How to Purchase Cross-Border Auto Insurance for Travel in the US, Canada, and Mexico

——Step-by-Step Guide to Claims and Common Pitfalls That Could Lead to Denial

By Daniel Mercer | Updated on March 24, 2026 | 🕓12–15 minutes

Key Highlights

- Route Planning Across the US, Canada, and Mexico

- Key Differences in Insurance Coverage Between the Three Countries

- How to Purchase Valid Insurance for Mexico (and Avoid Overpaying)

- Essential vs Optional Coverage: What You Really Need

- Common Blind Spots That Can Lead to Claim Denials

- Practical Pre-Trip Checklist for Cross-Border Drivers

I’m a self-driving travel enthusiast. Last autumn, I made a decision that many of my friends thought was a bit crazy—I drove alone across the United States, Canada, and Mexico on a true “North American Grand Loop” road trip.

To be honest, the idea at first was simple. I wanted to watch the Pacific sunset along California’s Highway 1, experience the breathtaking autumn scenery of the Canadian Rockies, and taste authentic street tacos in Mexico. Three countries, three completely different landscapes and cultures—all in one journey. Just thinking about it was exciting.

But once I started planning, I realized how “naive” that idea was. The first major headache? Cross-border auto insurance.

Although the US, Canada, and Mexico are geographically connected, their insurance systems are like three completely different worlds. My US policy could still work in Canada, but once I entered Mexico, it would become completely useless. I read stories on forums about people who got into accidents in Mexico without local insurance—having their cars impounded, being stuck at the border for days, and eventually paying fines several times higher than the insurance cost just to get out.

Those stories made me nervous.

From initial confusion to reading dozens of forum posts and making over ten phone calls, I finally figured everything out. Today, I want to share my full experience to help you avoid the same mistakes.

My Route Plan: Where I Went and How Long

I planned a 28-day itinerary—not overly long, but enough for a classic loop:

Days 1–10: United States

Depart from Los Angeles, drive north along Highway 1, pass through San Francisco and Portland, and reach Seattle.

Days 11–15: Canada

Enter Vancouver from Seattle, head east to Banff National Park, then return south.

Days 16–28: Mexico

Enter Mexico from San Diego, travel through Tijuana and Ensenada, and go deeper into the Baja California Peninsula.

I chose late September. The US West Coast and Canadian Rockies are stunning in autumn, while Baja California has mild weather—not too hot.

Both US–Canada and US–Mexico borders have well-established crossing points. I deliberately avoided busy urban crossings and chose less crowded but more efficient ones.

For insurance, my US policy covered Canada (which I confirmed in advance), but I needed separate insurance for Mexico. My route made the “insurance switch” easier—I had enough time before entering Mexico to arrange coverage in a border city.

Driving Tips

In Mexico, right turns on red are usually prohibited unless there is a “Derecho en Rojo” sign. I almost made a habitual right turn in Tijuana—luckily, my passenger stopped me.

Mexico also has a dedicated roadside assistance team for travelers called “Ángeles Verdes.” They wear green uniforms and provide free help. I saved their number in my phone—recommended by an experienced driver from a forum.

Parking and Navigation

United States:

Parking in big cities is expensive and hard to find. I usually used ParkWhiz or SpotHero to reserve in advance. Always check street cleaning schedules—tickets are common.

Canada:

More user-friendly. Parking is abundant in places like Banff, but during peak season, arriving early is still recommended.

Mexico:

Street parking is often free in small cities, but in large cities, paid parking is safer. Most hotels I stayed at offered parking—paid, but worth the peace of mind.

For navigation, I downloaded offline maps for all three countries. Google Maps worked well in the US and Canada, but in Mexico, I found Waze more accurate for real-time updates, especially for police checkpoints and construction alerts.

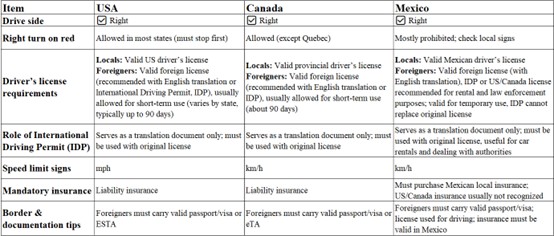

Insurance Considerations

At first, I naively thought “one international policy would be enough.” After a few days of research, I realized it was far more complicated.

