How Does Insurance Work After an Accident in a Car-Sharing Service in the US?

——A Complete Guide to the Claims Process and Required Documents for Ride-Sharing and Car-Sharing Incidents

By Ethan M. Caldwell | Updated on March 25, 2026 | 🕓12–15 minutes

Key Highlights

- How car-sharing insurance works in the U.S. (Zipcar, Turo, Getaround)

- Step-by-step accident handling within the critical 72-hour window

- Liability determination and how it affects your compensation

- Complete claims process and required documentation

- Real-world cases, legal risks, and how to reduce out-of-pocket costs

In the United States, car-sharing has become an important transportation option for commuters in major cities. Whether you are a Zipcar user, a Turo renter, or a Getaround member, car-sharing is changing commuting habits. However, when an accident occurs, the complex insurance rules often leave many users unprepared.

According to insurance industry data, up to 80% of car-sharing accident victims fail to receive the maximum compensation within 72 hours after an accident. Misoperation, incomplete documentation, and unclear liability often lead to claim denials or delays lasting weeks or even months.

1. Basics of Car-Sharing Commuting Accident Insurance

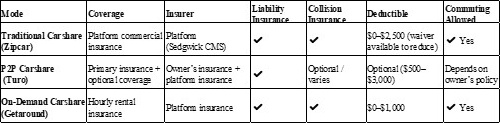

1.1 Insurance Models for Car-Sharing

The coverage mechanisms differ significantly between various car-sharing platforms:

Collision Damage Waiver (CDW): Covers damage to the vehicle itself. On Zipcar, if the waiver is not purchased, the responsible party may need to pay up to $2,500 in damages.

Liability Insurance: Covers damages to third parties (other vehicles, people, property).

Personal Auto Insurance: Most personal auto policies do not automatically cover car-sharing vehicles, especially in peer-to-peer (P2P) models. Always confirm with your insurance company before use.

1.2 Does Commuting Count as “Authorized Use”?

Zipcar and Getaround: Platform terms clearly allow commuting, and accidents during commuting are covered under insurance.

P2P Platforms (e.g., Turo): The situation is more complex. Although Turo does not prohibit commuting, vehicle owners can set restrictions in the “vehicle rules,” such as “no daily high-mileage commuting” or “for leisure use only.” If an accident occurs in violation of these restrictions, platform insurance may be denied.

Before booking a P2P vehicle, carefully read the owner’s “permitted use” terms. If commuting is essential, choose vehicles explicitly marked as “commuting allowed.”

2. Accident Determination and Insurance Responsibility Analysis

2.1 The Central Role of Liability Determination

Most U.S. states follow a fault-based system, where the party at fault bears responsibility. The proportion of fault directly affects insurance compensation:

You are fully at fault → You pay the deductible; platform insurance covers the remaining portion.

Other party fully at fault → Their insurance covers all costs; you pay nothing.

Shared fault → Costs are divided according to the percentage of responsibility.

3. Complete Claims Process

3.1 On-Site Accident Handling

Why the first 72 hours are critical: 80% of victims fail to receive maximum compensation because they miss this 72-hour window.

Step 1: Ensure Safety and Call the Police

If someone is injured, the vehicle cannot move, or liability is disputed, immediately dial 911. Provide the dispatcher with the accident location and any injuries. The police report is the best defense during insurance investigation.

Step 2: Take Comprehensive Photos

- Full 360° vehicle photos (four directions)

- Close-up photos of each damage (2 per area: wide + close)

- Clear photo of license plate

- Accident scene environment (intersections, traffic signals, road signs)

- Skid marks on the ground

- Other party’s vehicle and license plate

Getaround official photo standard: For each damaged area, take one wide shot (~2 meters) showing location and one close-up (~45 cm) showing details. Avoid reflections, darkness, blurriness, or dirt.

Step 3: Collect All Parties’ Information

Record the following:

- Other driver: Name, phone, address, driver’s license number

- Other vehicle: License plate, make, model, color

- Other insurance: Company name, policy number

- Witnesses: Name, phone, address (passengers do not count as independent witnesses)

- Damaged property (e.g., guardrails, streetlights): Owner contact information

Step 4: Record Accident Details

- Date and time of the accident

- Exact location (street, intersection, landmarks)

- Weather and road conditions

- Whether anyone was sent to the hospital and the hospital name

Step 5: Report the Accident to the Platform

Zipcar: Report as soon as possible, within 24 hours. Account is suspended until the report is submitted.

