What to Do After an Accident in a Short-Term Rental Car: Insurance Claims Explained

——A Practical Guide to the Claims Process, Required Documents, and Choosing the Right Add-On Coverage

By Michael Anderson | Updated on March 30, 2026 | 🕓15 minutes

Key Highlights

- What costs can arise after a minor accident in a rental car, and which ones are usually covered by insurance?

- What are the hidden gaps in standard rental car insurance, credit card coverage, and personal auto insurance?

- How do claims processes differ across countries and regions?

- What steps should you take immediately after an accident to protect your claim?

- Which additional coverages are worth considering before taking a rental car on the road?

You’re on the sunny streets of southern Spain, driving a rental car along the Mediterranean coastline. While reversing, you didn’t notice a low stone pillar behind you, and the rear bumper got a few noticeable scratches. You step out and look at it, thinking, “Luckily I bought insurance, this shouldn’t be a big problem.”

When returning the car, the rental company staff walked around the vehicle, tapped a few times on their tablet, and handed you a bill:

Vehicle repair cost: €2,800

Downtime loss: €500

Administrative fee: €150

Total: €3,450

You freeze. A few scratches, over three thousand euros.

“I bought insurance!” you say.

“Yes, but your insurance has a deductible and does not cover downtime or administrative fees,” they reply calmly.

This is not a made-up story. It’s a type of real bill I have repeatedly seen while tracking rental car claims over the past few years. Every charge has its source, and behind every “I thought insurance would cover it” thought, there can be a significant financial gap.

Today, I want to break down these bills for you. Not to scare you, but to help you clearly understand next time you rent a car: which costs might occur, who is responsible for them, and—most importantly—how to proactively close the most common risk gaps.

Part 1: A Complete Breakdown of an Accident Bill

Let’s open up that Spanish bill and examine it line by line.

1.1 Vehicle Repair Cost: €2,800

This is the largest item on the bill. The rear bumper repair—covering parts replacement, painting, and labor.

Why so expensive? Several factors overlap:

OEM parts: Rental cars usually require original manufacturer parts for repairs, which cost much more than aftermarket parts.

Painting process: Modern car paint uses multiple layers; a complete repaint of a bumper involves disassembly, sanding, primer, color coat, and clear coat, with labor costs in Europe reaching €80–120 per hour.

Rental company repair network: Most rental companies have partnerships with specific repair shops, and their quotes often exceed the market average.

This cost corresponds to the physical repair of the vehicle. In most insurance structures, this is the easiest part to cover—as long as you bought CDW/LDW. But coverage does not equal full coverage.

1.2 Downtime Loss: €500

This is the fee most renters feel is “unfair.”

The logic is simple: while your car is being repaired, the rental company cannot rent it out, resulting in lost revenue. The company charges you based on “daily rental × repair days.”

In this bill:

Repair took 5 days

Daily rental for a similar car: €100

5 days × €100 = €500

Key issues: Was 5 days actually needed? Sometimes yes. But sometimes, the rental company might “extend” the repair period—for example, the workshop may take only 2 days, but because of parts ordering, the rental company still charges 5 days. More importantly, most standard insurance (including many credit card insurance policies) clearly do not cover downtime loss.

1.3 Administrative Fee: €150

This is the smallest but most frustrating item.

The rental company charges this fee for paperwork, communication with the repair shop, insurance claim coordination, and other “administrative costs.” The amount usually ranges from €50–250, depending on the company and the complexity of the accident.

Key point: almost no insurance covers this fee. It is not a “loss” but a “service fee,” so the insurance logic is: we do not cover service fees.

1.4 Deductible: The “Out-of-Pocket” Hidden in Repair Costs

In this bill, the €2,800 repair cost actually has a hidden structure: if the renter bought CDW but not zero-deductible coverage, the repair cost would include a deductible, usually €800–1,500.

This means that even if insurance “covers” the repair, the renter still has to pay the deductible first. In this Spanish case, the renter purchased zero-deductible coverage, so the repair was fully covered. If not, the bill would have an extra €800–1,500 out-of-pocket.

