Electric Vehicle Commuting Insurance vs Regular Auto Insurance: What Actually Changes in Real Claims?

——A Data-Backed, Real-Case Analysis of Costs, Coverage Gaps, and Claim Denials

By Emily Carter | Updated on March 24, 2026 | 🕓12 minutes

Key Highlights

- Comparison of EV vs. conventional vehicle insurance in real claims

- Real-world claim cases illustrating EV-specific risks

- Common reasons EV commuting claims are denied

- How to calculate the true cost of EV insurance

- Strategies to optimize commuting EV insurance

What are the differences between EV commuting insurance and regular auto insurance? How is the cost of EV commuting insurance calculated most efficiently? In which situations does insurance not cover accidents that occur on the way to work?

Last winter, a Tesla Model 3 owner accidentally hit a pillar while reversing at low speed in the company’s underground parking lot on the way to work. On the surface, the accident didn’t seem serious—the rear bumper had a minor dent, and the tail light was broken. Based on experiences with conventional vehicles, this would be a typical single-vehicle accident, with repair costs around $1,500–$2,000.

But what happened next caught the owner off guard.

After the insurance company towed the car to an authorized repair center for inspection, the repair report showed that the collision area was near the rear high-voltage battery pack, and the battery casing had a deformation of 0.3 mm. Although the car was still drivable and the dashboard showed no fault codes, the repair center, following manufacturer safety protocols, recommended replacing the entire battery pack. Replacement cost: $16,800.

Ultimately, the insurance company declared the vehicle a total loss, citing that “repair costs exceed 70% of the vehicle’s actual value.” After receiving the payout, the owner found that the expected premium for the following year would increase by 40%, and several insurance companies refused to offer standard rates for their new car.

On multiple EV owner forums, similar experiences were reported: a seemingly minor parking lot collision led to a total loss declaration due to potential battery damage.

Why can a seemingly ordinary parking lot accident turn into an insurance disaster for an electric vehicle?

Part 1: Why EV Insurance Behaves Differently in Commuting Scenarios

1.1 Why Minor EV Accidents Lead to Higher Payouts

Core reason: The “chain reaction” cost logic of the battery

Repairs for conventional internal combustion vehicles follow a “localized damage, localized repair” logic—if the bumper is damaged, replace the bumper; if the headlight is broken, replace the headlight. But high-voltage battery packs in EVs are usually spread across the chassis, covering a large area between the front and rear axles.

This means:

- A rear-end collision may transmit impact forces through the vehicle structure to the battery casing.

- Bottom scraping can directly damage the battery’s cooling lines.

- Water exposure can allow moisture to seep into the battery pack if seals are compromised.

The insurance company’s main challenge: battery damage is hard to repair “locally.” Most manufacturers’ repair manuals stipulate that any deformation of the battery casing, no matter how small, requires full replacement. Reason: the risk of thermal runaway cannot be fully ruled out through visual inspection.

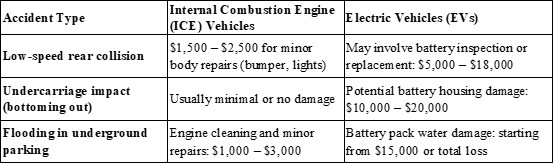

Typical cost comparison:

1.2 Why Commuting Classification Affects Claims

Insurance policies typically categorize vehicle usage into three levels:

- Social, Domestic & Pleasure (SDP): only for non-commuting personal activities.

- Commuting: includes regular trips to and from the workplace.

- Business: includes passenger transport, deliveries, business visits, etc.

Key difference: commuting is seen as a “high-frequency, fixed-route, high-exposure” scenario.

If the policyholder selects “personal use” but actually commutes daily, in case of an accident:

- The insurer may reduce the payout by 20%-50% due to “failure to disclose a material fact.”

- In extreme cases, if the accident occurs on the commute and the insurer has evidence, it may deny the claim entirely.

Example: A UK Nissan Leaf owner chose “social & leisure use” but commuted daily. After a rear-end accident on the way to work, the insurer analyzed the car’s GPS data, determined that 90% of mileage was for commuting, and ultimately reduced the payout by 40%.

1.3 Why Battery Risk Affects Underwriting

EV insurance underwriting logic is fundamentally changing:

- Traditional logic: evaluate the probability of an accident.

- EV logic: evaluate the expected payout per single accident.

The battery accounts for 30%-50% of the vehicle value. This means:

- A $40,000 EV has a battery valued at $12,000–$20,000.

- Once the battery is damaged, repair costs can easily exceed 60%-70% of the vehicle value.

- The insurer’s main risk is not “frequent accidents,” but “one accident can blow the payout.”

