How to Avoid Hidden Fees in Cross-Border Car Rental Insurance?

——Understanding Coverage for Traffic Accidents, Common Claim Denials, and How to Purchase Temporary Insurance for Emergencies

By Adrian Keller | Updated on March 20, 2026 | 🕓13 minutes

Key Highlights

- Understanding Core Policy Terms (Deductibles, Exclusions, Coverage Limits)

- How to Verify If Your Insurance Covers Cross-Border Travel

- Real Case Studies: Hidden Fees, Disputes, and Insurance Pitfalls

- Common Reasons for Claim Denials and How to Avoid Them

- Step-by-Step Claims Process After an Accident

- Temporary Insurance Options (Third-Party, Credit Card, Travel Insurance)

- Practical Strategies to Avoid Extra Fees and Disputes

Car rental insurance for cross-border driving is extremely complex. When I was driving through the Canadian Rockies, I also hesitated at the rental counter: should I buy that “zero deductible” insurance for CAD 30 per day? Later, I realized that terms like “deductible,” “exclusions,” and “geographical restrictions” in the policy can each become a reason for claim denial.

This article is based on global self-driving experiences and real-life cases. It provides an in-depth analysis of the “pitfalls” and “solutions” in cross-border rental insurance to help you make more informed decisions. Please note that this article is for experience sharing only and does not involve the sale or recommendation of any insurance products.

1. Why Is Cross-Border Rental Insurance a “Necessity”?

When driving across borders, we face unfamiliar road conditions, different traffic regulations, and language barriers in reporting accidents. The probability of incidents is much higher than in daily driving. Without proper insurance, even a minor accident can turn into a financial disaster.

2. Cross-Border Rental Insurance Basics: Understanding Your Policy

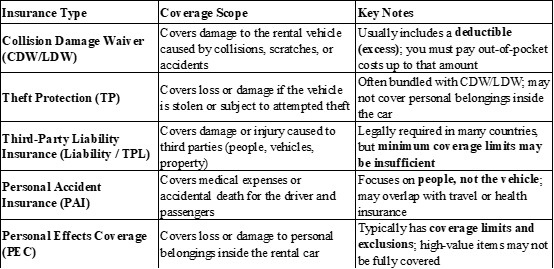

2.1 Key Types of Coverage

2.2 Deductible: The Core Concept You Must Understand

The “deductible” is the threshold you must pay before insurance coverage applies.

Deductibles vary greatly by country and region. According to Hertz data, many rental packages in the U.S. can have a $0 deductible, Canada typically around CAD 500, parts of Europe can range from €850 to €15,000, while Australia and New Zealand can reach 5,900–7,900 in local currency.

2.3 How to Determine Whether Insurance Covers Your Trip?

First, geographical coverage. Credit card rental insurance often has geographic limitations. Some users report that CIBC credit card coverage is valid across Canada and most U.S. states, but may exclude Hawaii, Alaska, and Puerto Rico. Most of Europe is covered, while Africa and South America are generally excluded. Always call your card issuer before departure to confirm.

Second, road condition restrictions. Many standard policies explicitly exclude damage caused on “unsealed roads.” This means that if you plan to visit Iceland’s highlands, Australia’s red center, or remote regions like western Tibet, your standard insurance may become invalid.

Third, vehicle type restrictions. Luxury cars, pickup trucks, and SUVs above a certain value are often excluded from standard coverage.

3. Common Pitfalls in Cross-Border Driving and Real Cases

1. New Zealand — When “Insurance” Is Actually a Pricing Trap

In February 2025, a report by Consumer NZ exposed an “insurance scam” involving the Auckland-based rental company autoUnion.

Ashwell declined a NZD 3,000 option and chose a standard insurance plan for NZD 25 per day, paying a NZD 500 deposit. Upon pickup, she found the vehicle “dirty and smelly,” but still drove away.

During the trip, the car suddenly shook violently and broke down on the highway. Staff later accused her of “using the wrong fuel.” Ashwell denied this—she owned the same model and kept fuel receipts clearly showing she used 91 octane petrol, matching the fuel cap instructions.

A few days later, she discovered that NZD 1,500 had been deducted from her debit card by “autoUnion Abu Dhabii,” with additional cross-border fees totaling NZD 1,558.

When she requested inspection reports, repair invoices, and fault details, the company sent a photo of a “half bottle of colored liquid” as supposed evidence. The repair invoice also appeared suspicious.

After disputing the charge with her bank, she successfully obtained a chargeback. On social media, she found many others reporting identical experiences: being forced to buy insurance at pickup, charged arbitrary fees upon return, and given vague responses when requesting evidence.