1.5 Diminished Value: Hidden Costs That May Appear

This bill does not include diminished value, but it can exist.

Diminished value logic: even after repairs, a vehicle’s market value decreases because it has an accident record. Some countries and rental companies allow recovery of this depreciation.

In some U.S. states, this is legally recoverable; in Europe, it is less common but not unheard of. If it occurs, the amount may be 10–30% of the repair cost.

Part 2: Insurance Coverage Blind Spots — What You Think is Covered May Not Be

Short-term rental insurance is essentially “patched together.” Different sources cover different parts, leaving many gaps.

2.1 Rental Company CDW/LDW: Broadest Coverage, Most Gaps

CDW (Collision Damage Waiver) or LDW (Loss Damage Waiver) is the basic protection offered by rental companies, usually included in the rental price or optional.

Covers:

Vehicle damage from collisions, scratches, theft

Does not cover (common exclusions):

The key point: CDW often has a deductible. Even if the accident falls within coverage, you pay a fixed amount first, and the insurance covers the rest.

2.2 Credit Card Insurance: Secondary Coverage, More Exclusions

Many premium credit cards offer rental collision coverage. Sounds great—pay with your card, get insurance for free.

But details make it far from “universal”:

Secondary insurance terms:

You must first claim through the rental company or other insurance

Credit card insurance only covers the “uncovered portion”

If you skip the first insurer and go straight to the credit card, claims may be denied

Common exclusions (more than rental CDW):

❌ Downtime loss

❌ Administrative fees

❌ Certain vehicle types (luxury cars, SUVs, vans, pickups)

❌ Rentals longer than 30 days

❌ Certain countries/regions (e.g., Ireland, Israel, Jamaica)

❌ Tires, glass, undercarriage

Real case:

A tourist rented in Ireland using a credit card. Accident repair cost: €1,200. Credit card insurance denied the claim because Ireland was on the exclusion list. The tourist paid fully out-of-pocket.

2.3 Personal Auto Insurance: Usually Invalid Cross-Border

Many think, “I have car insurance at home; it should cover a rental.”

Reality:

Most domestic commercial car insurance does not cover foreign rentals

Even if some high-end policies cover abroad, they usually have strict limits (e.g., rental period <30 days, only specific countries)

Claiming through domestic insurance may raise your home premiums

Core conclusion: Short-term rental insurance is not “one insurance,” but “a patchwork of multiple insurances.” The joints of this patchwork are risk blind spots. And these blind spots are exactly where the charges on accident bills often appear.

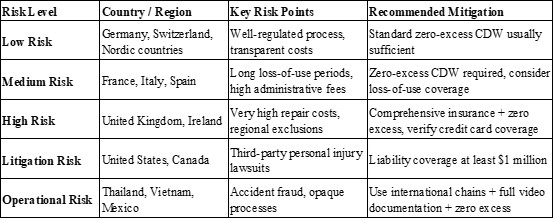

Part 3: Cross-Country Claims Differences — Same Car, Different Rules

The variable most often underestimated in short-term rentals is country. The same accident may have completely different handling processes, cost structures, and insurance rules depending on the country.

3.1 Europe: Strict Procedures, Downtime Fees Often Recovered

Germany, Switzerland, Austria:

Extremely standardized procedures; accidents usually must be reported to the police

Police report is key for claims

Repair quality requirements are high; costs are transparent but relatively high

Downtime loss calculated accurately based on actual repair days

France, Italy, Spain:

Even minor accidents may need formal documentation, otherwise claims are difficult

Downtime periods tend to be longer (workshop efficiency lower, parts supply slow)

Rental companies tend to replace rather than repair, increasing repair costs

Risk tip: minor accidents’ downtime loss may reach €500–1,000

UK, Ireland:

Repair costs extremely high, especially for luxury brands

Strict liability determination; complex road conditions (right-hand drive)

Special risk: some credit cards exclude Ireland from coverage

3.2 North America: Liability Coverage Is Key

USA, Canada:

Third-party liability coverage is crucial; U.S. litigation culture is strong—if someone is injured, claims may be extremely high

Basic rental fee usually does not include third-party liability (some states except); supplementary liability insurance (LIS/SLI) must be purchased

Recommended coverage: $1 million

Credit card insurance widely used, but confirm if it’s primary coverage

3.3 Asia & Emerging Markets: Unstandardized, High Operational Risk

Thailand, Vietnam, Mexico:

Rental company standardization varies greatly

Risk of “accident fraud” (companies exaggerate damage)

Police reporting process not transparent

Core advice: choose international chains (Hertz, Avis, Europcar), record video during pick-up

Japan, South Korea:

Processes highly standardized, but strict restrictions for foreign drivers

Chinese driving licenses cannot be used directly (IDP required)

Road rules differ (right-hand vs. left-hand), accident rates higher

3.4 Country Risk Quick Reference Table

Part 4: Claims Process Recap — Each Step Can Have Pitfalls

4.1 Step 1: At the Scene — Every Action Affects Your Claim

Correct actions:

1. Ensure safety; place warning signs

2. Take photos (overall + details + other vehicle + road conditions)

3. Do not admit fault (“I’m not sure; let the police handle it”)

4. If third party or injury involved, call police immediately

5. Contact rental company for accident instructions

If ignored:

No photos → responsibility cannot be proven; may be deemed fully at fault

Admitting fault → may violate rental contract, affecting claim

Not reporting promptly → in some countries, insurance may be denied

4.2 Step 2: Return Time — Bills Come Faster Than You Think

At return, the company checks the vehicle:

1. Staff records damage

2. You sign accident confirmation form

3. Rental company charges your credit card the estimated cost (or freezes equivalent amount)

4. You receive the bill

If ignored:

Not checking damage record → may be charged for pre-existing damage

Not requesting a written bill → no documentation for claims

4.3 Step 3: Insurance Claim — Discovering Coverage Gaps

This is the most stressful stage. You may face multiple insurance channels:

Channel 1: Rental company CDW

With zero deductible, repair cost fully covered

Without zero deductible, you pay the deductible

Downtime and administrative fees usually not covered

Channel 2: Credit card insurance

Submit rental company payment receipt, accident report, police report, etc.

Wait for review (2–8 weeks)

May be denied (excluded regions, vehicle types, late report, etc.)

Channel 3: Personal car insurance (if applicable)

Confirm cross-border validity

May affect domestic premiums

If ignored:

Not keeping all documents → incomplete claim

Reporting late → insurance denied

Not confirming payment order → misusing insurance channels, claim fails

4.4 Step 4: Disputes and Supplementary Payments — May Take Months

Even after partial reimbursement:

Negotiate downtime calculation with rental company

Appeal credit card insurance denial

Pay administrative fees or other uncovered items

If ignored:

Giving up negotiation → pay hundreds or thousands extra

No appeal record → lose future recovery rights

Part 5: Visualizing Hidden Risks — Which Risks Can Be Transferred, Which Must Be Borne

1. Transferable Risks: Where Insurance Truly Helps

These risks have clear insurance products that can cover them.

Vehicle repair costs: Core CDW coverage. Note: most CDWs have a deductible (€800–1,500 in Europe). Only zero-deductible purchase fully eliminates out-of-pocket.

Third-party liability: Compensation for injury or property damage to others can be huge. European base rental usually includes high liability; in the U.S., purchase separately, recommended coverage ≥ $1 million.

Theft protection: Usually bundled with CDW; also has deductible. Theft due to negligence (keys left inside) may be denied.