My US insurer told me the policy automatically covers Canada, as long as I carry the “Canada Non-Resident Inter-Province Motor Vehicle Liability Card.”

But when I asked about Mexico, the answer was clear:

“Sir, our policy is not valid in Mexico. You need to purchase local insurance.”

So I began researching Mexican insurance.

The most important takeaway:

Do not cheap out with basic liability-only coverage.

One forum user shared a painful story—he only bought liability insurance, lost control after a tire blowout, and crashed into a guardrail. The damage was nearly $10,000, but since he didn’t have collision coverage, he paid everything out of pocket.

I initially planned to buy insurance at the border through rental companies—it seemed convenient. But after comparing prices, I found their rates were nearly double those online, and they often bundled unnecessary add-ons.

In the end, I purchased a full-coverage policy online from a Mexican insurer (GNP), including liability, collision, theft, and medical coverage.

- Cost: $28/day

- Rental counter price: $55/day

Almost half the price.

“Don’t buy Mexican insurance after crossing the border.”

Border agents can be unreliable, and some even sell fake policies. Buying online in advance and printing the documents is the safest option.

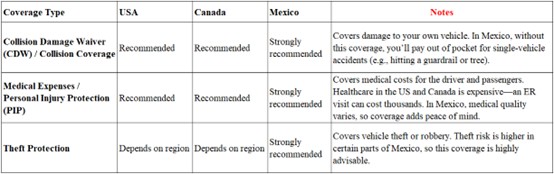

What Insurance Do You Actually Need?

First, liability insurance is mandatory in all three countries. It covers damage or injury to others caused by you.

Mexico has particularly strict requirements—high coverage limits (e.g., 300,000 pesos or more) are recommended.

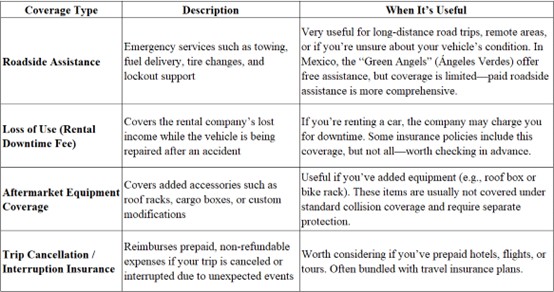

Second, the following are not legally required but essential:

Finally, these optional coverages depend on your budget:

Common Blind Spots

During research and purchase, I discovered several easily overlooked issues:

- Not all Mexican policies cover the entire country. Some only cover the “free zone” within 100 km of the border. If traveling inland, ensure nationwide coverage.

- Save the 24-hour assistance number—on your phone and written in the car.

- Always call the police in Mexico, even for minor accidents. Without a police report, claims may be denied.

- My premium credit card claimed “global rental coverage,” but Mexico was excluded. Always confirm directly.

- Always read the “Exclusions” section carefully. Common exclusions include:

-Driving on unpaved roads

-Restarting the engine after water damage

-Using the vehicle for commercial purposes

If renting a car, check the deductible—some are as high as $2,000, meaning small accidents come out of your pocket.

On the Road Experience

Driving north from Los Angeles along Highway 1 is one of the most iconic road trips in the US. Roads are excellent, gas stations are plentiful, and navigation is reliable—a perfect “beginner-friendly” segment.

Challenges?

Traffic in Los Angeles and San Francisco is heavy, and parking is expensive. I paid $45 for one night in San Francisco.

Also, US toll roads require preparation—some are cashless, requiring FasTrak or online payment. Missing payments leads to fines.

In Canada, the scenery was breathtaking. The drive from Vancouver to Banff was filled with stunning views of the Rockies.

But there were challenges. By late September, snowfall is possible. I encountered light snow and slippery roads. Fortunately, I had winter tires and drove cautiously.

Canada also has stricter speed enforcement than the US.

