What Are the Key Differences Between Urban Auto Insurance in the US and Europe?

—— Comparing Coverage, Costs, Claims Processes, and Commuting Risk Factors Across Major Cities

By Jonathan Miller | Updated on March 26, 2026 | 🕓12 minutes

Key Highlights

- Why premiums differ dramatically between the US and Europe

- Minimum coverage vs. high baseline insurance approaches

- US credit-based pricing vs. Europe’s driving-focused system

- Claims processes: Legal battlefield vs. standardized administrative flow

- Commuting risks in major cities across both continents

As a car owner who has driven extensively in both the US and Europe, I spent three years studying the differences in auto insurance systems between the two regions. I have experienced claim disputes, skyrocketing premiums, and the confusion of cross-border driving. Here, I am not promoting any insurance products; I am simply sharing real experiences and case studies to help you make wiser risk management decisions in different environments.

1. Why can premiums for the same car differ by several times?

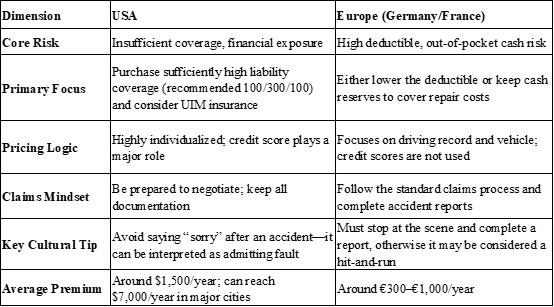

First, let’s look at some startling data: in the US, the average annual premium for a typical family car is around $1,500, while in Germany or France, similar insurance may cost only €300–€1,000. But this is just the average—full coverage in Brooklyn, New York, can reach $6,841/year, 1.75 times the state average.

Behind this difference lie two completely different pricing philosophies.

2. Coverage: Minimum coverage vs. a high baseline

🇺🇸 United States: 50 states, 50 sets of rules

Auto insurance in the US is regulated independently by each state, creating a “fragmented” regulatory map. Each state has different minimum liability requirements, but a common feature is that these minimums are often worryingly low.

For example, in California, the minimum property damage liability is only $5,000. In today’s car and repair cost environment, even a minor rear-end collision can exceed this amount. If you only purchase the state-mandated minimum, and the at-fault party’s coverage is insufficient, the difference will be borne by you—this is the unique US risk of underinsured motorists (UIM).

In the US, collision and comprehensive coverage are generally not mandatory (unless you have a car loan). But if you want real protection, you almost must buy them. Additionally, there are optional add-ons like medical payments coverage, uninsured motorist coverage, and roadside assistance, making the selection process extremely complex.

🇪🇺 Europe: Unified “high baseline” coverage

Europe (especially the EU) takes a completely different approach. All member states follow the EU Motor Insurance Directive, implementing a unified third-party liability system with very high coverage—often in the millions of euros.

What does this mean? If you have an accident in Berlin or Paris and are at fault, the victim is almost guaranteed full compensation, without being affected by your coverage limits. This reflects a social philosophy: accident victims should not be left uncompensated due to the perpetrator’s lack of wealth.

Europe’s full coverage (Casco) is similar to the US, but with a key difference—the excess (deductible) system. When renting a car in Europe, the base price usually includes basic collision/theft coverage but comes with a very high excess, sometimes up to €2,000. This means if you scratch the car, you must pay up to €2,000 out-of-pocket. This is not the insurer being “unfair,” but a risk-sharing mechanism—it encourages careful driving while keeping base premiums relatively low.

3. Premium pricing: Credit score vs. driving behavior

🇺🇸 United States: Your credit score is your risk score

In the US, insurers scrutinize everything about you:

Credit score: One of the core pricing factors; a poor score can double your premium (though some states have banned this practice)

Personal attributes: Age, gender, marital status, occupation, even the color of your car

Location: Risk varies significantly by ZIP code

Unmarried young men pay the highest rates because insurers consider them “less responsible and more accident-prone.” If you drive a bright red sports car, your premium may also increase—psychologists believe men who prefer bright colors are more emotionally reactive.

This pricing model logic is “actuarial fairness”—using all available data to predict your likelihood of claims. But the consequence is that newcomers, young people, or low-income groups may face a “poverty premium.”

🇪🇺 Europe: Focus on driving itself

Europe’s pricing system focuses more on factors directly related to driving:

Bonus-Malus system: The essence of European insurance. The longer you go without an accident, the higher the discount (“bonus”); after a claim, next year’s premium rises sharply (“malus”). In Germany, new drivers pay 260% of the standard rate, decreasing yearly to a minimum of 35%—if no accidents occur.

Vehicle characteristics: Model, horsepower, and safety features are core pricing factors

Usage patterns: Cars used for daily commuting have higher premiums than weekend-only vehicles

Registration location: In Germany, the same car registered in Berlin can cost one tier more than in Bonn, due to higher vehicle density, traffic complexity, and theft rates

Europe generally prohibits or strictly limits the use of credit scores, marital status, or similar factors in pricing. The philosophy is that driving risk should be determined by driving behavior and vehicle risk—a socially fair approach.

