Long-Haul Logistics Insurance in Europe: Costs vs. Claims Success Rate

——Case Studies on Choosing Add-On Coverage for Maximum Protection

By Lucas Reinhardt | Updated on March 25, 2026 | 🕓12–15 minutes

Key Highlights

- Why basic logistics insurance is often insufficient for European long-haul transport

- Real case studies: theft, legal disputes, and operational errors under the CMR framework

- Cost vs. protection: how to calculate premiums and avoid over-insuring

- Practical steps to improve claims success rates through documentation and compliance

A truck fully loaded with high-value electronic goods departs from London, crosses the English Channel, travels along French highways, and ultimately reaches its destination in Florence, Italy. At a highway rest area in France, during a brief ten-minute absence by the driver, the container seal is broken, and goods worth tens of thousands of euros vanish without a trace. The cargo owner assumed they were insured, but the final compensation amounted to only one-tenth of the actual loss—because the carrier’s liability was limited to 8.33 SDR per kilogram under the CMR Convention, and the “basic insurance” purchased did not cover theft risk.

This is not a fictional story, but a real case involving a UK freight forwarder in 2025. With the globalization of cross-border e-commerce and manufacturing supply chains, long-haul logistics in Europe faces unprecedented risk challenges: multi-country transportation, multimodal transshipment, port congestion, labor strikes, and increasingly frequent extreme weather events. Is basic insurance alone really sufficient? How can add-on coverage improve protection and increase claims success rates?

I. Overview of Long-Haul Logistics Insurance in Europe: More Than Just “Having Coverage”

1.1 Full Breakdown of Insurance Types

Long-haul logistics insurance in Europe is not a single product but a combination of “basic coverage + add-on coverage.” Understanding the scope of each type is the first step toward a scientific insurance configuration.

Basic Coverage: Total Loss and Partial Loss

Basic insurance covers losses caused by natural disasters or accidents during transportation. Total loss refers to goods being completely destroyed or irreparable; partial loss refers to damage to part of the cargo, compensated proportionally. Basic premium rates typically range from 0.2% to 0.8% of cargo value. For general goods transported by sea, rates can be as low as 0.3%, while high-risk goods (fragile or high-value items) may reach up to 1.5%.

Add-On Coverage: Targeting “Invisible Risks” Precisely

1.2 Cost Structure: More Than Just a Percentage

The total cost of logistics insurance consists of three components:

Total Premium = (Cargo Value × Basic Rate) + Σ (Cargo Value × Add-On Rates) + Minimum Premium / Fees

Key parameters:

- Minimum premium: typically €50–€150, regardless of cargo value

- Transport mode impact: sea freight has the lowest rates (0.2%–0.5%), followed by air freight (0.3%–0.8%); road and multimodal transport have higher rates due to increased transshipment risks

- Number of transshipments: each additional transshipment increases the rate by approximately 0.05%–0.1%

Example Calculation:

For cargo valued at €100,000, selecting “basic coverage (0.3%) + war/strike coverage (0.2%) + documentation & compliance coverage (0.1%)”:

Total premium = €100,000 × 0.6% + minimum premium €80 = €680

II. Claims Success Rate Analysis: The Truth Behind the Numbers

2.1 Four Key Factors Affecting Claims Success Rate

1) Clarity of Policy Terms

The clearer the terms and defined liabilities, the higher the claims success rate. Ambiguous “all risks” definitions often lead to disputes after an incident.

2) Complete Transportation Evidence Chain

From container loading photos, bills of lading, transshipment receipts to customs documents—missing any link may result in claim denial. In European logistics practice, evidence chain completeness is the “lifeline” of claims.

3) Financial Strength of Carrier and Insurer

Top-tier insurers (such as Allianz, AXA) provide stable payouts but at higher premiums; smaller insurers may have stricter reviews and longer claims cycles.

4) Reasonableness of Declared Cargo Value

Undervaluation → insufficient compensation ceiling

Overvaluation → triggers investigation for “over-insurance,” potentially considered fraudulent

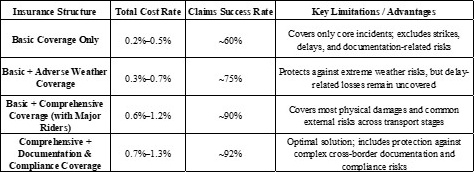

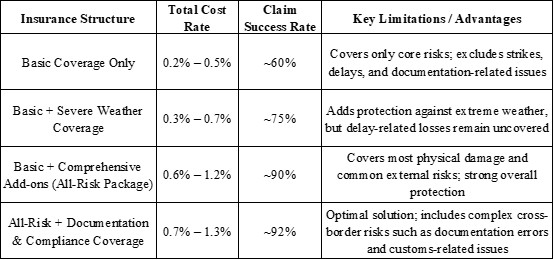

2.2 Comparison of Claims Success Rates by Insurance Structure

From 60% to 92%, the leap lies in the precise configuration of add-on coverage. Every additional premium spent on add-ons offsets the probability of claims failure in specific risk scenarios.