Before entering Mexico, I did the most preparation—but still faced surprises.

The toll road (Cuota) from Tijuana to Ensenada is excellent. But once on free roads (Libre), conditions worsen—potholes and sudden speed bumps (“Topes”) appear without warning.

Police checkpoints are common. I encountered two—both routine document checks. I kept all documents organized in a folder, making the process smooth.

Claims Process and Tips

Although I didn’t have a major accident, I did scrape a pillar while reversing in a hotel parking lot in Ensenada.

Since it was a single-vehicle incident with no injuries, I didn’t report it locally. After returning home, I contacted the insurer and submitted:

- Photos of the accident

- Hotel CCTV footage (which I requested)

- Driver’s license and policy copies

- Repair estimate

After completing forms and mailing documents, the claim was processed in about three weeks.

- Total repair cost: ~$800

- Deductible: $500

- Reimbursement: Remaining amount covered

This small accident made me realize the value of proper insurance.

Common Claim Denial Scenarios

From forum cases, I summarized the most common reasons:

1. DUI (Driving Under the Influence)

Absolute red line. No insurance covers illegal behavior. In Mexico, it can also lead to criminal charges.

2. Invalid or Missing Documents

One traveler’s claim was denied because his translated license was not notarized.

3. Failure to Report

In Mexico, always call the police—even for minor incidents. No report = claim denial.

Insurance companies usually require reporting within 24 hours.

4. Improper Vehicle Use

Driving off-road without coverage can result in denial.

Final Thoughts and Tips

- Choose insurance that covers all three countries

- Understand each country’s driving rules

- Pay attention to claim procedures and fine print

Prepare a “border document folder” with:

- Passport

- Driver’s license (original + translation/notarization)

- Vehicle registration

- Insurance documents (separate for US/Canada and Mexico)

- Itinerary

Save emergency numbers for all three countries.

Watch out for Topes in Mexico—they appear suddenly and can cause damage.

I’m glad I did thorough research before the trip—and even more glad that my small accident remained just a minor lesson, not a disaster.

I hope my experience helps you avoid the same pitfalls.

Prepare your insurance, understand the rules, and then—enjoy the road ahead.

References

1. Government of Canada. (2024). Driving in Canada as a visitor. [https://travel.gc.ca/travelling/documents/driving]

2. Transport Canada. (2023). Road safety and motor vehicle regulations. [https://tc.canada.ca]

3. Secretaría de Hacienda y Crédito Público. (2022). Seguro obligatorio de responsabilidad civil vehicular. [https://www.gob.mx/shcp]

4. AMIS (Asociación Mexicana de Instituciones de Seguros). (2023). Auto insurance requirements for foreign vehicles in Mexico. [https://www.amis.com.mx]

5. U.S. Department of State. (2024). Mexico international travel information. [https://travel.state.gov]

6. Consumer Reports. (2023). What your car insurance covers—and what it doesn’t. [https://www.consumerreports.org]

7. AAA (American Automobile Association). (2024). International driving and insurance requirements. [https://exchange.aaa.com]

About the Author

Daniel Mercer

Daniel Mercer is an independent automotive travel writer and long-distance road trip enthusiast specializing in cross-border driving experiences across North America and Europe. With years of hands-on experience in multi-country road trips, he focuses on practical travel logistics, insurance strategy, and real-world risk management for self-driving travelers.

His work is grounded in real travel scenarios, aiming to bridge the gap between policy terms and what actually happens on the road.

Editorial Transparency Statement

This article is based on the author’s personal travel experience, independent research, and publicly available information from insurance providers and user communities.

No insurance company sponsored, reviewed, or influenced the content of this article. All opinions, recommendations, and interpretations are solely those of the author.

Insurance policies, coverage limits, and legal requirements may vary by provider, region, and time. Readers are strongly encouraged to verify details directly with insurers or licensed professionals before making purchasing decisions.

Disclaimer

The information in this article should not be considered professional insurance, legal, or financial advice. Insurance coverage, exclusions, and eligibility vary widely depending on the provider, jurisdiction, and individual circumstances.

Recommended for you