Industry data: According to the 2025 New Energy Vehicle Insurance Claims Report by the China Insurance Association, the average premium for new energy vehicles is 21% higher than for conventional vehicles, but the claim frequency is 8% lower. The only reason premiums are higher is that the average payout amount is 76% higher.

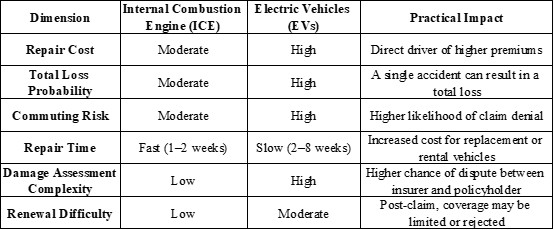

Part 2: Claims Comparison Between EVs and Conventional Vehicles

Repair Cost

- Conventional vehicles: mature market for engine, transmission, and core parts. Independent repair shops and dealerships can handle most repairs. Replacing and painting a rear bumper may cost $600–$800 at an independent shop.

- EVs: high-voltage batteries, motors, and controllers require authorized repair centers. Labor costs are higher ($120–$200/hour vs. $70–$100/hour). Parts lead time is longer.

Example: A Ford Mustang Mach-E owner in the U.S. paid $1,200 to replace a right side mirror with camera and blind-spot module, waiting 3 weeks. A comparable fuel vehicle, Ford Escape, cost $400 and 2 days.

Total Loss Probability

- Conventional vehicles: total loss occurs when frame or engine is heavily damaged. A 5-year-old car worth $15,000 may be totaled if repair exceeds $10,000.

- EVs: due to high battery value, total loss threshold is lower. A 3-year-old EV worth $25,000 may trigger total loss if battery replacement costs $20,000. Minor chassis scrapes may deform the battery casing, triggering total loss.

Example: BYD Han owner hit a raised drain cover in the underground garage; minor battery bottom scratches detected. Battery replacement cost: ¥60,000 (~$8,800), vehicle second-hand value: ¥90,000 (~$13,200). Insurance treated it as total loss.

Commuting Risk

- Conventional vehicles: commuting itself does not alter claims logic. Correct usage class ensures standard claim process.

- EVs: commuting increases exposure to EV-specific risks such as high-density parking, public charging. Examples:

Damage from other cars while charging at workplace.

Malfunction at public fast-charging station; unclear liability.

Daily parking in underground garages increases risk of water ingress or scraping.

Example: A European owner’s charging port burned due to a faulty charging gun at a workplace station. Insurance initially denied coverage; after 3 months, partial payout was granted.

Part 3: Real Claims Cases

Chassis Scraping – Immediate Inspection Required Even Without Warnings

- Scenario: driving over a raised manhole cover at ~30 km/h.

- Vehicle: Xpeng P7, 1.5 years old

- Incident: no dashboard warning, vehicle drove normally.

- After 2 months: “Battery system fault” appeared. Inspection revealed shorted internal cells; battery replacement cost ¥78,000 (~$11,500).

- Insurance claim: only 50% paid, citing inability to prove direct causation. Owner paid remaining ¥39,000 (~$5,750).

Key lesson: After any chassis scraping, water exposure, or collision, even without dashboard warnings, immediately inspect and report within 24 hours. Battery damage may have a latent period.

Part 4: Why EV Commuting Claims Are More Likely Denied

Charging Equipment Mismanagement

- Portable charging cables are often considered “personal items,” not vehicle parts. Standard car insurance usually excludes coverage unless “on-board item insurance” is added.

- Theft, crushing, or loss of cables may be denied. Some premium policies include cable coverage, but confirmation is needed.

Mitigation:

- Store charging cable in trunk or home when away from car.

- Confirm policy includes “charging equipment coverage.”

- Consider separate insurance for portable chargers if charging publicly.

Battery Damage Hard to Attribute

- Insurance requires “direct loss caused by an accident.” Battery aging or normal degradation is excluded. Delays between accident and damage detection make insurers claim “other causes” or “natural wear,” reducing or denying payout.

Mitigation:

- Immediate inspection at authorized center after bottom scraping, water exposure, or collision.

- Keep inspection reports, repair records, and photos.

- Report within 24 hours, even if no visible issues.

Unauthorized Modifications or Software Updates

- Vehicles must remain “factory condition.” Unauthorized modifications (motor, battery, suspension) must be declared; otherwise, related damage may be denied.

Examples:

- Third-party software boosting power → motor/battery issues denied.

- Non-original tires → blowout claims denied.

- Third-party tow hooks → rear damage from collision denied.

Note: Even manufacturer-provided OTA upgrades (e.g., Tesla acceleration pack) alter performance; declare to insurer to adjust premium.

