover cross-border driving in Europe?

Sometimes—but often with restrictions. Many policies exclude certain countries, vehicle types, or require you to decline the rental company’s insurance. Always confirm with your card issuer before travel.

3. What happens if I accidentally drive into a restricted country?

Your insurance may become completely invalid. Any damage, theft, or liability could be fully your responsibility. Always confirm permitted countries in writing at pickup.

4. Are minor scratches and parking damage covered?

Not always. If there is no identifiable third party or if the vehicle was not parked in a “secure” location, the claim may be denied depending on the policy.

5. What is the most common reason for claim rejection?

Driver-related issues—such as unauthorized drivers, misfuelling, or violating traffic laws—are among the most frequent reasons insurers deny claims.

6. Should I rely only on rental company insurance?

Rental company insurance offers convenience but is often expensive. A hybrid strategy (basic insurance + third-party excess) usually provides better value for money.

References

1. European Commission. (2023). Motor insurance in the European Union: Minimum coverage requirements and cross-border protections. Retrieved from [https://ec.europa.eu]

2. European Consumer Centre Network. (2022). Car rental in Europe: Key consumer rights and common pitfalls. Retrieved from [https://www.eccnet.eu]

3. Hertz. (2024). Terms and conditions of rental and insurance coverage in Europe. Retrieved from [https://www.hertz.com]

4. Association of British Insurers. (2023). Guide to car hire excess insurance and exclusions. Retrieved from [https://www.abi.org.uk]

5. Consumer Reports. (2024). Rental car insurance: What you need to know before you travel. Retrieved from [https://www.consumerreports.org]

About the Author

Lucas Bennett

Lucas Bennett is an independent travel risk analyst and insurance researcher with over 8 years of experience studying cross-border mobility and vehicle insurance systems in Europe and North America.

Having personally completed multiple self-driving trips across the Schengen Area, Lucas combines real-world driving experience with policy analysis. His insights are also informed by case studies from global travel forums and consumer complaint databases, offering practical, experience-driven guidance rather than purely theoretical advice.

Editorial Transparency Statement

This article is independently researched and written based on publicly available insurance policy documents, official regulatory guidelines, and real-world case studies reported by travelers.

- No sponsorship or financial incentives influenced the content

- All recommendations are based on risk analysis and cost-efficiency

- Readers are encouraged to verify specific terms directly with rental companies or insurers before purchase

Disclaimer

The information in this article should not be considered professional insurance, legal, or financial advice. Insurance coverage, exclusions, and eligibility vary widely depending on the provider, jurisdiction, and individual circumstances.

Recommended for you