2. Reducible Risks: Insurance Doesn’t Cover Fully, But You Can Control

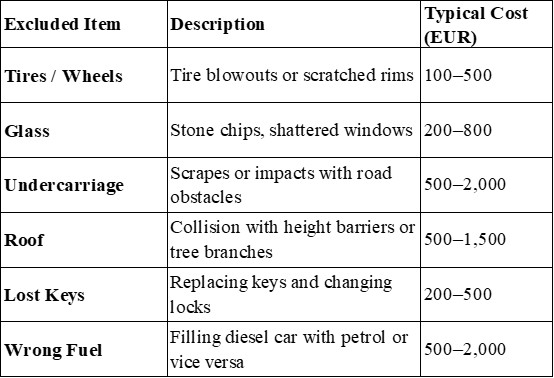

These risks have no dedicated insurance, but you can reduce loss by choice or action:

Downtime loss: Rental company income loss during repair; calculated as “daily rental × repair days.” Most standard insurance does not cover. Reduce by either purchasing an all-inclusive plan with downtime coverage or negotiating actual repair time with workshop proof.

Administrative fee: €50–250; almost no insurance covers. Only “zero-liability full coverage” packages may waive it.

Tires/glass/undercarriage: Standard CDW excludes these. If driving on rough roads, buy coverage upgrades.

3. Uncontrollable Risks: Must Be Self-Borne

Insurance never covers, only preventable or self-borne:

Administrative fee (without package): €50–250, mandatory

Wrong fuel type: €500–2,000; all insurance excludes, driver error

Lost key: €200–500 for smart key, may require lock replacement; not covered

Contract violations: DUI, unlicensed driving, off-road driving → all insurance void, total self-pay

4. Decision Logic for the Three Risk Types

Must buy: CDW + zero deductible. Bottom line to avoid a €1,000+ bill from one accident.

Optional: Tires/glass/undercarriage coverage (if mountain/rough roads), downtime coverage (budget permitting), supplemental third-party liability (U.S. rentals).

Self-borne, but must be aware: Administrative fee, wrong fuel, lost key, contract violations.

5. Two-Minute Pre-Pickup Self-Check

Have I confirmed CDW deductible? Bought zero deductible?

Does my route require tires/glass coverage?

Do I need supplemental liability insurance for this country?

Am I aware of administrative fees?

Have I confirmed fuel type and secured the keys?

Answer these five questions, and you’ll clearly understand “what risks I bear.” This awareness is the best protection when renting a car.

References

1. The Business Research Company. (2025). Rental car insurance global market report 2025. GII Research. https://www.giiresearch.com/report/tbrc1823118-rental-car-insurance-global-market-report.html

2. Northbound. (2025). If vehicle damages, breaks down or an accident occurs. https://www.northbound.is/zh/help/article/what-to-do-if-vehicle-damages-breaks-down-or-accident

3. Gentile, D., Donmez, B., Min, D., & Waite, T. (2025). Assessing risk of collision with fleet telematics for usage-based insurance: Case study from South Korean car rental operations. Transportation Research Record: Journal of the Transportation Research Board. https://trid.trb.org/View/2630574

4. MFMac. (2025, August 28). What should I do after a road traffic collision abroad? https://www.mfmac.com/insights/personal-injury/what-should-i-do-after-a-road-traffic-collision-abroad-qa/

5. Hola Car Rentals. (2026, February 5). In the United States, what is ‘loss of use’ on a car-hire contract, and who pays? https://holacarrentals.com/blogs/car-rental-united-states/in-the-united-states-what-is-loss-of-use-on-a-car-hire-contract-and-who-pays

6. CarInsurent. (2026, February 12). Rental car insurance: Identifying geographic anomalies in rental car damage claims. https://carinsurent.com/guides/car-rental-insurance-guides/rental-car-insurance-identifying-geographic-anomalies-in-rental-car-damage-claims/

About the Author

Michael Anderson is an automotive risk consultant and writer based in London. With over a decade of experience in vehicle rental operations and insurance claims analysis, Michael has advised both rental companies and private renters on minimizing risk and navigating international insurance claims. He regularly contributes to industry journals on automotive insurance trends.

Editorial Transparency Statement

This article is independently researched and written by the author. All information is based on publicly available sources and verified case studies. No rental company or insurance provider sponsored this content.

Disclaimer

This article provides general information for educational purposes only. It does not constitute legal, financial, or insurance advice. Readers should consult their rental agreements, insurance policies, or professional advisors for guidance specific to their circumstances.

Recommended for you