Consumer NZ found that autoUnion did not disclose any actual insurer behind its “insurance,” and its claim of “400+ global branches” could not be verified. When journalists visited its Auckland location, they found only a gravel lot with three cars, one clearly heavily damaged and covered with a tarp.

The CEO of the Rental Vehicle Association (RVA) stated that autoUnion is not a member, and its NZD 7/day pricing is “not economically viable,” warning consumers to stay cautious.

Takeaways:

Be cautious of rental prices far below market average—if it’s too cheap, there’s usually a catch

Verify whether the company is a member of a local rental association (e.g., RVA in New Zealand, BVRLA in the UK)

When purchasing insurance, ask: “Which insurance company underwrites this? What is the policy number?”

Keep all fuel receipts—they are critical evidence to defend yourself

2. Thailand — A Tiny Windshield Chip Leads to Maximum Liability Charge

In October 2025, the Hong Kong Consumer Council reported a cross-border rental dispute in Thailand.

Mr. Fung rented a car for 5 days at 5,000 THB. The contract stated that without purchasing Super Collision Damage Waiver (SCDW), the maximum liability would be 16,050 THB—but it did not specify repair pricing standards.

Upon return, staff pointed to a tiny chip on the windshield and demanded the full 16,050 THB—the maximum liability—rather than actual repair cost.

Due to time pressure and language barriers, he paid. After returning to Hong Kong, he filed a complaint. With mediation between Hong Kong and Thai consumer authorities, the company eventually issued a full refund.

Takeaways:

Confirm whether the contract includes detailed repair pricing standards

If charged the maximum liability instead of actual cost, raise objections immediately

Keep contact details of consumer protection agencies—you can still pursue claims after returning home

3. Portugal — Charged €340 for Insurance You Explicitly Rejected

In November 2025, a 78-year-old British couple rented a car at Faro Airport in Portugal through Avis. They had already purchased independent insurance through RAC for £33.15 and clearly declined additional insurance at the counter.

However, after returning home, they found that Avis charged €340 for insurance—more than the rental cost itself.

When they complained, Avis claimed that “your signature is on the contract.” Although the couple acknowledged the signature, they insisted the staff never disclosed the added insurance nor asked them to verify the breakdown before signing. Avis refused a refund.

A columnist from the Daily Mail noted that such situations are not uncommon—tired travelers at late-night counters often fail to review contracts carefully, and staff may take advantage by quietly adding extra charges.

Takeaways:

Even when exhausted, review all charges line by line before signing

If you don’t understand the local language, request an English version

Print your independent insurance proof and clearly state in writing: “Insurance already purchased; decline all additional coverage”

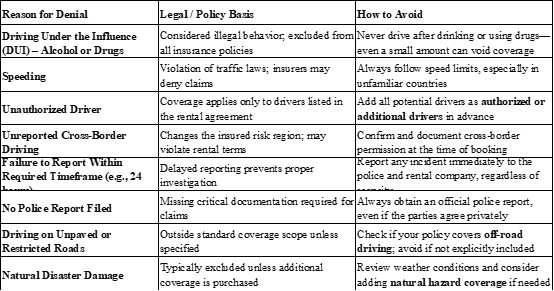

4. Common Reasons for Claim Denial (With Prevention Strategies)

5. Claims Process: What to Do After an Accident

Regardless of severity, follow these steps:

Step 1: Ensure safety and report immediately

Call emergency services if anyone is injured

Report to local police and obtain a Police Report

Notify the rental company within 24 hours (some insurers require shorter timeframes)

Step 2: Preserve the scene and collect evidence

Do not move the vehicle unless necessary for safety

Take photos: vehicle positions, damage points, skid marks, other license plates

Record the other party’s details: name, contact, plate number, insurer

Step 3: Arrange assistance and wait for processing

Follow rental company instructions for towing to designated repair centers

Keep all receipts: towing, repair estimates

Confirm next steps in the claims process with the rental company

Step 4: Submit documents and follow up

Provide required documents: passport, driver’s license, police report, repair invoices

Keep all communication records (emails, call recordings)

If disputes arise, seek help from consumer protection agencies or regulators

6. How to Purchase Temporary Insurance for Emergencies

6.1 Buy Daily Coverage via Third-Party Platforms

Many online rental platforms offer “excess reimbursement insurance” or “full coverage add-ons” to cover deductibles. These are often 30%–50% cheaper than rental counter options.