Turo: Report within 24 hours. Choose to resolve directly with the other party or submit a claim.

Getaround: Report within 5 days, 100% online. Customer service cannot submit on your behalf.

Step 6: Obtain Official Police Report

- If police are on-site, record the report number and officer’s name.

- If no police are present, go to the local police station within 24 hours.

- Some states require waiting 24–48 hours for the official report.

3.2 Platform Internal Reporting System Details

Zipcar Reporting Process:

1. Contact Zipcar to report the accident

2. Receive a link to the accident report form via SMS

3. Complete and submit the form

4. Account status updated to suspended within 3 business days

5. Claims department (Sedgwick CMS) evaluates liability and damage; this may take several weeks

Turo Reporting Process:

1. Report via app within 24 hours of the accident

2. Choose resolution: direct settlement with the other party or submit a claim

3. If submitting a claim, Turo contacts you within 24 business hours

4. Third-party appraiser assesses damage via photos (1 day) or on-site inspection (5–7 days)

If resolving directly, complete within 20 days or escalate to Turo.

Getaround Reporting Process:

1. Fill out the in-car accident report (in the glove box) at pick-up

2. Notify the vehicle owner

3. Owner submits an online report within 5 days

4. Ensure all documents are submitted to accelerate processing

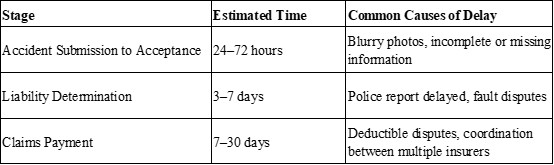

3.3 Insurance Assessment and Case Review

Minor damage: Photo-based assessment, process expected within 1 day

Moderate damage: Photo + video assessment, process typically 2–3 days

Severe damage: On-site assessment, process expected 5–7 days

Turo assessment specifics: If photo quality is poor or damage is complex, a site assessment team may be dispatched, extending assessment to 5–7 days.

3.4 Claims Review and Payout Timeline

4. Real Case References

Case A: Zipcar Rear-End Collision (Minor Damage)

User Q in Boston was rear-ended while waiting at a red light. Vehicle damage: $2,400; no injuries.

On-site handling:

Dialed 911; police provided a report

Took photos of the scene and both vehicles’ damage

Recorded the other driver’s license and insurance information

Liability Determination:

Police report assigned full fault to the other driver

Claim Path & Outcome:

Submitted report to Zipcar within 24 hours

Sedgwick CMS coordinated directly with the other party’s insurer

Repair cost $2,400 fully covered; User Q paid nothing

Claim Duration: 2 weeks

Case B: Turo P2P Accident (Multi-Vehicle Collision)

User H in Los Angeles caused a three-car rear-end collision while changing lanes and failing to yield. Minor injuries to a driver.

On-site handling:

Called 911; police arrived

Took scene photos

Provided dashcam video

Liability & Dispute:

Initial allocation: User H 70%, right-side vehicle 30%

Right-side driver disputed; liability reassessed to 50/50

Claim Outcome:

User’s protection plan deductible: $750

Platform covered remaining repair costs

Minor medical costs covered by platform liability

Total payout: $5,800; user paid $750

Claim Duration: 6 weeks (extended due to dispute)

Case C: Turo Legal Case (Third-Party Injury)

In July 2019, Josh Hermans rented a Ford Mustang via Turo from Ilia Ivanov. After drinking, he drove at 2 a.m. and hit Juan Osegueda’s car, injuring pedestrian Trejo Basurto.

Plaintiff sued Turo and owner Ivanov under the theory of “negligent entrustment.”

Court Decision:

Summary judgment in favor of Turo and Ivanov

Reason: No evidence Hermans was unfit to drive at pick-up

Turo, as “legal owner,” had statutory liability; payout capped at $15,000 per plaintiff

Case D: Ride-Sharing Insurance Exclusion

August 2021: Shante Service in a Lyft vehicle filed a claim with Progressive for an uninsured driver (SUM).

Progressive excluded “for-hire vehicles” from the policy. NYC Admin Code §19-502 classifies passenger vehicles for hire as “for-hire vehicles.”