III. Real Case Studies in Europe: Learning from Practice

Case 1: UK ↔ Italy Road Transport Theft — Complementarity Between CMR Liability Limits and Commercial Insurance

Background:

A UK freight forwarder operates consolidated road freight services between London and Florence, Italy. In 2025, goods were stolen at a highway rest area in France. The vehicle was recovered, but part of the high-value cargo was lost. Total cargo value: approximately €120,000.

Insurance Situation:

Some cargo owners relied solely on carrier liability insurance, while others purchased comprehensive commercial cargo insurance.

Compensation Results:

- The carrier compensated based on the CMR Convention limit of 8.33 SDR/kg (approximately €23/kg). Assuming a total cargo weight of 2 tons, the maximum compensation was €46,000—far below the actual value.

- Cargo owners with comprehensive insurance received compensation exceeding 85% of cargo value, with insurers covering the gap beyond the carrier’s liability.

- Cargo owners relying only on carrier liability received less than 40% of actual losses.

Key Insight:

CMR is not insurance—it is a liability ceiling. In European road transport, carrier liability cannot replace cargo insurance. Any cargo exceeding €5,000 in value should be covered by independent cargo insurance or comprehensive coverage.

Practical Recommendations:

- After an incident, submit a formal CMR claim notice to the carrier (to preserve legal recourse) and report the claim to the insurer simultaneously.

- Carrier compensation does not count toward the insurance deductible and can be used cumulatively.

Case 2: Malta Court Case — Burden of Proof as the “Life-or-Death Line” in Claims

Case Name: Elmo Insurance Ltd. vs Jet Freight Ltd.

Background:

In November 2020, a shipment of household appliances (total value €25,382.40) transported by sealed truck from Romania to Malta was lost during road transit. The contract was governed by the CMR Convention.

Key Issue:

After cargo loss, who bears the burden of proof? Does the insurer have the right to deny claims due to insufficient evidence?

Court Ruling:

- Clarified the critical role of burden of proof allocation in insurance disputes under the CMR framework.

- The insurer successfully established liability by proving the loss occurred during the insured period and within the policy’s coverage scope.

- The ruling emphasized that failure to provide a complete evidence chain (bill of lading, transshipment receipts, incident reports) allows insurers to deny claims.

Key Insight:

The evidence chain is the only legal language. Even with broad policy terms, failure to prove that “the incident occurred during the insured period and resulted from a covered risk” leads to claim failure.

Practical Recommendations:

- Photograph container corners and seal numbers during loading (video + images).

- Obtain receipt copies at every transshipment stage.

- For significant losses, appoint an independent surveyor—this is highly recognized by European courts and insurers.

Case 3: European 3PL Industry Practices — The Overlooked “CMR Documentation Details”

Background:

Multiple European third-party logistics providers have identified common reasons for claim denial or limitation, often unrelated to policy terms but rather to operational flaws.

Typical Issues:

1. Damage not noted on CMR document: If visible damage is not recorded as a “reservation” upon delivery, carrier liability is released.

2. Failure to notify within 7 days: Under the CMR Convention, visible damage must be reported in writing within 7 days, or the right to claim is lost.

3. Incomplete documentation chain: Missing transshipment records in multimodal transport makes it impossible to determine where the damage occurred.

“Breakthroughs in claims are not achieved by policies alone, but by complying with CMR reporting procedures, documenting damage evidence, and accurately filing cargo insurance claims.”

Insurance is not a “get-out-of-jail-free card.” Even with comprehensive coverage, failure to follow CMR procedures may prevent recovery from carriers, leading insurers to face unsuccessful subrogation and potentially impacting future premiums.

Practical Recommendations:

- Translate policyholder obligations into operational manuals and integrate them into KPI systems for warehouse and transport staff.

- Conduct regular training for frontline personnel on CMR documentation standards, 7-day notification rules, and evidence collection.