Pros: transparent pricing, easy comparison

Cons: reimbursement model—you pay upfront and claim later

6.2 Credit Card Coverage

Premium credit cards (e.g., Visa Infinite, Mastercard World Elite) often include rental collision coverage. Pay the full rental with the card and decline rental company insurance to activate it.

Key reminders:

Confirm your card includes this benefit

Check geographic coverage

Verify deductible amounts

Confirm coverage for tires, glass, and undercarriage

6.3 Comprehensive Travel Insurance

For long cross-border trips, standalone rental insurance may not be enough. Comprehensive policies often include:

Self-driving accident medical coverage

Emergency evacuation

Baggage loss/delay

Flight delay/cancellation

Confirm that your policy covers your vehicle type and planned routes before purchasing.

7. My Key Takeaways

After driving across more than ten countries, I’ve distilled three core principles:

1. Prevention First: Understand Your Insurance, Don’t Just “Buy and Forget”

Don’t rely on the label “full coverage.” Verify:

What is the deductible?

Are glass, tires, and undercarriage covered?

Is cross-border driving allowed?

Are unpaved roads covered?

Is loss-of-use included?

A simple method: save the policy PDF on your phone and review it at pickup.

2. Document Everything: Record the Entire Process

At pickup:

Take a 360° video, focusing on wheels, windshield, roof, and undercarriage edges

Include timestamp (e.g., phone clock)

Ensure all existing damage is marked on the inspection sheet

During the trip:

Keep all fuel receipts

Keep toll and parking receipts

Document any abnormal situations

At return:

Record the return process on video

Get written confirmation of “no damage” or acknowledged damage

Keep the return receipt

3. Be Flexible: Tailor Insurance to Your Trip

Short city trips (1–3 days): credit card coverage may suffice

Long cross-border trips (1+ week): consider zero-deductible coverage

Special terrain (gravel, desert): purchase specific add-ons

Family travel: prioritize personal accident coverage

The beauty of cross-border driving lies in the freedom to explore—but that freedom comes with uncertainty. Insurance is not meant to “make money,” but to hedge against risks you cannot afford. The best protection is safe driving and risk awareness—insurance terms come second.

References

1. Daily Mail. (2025, November 12). Elderly couple charged €340 for car hire insurance they explicitly declined at Portugal airport. Retrieved from https://www.dailymail.co.uk

2. Consumer NZ. (2025, February 18). Rental car trap: How one company’s ‘insurance’ left customers out of pocket. Retrieved from https://www.consumer.org.nz

3. Consumer Council. (2025, October 15). *Overseas car rental disputes: A case study on hidden charges and insurance pitfalls. Choice Magazine, (573), 24-27.

4. Hertz. (n.d.). Rental car insurance and protection products. Retrieved from https://www.hertz.com/rentacar/productservice/index.jsp?targetPage=protection_products.jsp

5. Visa. (2025). Visa Infinite® benefits guide: Auto rental collision damage waiver. Retrieved from https://www.visa.com/infinite/benefits.html

6. Mastercard. (2025). Mastercard World Elite™ benefits: Rental car insurance. Retrieved from https://www.mastercard.us/en-us/consumers/find-card-products/world-elite/benefits.html

7. CIBC. (2025). CIBC credit card insurance certificate of insurance: Auto rental collision/loss damage insurance. Retrieved from https://www.cibc.com/en/personal-banking/credit-cards/insurance.html

About the Author

Adrian Keller

Adrian Keller is an independent mobility risk researcher and cross-border travel writer with a focus on car rental insurance, international driving regulations, and consumer protection in the travel sector.

Over the past decade, he has completed self-driving journeys across Europe, North America, and Oceania, gaining extensive firsthand experience with rental systems, insurance frameworks, and cross-border compliance challenges.

Editorial Transparency Statement

This article is based on a combination of personal experience, publicly reported case studies, and information from consumer protection organizations and industry guidelines.

No sponsorships, commissions, or commercial partnerships influenced the content of this article. The purpose is solely to provide educational insights and improve consumer awareness regarding cross-border car rental insurance.

While every effort has been made to ensure accuracy, insurance policies and rental agreements vary significantly by provider, country, and individual circumstances.

Disclaimer

This article is based on personal experience and publicly available information and does not constitute insurance advice. Policy terms vary by country, rental company, and credit card issuer—always read your contract carefully and consult customer service before traveling.

The information in this article should not be considered professional insurance, legal, or financial advice. Insurance coverage, exclusions, and eligibility vary widely depending on the provider, jurisdiction, and individual circumstances.

Recommended for you