Court Ruling: August 2025, NY Appellate Court sided with Progressive

Lyft vehicle was deemed “for-hire” and not covered under SUM

Key Takeaway: Policy language is critical; legal definitions may create unexpected coverage gaps. Passengers should also understand their insurance coverage status.

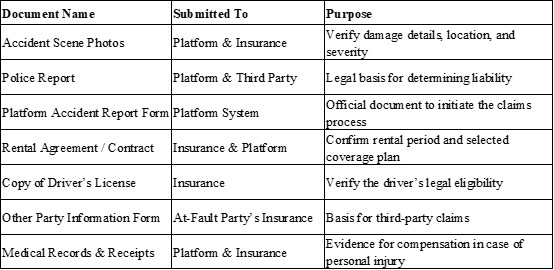

5. Required Documents for Claims

6. How to Reduce Deductible Costs

1. Purchase upgraded insurance:

Zipcar: Damage Fee Waiver reduces deductible to $0

Turo: Choose higher-tier protection plan (Premium/Plus)

2. Use specific credit cards:

Some premium cards (e.g., Chase Sapphire Reserve) offer rental insurance

Note: P2P rentals (Turo/Getaround) usually not covered by credit card insurance

3. Read terms in advance:

Zipcar: Damage fee capped at $2,500 if no violation

Turo: Deductible for each protection plan clearly stated at booking

If an accident occurs, stay calm and follow each step carefully. For personal injury or liability disputes, consult a professional lawyer. Remember—well-prepared victims receive the maximum protection.

This article is based on official Zipcar, Turo, and Getaround help documents, as well as legal case analyses. Insurance terms may update at any time; always refer to the platform’s latest policies.

FAQ

1. Will my personal auto insurance cover car-sharing accidents?

In most cases, no. Standard personal auto policies often exclude coverage for car-sharing, especially for peer-to-peer platforms like Turo or Getaround. Always confirm with your insurer.

2. Do I always have to pay a deductible?

Not necessarily.

If you are not at fault, the other party’s insurance usually pays.

If you are at fault, your deductible depends on your protection plan.

3. Can I handle the claim privately without involving the platform?

Yes, especially on platforms like Turo. However:

You must resolve it within a specified timeframe (e.g., 20 days)

If disputes arise, escalation to the platform may delay the process

4. Are passengers covered under car-sharing insurance?

Generally, yes under liability insurance, but coverage limits and conditions vary. Legal definitions (e.g., “for-hire vehicle”) may affect eligibility.

5. Does credit card rental insurance apply to Turo or Getaround?

Usually no. Most credit card benefits exclude peer-to-peer car-sharing services.

References

1. Turo. (2024). Protection Plans & Insurance Overview. Retrieved from [https://turo.com]

2. Zipcar. (2024). Damage Fee and Insurance Policy. Retrieved from [https://www.zipcar.com]

3. Getaround. (2024). Guest Liability Protection & Claims Process. Retrieved from [https://www.getaround.com]

4. Sedgwick Claims Management Services. (2023). Auto Claims Handling Procedures. Retrieved from [https://www.sedgwick.com]

About the Author

Ethan M. Caldwell

Ethan M. Caldwell is a transportation policy researcher and independent writer specializing in shared mobility systems, car-sharing platforms, and consumer insurance behavior. With a background in urban mobility studies and public policy analysis, he has spent the past 8 years researching how emerging transportation models—such as peer-to-peer car-sharing and ride-hailing—interact with traditional insurance frameworks.

Editorial Transparency Statement

This article is based on publicly available information from official platform documentation (Zipcar, Turo, Getaround), insurance regulatory bodies, and real legal case analyses.

The content is intended for informational and educational purposes only and does not constitute legal or insurance advice. While every effort has been made to ensure accuracy, insurance policies, platform rules, and legal interpretations may change over time.

Readers are encouraged to verify details directly with service providers, insurers, or licensed professionals before making decisions.

No sponsorship, paid promotion, or commercial influence was involved in the creation of this content.

Disclaimer

The information in this article should not be considered professional insurance, legal, or financial advice. Insurance coverage, exclusions, and eligibility vary widely depending on the provider, jurisdiction, and individual circumstances.

Recommended for you