IV. Add-On Coverage Strategy: How to Configure Precisely

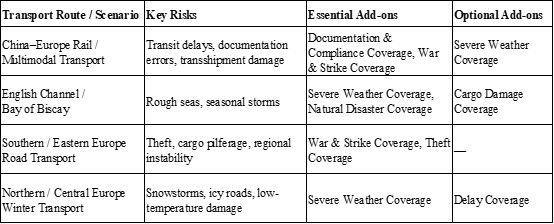

4.1 Route-Based Configuration Guidelines

4.2 Cargo-Type-Based Recommendations

High-value electronics (over €50,000):

- Recommended: comprehensive coverage + delay insurance

- Reason: sensitive to delivery timing; delays may halt production lines

Multimodal shipments (sea + road):

- Recommended: comprehensive coverage + war/strike coverage + documentation & compliance coverage

- Reason: increased risk of labor disputes and documentation errors

Art and luxury goods (over €100,000):

- Recommended: comprehensive coverage + special packaging coverage + theft insurance

- Reason: carrier liability limits are often insufficient; theft is the primary risk

Time-sensitive goods (production materials, perishables):

- Recommended: basic coverage + delay insurance (essential)

- Reason: delay insurance (0.12%–0.3%) can cover losses far exceeding cargo value

4.3 Avoid Over-Insuring: Cost-Effectiveness Analysis

Not all add-on coverage is necessary for every shipment. Consider reducing coverage in the following cases:

- Low-value cargo (< €5,000): basic coverage is sufficient

- Direct sea transport (no transshipment): documentation & compliance coverage may be omitted

- Summer transport (outside storm seasons): adverse weather coverage may be optional

Decision Principle:

Analyze claims data from the past 12 months to identify the top three risk events causing losses, and selectively add corresponding coverage.

V. Operational Guide: Five Steps to Improve Claims Success Rate

1. Identify Risks and Configure Coverage in Advance

- Analyze transport routes (high-risk regions, multimodal transport)

- Evaluate cargo characteristics (value, fragility, time sensitivity)

- Configure coverage based on a “must-have add-on list”

2. Clarify Policy Terms and Exclusions

- Review coverage scope (warehouse-to-warehouse? door-to-door?)

- Understand exclusions (war, nuclear risks, intentional damage)

- Check deductibles (e.g., €200 or 10%)

3. Preserve Complete Evidence Throughout Transportation

Before incidents (preventive evidence):

- Container loading photos (corners, seal numbers with timestamps)

- Transshipment records (signed receipts for each stage)

- Customs documents consistent with invoices and packing lists

After incidents (emergency evidence):

- Within 24 hours: report to police (if theft involved) and notify insurer

- Within 7 days: submit written notice to carrier (CMR requirement)

- Take photos/videos of damage and retain damaged packaging

- Appoint an independent surveyor for major losses

4. Declare Cargo Value Accurately

- Use invoice value—avoid underreporting or overreporting

- Include freight and insurance costs if applicable

5. Use Digital Claims Platforms to Accelerate Processing

- Leading European platforms (e.g., Claisy) offer payouts within 48–72 hours, much faster than traditional insurers (30–60 days)

- Digital platforms support online evidence submission and real-time tracking

In the complex environment of European long-haul logistics, insurance is not a simple “buy it and forget it” product—it is a finely tuned risk management system requiring precise configuration and strict execution. As demonstrated in these cases, the difference lies not in luck, but in preparation.

References

1. TT Club. (2025). Case 1: Cargo liability – freight forwarder. Retrieved from https://www.ttclub.com/news-and-resources/case-studies/article/case-1-cargo-liability-freight-forwarder/

2. Ganado Advocates. (2024). Burden of proof and the international carriage of goods: Insurer succeeds in cargo theft claim. Retrieved from https://ganado.com/burden-of-proof-and-the-international-carriage-of-goods-insurer-succeeds-in-cargo-theft-claim/

3. Reddit. (2026, January 15). How do EU logistics or 3PL's companies actually handle freight claims under CMR? Is the process as complicated as it looks? [Online forum post]. Retrieved from https://www.reddit.com/r/CustomsBroker/comments/1ruofta/how_do_eu_logistics_or_3pls_companies_actually/

4. Elmo Insurance Ltd. v. Jet Freight Ltd. (2020). Court of Appeal (Malta). Retrieved from Ganado Advocates case summary.

About the Author

Lucas Reinhardt

Lucas Reinhardt is a cross-border logistics analyst and independent supply chain researcher based in Europe. With a background in freight forwarding operations and transport compliance, he has spent the past decade studying risk patterns in long-haul cargo movements across the UK and EU corridors.

Editorial Transparency Statement

This article is intended to provide an objective, experience-based analysis of long-haul logistics insurance in Europe. The case studies referenced are derived from real industry scenarios, legal rulings, and operational insights from logistics practitioners.

No insurance providers have sponsored, influenced, or reviewed this content prior to publication. All recommendations are based on publicly available information, industry practices, and professional experience.

Disclaimer

This content is provided for informational and educational purposes only and does not constitute legal, financial, or insurance advice. The information presented does not represent an offer, solicitation, or recommendation to purchase any insurance product.

Insurance policies, coverage terms, and claims procedures vary by jurisdiction, provider, and individual contract. Readers are strongly advised to consult licensed insurance professionals, legal advisors, or qualified brokers before making any insurance-related decisions.

The publisher and author assume no liability for any losses or decisions made based on the information provided in this article.

Recommended for you