Part 5: How to Calculate True EV Insurance Cost

EV insurance true cost = annual premium + expected out-of-pocket repair cost + implicit risk cost – fuel savings

Components

1. Annual Premium

- EV premiums are typically 20%-30% higher than similar conventional cars. Example: $40,000 vehicle

- Conventional car: $1,200–$1,500/year

- EV: $1,500–$1,900/year

- Reason: battery replacement cost, limited authorized repair network, high per-accident payout.

2. Expected Out-of-Pocket Repair Cost

Formula: deductible × accident probability × (1 – insurance payout ratio)

Key variables:

- Deductible: $500 vs. $1,000. Higher deductible reduces premium by ~10%-15% but increases out-of-pocket during a claim.

- Accident probability: higher for commuters.

Example calculation:

- Option A: $500 deductible, $1,800 annual premium → 3-year total with 1 accident = $5,900

- Option B: $1,000 deductible, $1,600 annual premium → 3-year total = $5,800

- → Option B slightly better.

3. Implicit Risk Cost

- Premium increase after a claim: 20%-40% for 3 years

- Denial risk: undeclared usage, lost charging equipment

- Repair waiting cost: EV repairs take longer; rental or replacement car costs if not included

4. Fuel Savings

- Unique EV advantage offsets insurance cost.

Example:

- Commute: 20 miles/day × 240 days/year = 4,800 miles/year

- Gas car: 25 mpg × $4/gallon = $0.16/mile → $768/year

- EV: 0.35 kWh/mile × $0.15/kWh = $0.0525/mile → $252/year

- Annual savings: ~$516

Conclusion: Even if EV premium is $500 higher, net cost may be equal or lower.

Part 6: How Commuters Can Optimize EV Insurance

✔ Strategy 1: When to Choose Commuting Coverage

Select commuting coverage if:

- Commuting ≥3 days/week

- Single commute >10 miles

- Route includes high-risk roads (highways, congested city roads)

- Company provides charging spots (adds charging risk)

Skip commuting coverage if:

- Commute <2 days/week

- Short, safe commute

- Vehicle mainly used on weekends

Note: Definitions and rate increases vary among insurers; compare 3+ companies.

✔ Strategy 2: When to Choose Higher Deductible

Higher deductible ($1,000 vs $500) is preferable if:

- ≥3 years no claims

- Safe driving habits

- Sufficient emergency savings

- Low vehicle usage (<8,000 miles/year)

Lower deductible preferred if:

- New drivers or frequent claims

- Parking in high-risk areas

- Tight cash flow

- Loaned or leased vehicles (some lenders require low deductible)

✔ Strategy 3: How to Record Battery Status to Protect Yourself

Daily records:

- Record range monthly at full charge

- Monitor dashboard for “battery system fault” messages

- Keep official inspection reports (at least annually)

Post-accident actions:

- Inspect chassis immediately after scraping, water exposure, or collision

- Take multi-angle photos of vehicle, damage, and road conditions

- Report within 24 hours

- Authorized center battery inspection, keep report

- Avoid “wait and see” advice; insist on written record and formal inspection

✔ Strategy 4: How to Use Usage-Based Insurance to Lower Commuting Costs

- Usage-Based Insurance (UBI) is growing, ideal for stable commutes.

- Premium = base + per-mile rate × actual mileage

Suitable if:

- <10,000 miles/year

- Fixed route and distance

- Smooth driving (few hard brakes/accelerations)

Example: U.S. Progressive Snapshot: a commuter with 8,000 miles/year saved 15%-25% on premium vs traditional policy.

References

1. Bankrate. (2026). Electric car insurance: Cost and considerations. Retrieved from https://www.bankrate.com/insurance/car/electric-car-insurance/

2. EV.com. (2026). Electric vehicles and the new logic of car insurance: How data, charging, and driving behavior shape modern premiums. Retrieved from https://ev.com/news/electric-vehicles-and-the-new-logic-of-car-insurance

3. GEICO. (2026). Electric car insurance: What EV drivers need to know. Retrieved March 26, 2026, from https://www.geico.com/information/aboutinsurance/auto/electric-car-insurance/

4. go-e. (2026, February 19). EV insurance? Here’s what you need to know. go-e Magazine. Retrieved from https://go-e.com/en/magazine/ev-insurance

About the Author:

Emily Carter is an independent automotive insurance researcher and electric vehicle specialist based in Europe. She has over 7 years of experience analyzing vehicle insurance claims, risk management, and emerging trends in EV coverage. Emily frequently contributes insights to industry reports and automotive forums, helping drivers understand the real costs, risks, and strategies for insuring electric vehicles.

Disclaimer

The content provided on this website is for informational purposes only. It is not intended to serve as professional advice, a recommendation, or an offer to sell or endorse any specific insurance product. Readers should consult licensed insurance providers or legal advisors before making insurance decisions. The author and website disclaim any liability for actions taken based on the information provided.

Recommended for you