4. Claims process: From “legal battlefield” to “administrative flow”

🇺🇸 United States: Lawyers are the norm

A defining feature of US claims is high lawyer involvement. A real case in San Diego, California:

A woman was rear-ended during her commute. The initial damage seemed minor—bumper dent, broken tail light. The at-fault insurer offered $3,500 quickly. However, she later developed persistent neck pain and headaches and was diagnosed with a herniated cervical disc. After lawyers got involved, the case settled for $175,000.

This case highlights several US claims characteristics:

No-fault vs. tort states: In no-fault states, your own insurer covers medical costs first; in tort states, you must negotiate with the at-fault insurer

Pain and suffering claims: A US-specific concept where compensation can far exceed actual medical costs

Lawyer involvement is common: Insurers prioritize liability allocation over rapid payout

Another case in Maine involved a woman hit by a hit-and-run driver. The perpetrator was never found; she ultimately received compensation via her uninsured/underinsured motorist coverage (UIM)—underscoring the importance of adequate UIM coverage in the US.

🇪🇺 Europe: Standardized procedures and cross-border convenience

European claims resemble an administrative process rather than a legal battlefield. A notable case in the UK:

In 2018, London witnessed a car crash where a police officer drove at 87 mph (limit 30 mph) and collided with another vehicle, injuring a fellow officer. The case went through multiple courts, ultimately applying the EU Motor Insurance Directive’s direct claim mechanism.

The highlight: under the 2002 EU regulation, the victim can directly claim against the at-fault driver’s insurer, which “acts in the position of the perpetrator.” This makes the process more direct.

Other conveniences in Europe:

European Accident Statement: EU drivers carry a multilingual standard accident form. Both parties fill it out, draw diagrams, sign, and submit to the insurer, reducing disputes

Cross-border claims cooperation: Your policy is valid in any EU member country

Bonus-Malus system: Rewards safe driving; no-claim history can transfer across borders

5. Commuting risks: Different cities, different nightmares

🇺🇸 US cities: Long commutes and regional differences

The biggest risk in US urban driving is high mileage and regional variance. A 2025 study ranks the worst US driving cities: Philadelphia, Oakland, Washington D.C., New York, and Chicago.

Why is Philadelphia the worst? Longest congestion times, poor road maintenance, high accident and theft rates, and expensive insurance.

South Carolina is the worst state for driving: 26.21 deaths per 100,000 people, average commute 25.5 minutes, annual premium $1,812. Colorado has the highest car theft rate—731 per 100,000—and premiums close to $2,900/year.

The core US risk is not vehicle damage but medical bills: an ambulance, ER visit, or a few days in hospital can easily exceed $50,000–$100,000. A single at-fault accident may double premiums for 3–5 years.

🇪🇺 European cities: High density, low-speed risk

European urban driving risks are different. London, Paris, Rome, and Barcelona face:

Extremely dense traffic: Paris has the highest flight cancellation rate (21%), with Rome and London close behind

Difficult parking and slow speeds: serious accident frequency is relatively low, but minor scratches are common

Theft and cash risks: Paris 9%, Barcelona 8%, London 7%

For cross-border drivers, medical emergencies are a special risk: 11% of travelers in London and 10% in Rome face urgent medical situations. Public healthcare covers some costs, but cross-border medical expenses can still be a financial burden.

6. Key Takeaways

Reflecting on two years of research and personal experience, my biggest insight: auto insurance is not buying a product—it’s managing risk.

In the US, you are purchasing a firewall against astronomical medical and legal costs. This means focusing on coverage limits and UIM sufficiency, not just monthly payments.

In Europe, you are dealing with an administrative contract requiring careful management of excesses and discount systems. This means paying attention to your Bonus-Malus rating and whether the deductible is within your tolerance.

References

1. Chron. (2025). Best & worst cities to drive in America. Retrieved from https://www.chron.com

2. European Insurance and Occupational Pensions Authority (EIOPA). (n.d.). Motor insurance directives and cross-border claims. Retrieved from https://www.eiopa.europa.eu

3. KASH Legal Group. (2025). Case study: Rear-end collision with delayed injury discovery. Retrieved from https://www.kashlegal.com

4. NewsBreak. (2025). Differences in auto insurance requirements between the U.S. and Europe. Retrieved from https://www.newsbreak.com

5. Peter Thompson & Associates. (2021). Hit-and-run claims and uninsured motorist coverage: A Maine case study. Retrieved from https://www.peterthompsonlaw.com

6. Underwood Law Firm. (2025). State-by-state driving environment and insurance cost analysis. Retrieved from https://www.underwood.law

7. Zurich Insurance PLC v. Commissioner of Police for the Metropolis [2025] EWHC 123 (QB). (2025). England and Wales High Court.

About the Author

Jonathan Miller

Jonathan is a travel insurance analyst and freelance writer specializing in international travel risk management. With over 8 years of experience in both US and European travel insurance markets, he provides practical guidance for travelers, including expatriates and short-term tourists. He has consulted for rental car platforms, insurance brokers, and travel publications, helping readers optimize coverage for multi-country road trips.

Editorial Transparency Statement

This article is independently researched and written. It is intended solely to provide factual information and personal experience-based analysis. No insurance products are promoted or sold, and no affiliate relationships influence the content.

Disclaimers

The information provided is for reference purposes only and should not be considered professional insurance advice.

Readers should verify all details with local regulations, insurers, or licensed insurance professionals before making coverage decisions.

Policies, rules, and premiums vary by region, state, and country, and are subject to change.

Recommended for you