How to Choose the Best Commercial Vehicle Insurance for Urban Deliveries

——Protect Your Cargo, Minimize Operational Risks, and Learn from Real-World Case Studies (Global Guide)

By David Whitman | Updated on March 24, 2026 | 🕓15 minutes

Key Highlights

- Risk Analysis for Urban Delivery Vehicles – Driving environment, cargo, and external risks

- Insurance Type Analysis – Core and optional coverages, cargo vs. liability distinctions

- Coverage Limit Strategy – Third-party, cargo, and vehicle damage insurance considerations

- Claims Experience and Risk Control – Golden process for claims, risk management synergy

- Case Studies – Real-world international examples and lessons learned

- Global Principles and Best Practices – Universal recommendations for urban delivery insurance

On the streets and alleys of cities, millions of light trucks, refrigerated vans, and other delivery vehicles operate every day. These vehicles carry e-commerce packages, fresh food, and industrial spare parts, forming the "capillaries" of modern urban operations.

However, frequent start-stop traffic, congested roads, and complex interactions between vehicles and pedestrians make the accident rate of urban delivery vehicles much higher than that of ordinary passenger cars. More critically, when accidents occur, losses involve not only the vehicles themselves but also the value of cargo, third-party liability, and can even affect the stability of the entire supply chain.

I. Risk Analysis for Urban Delivery Vehicles

1.1 Driving Environment Risks

High-frequency stop-and-go in congested areas: On average, the number of braking events per kilometer is 6–8 times higher than on highways, leading to concentrated rear-end and scratch collisions.

Complex vehicle-pedestrian interactions: Pedestrians and non-motorized vehicles weave through traffic, increasing blind-spot accident risks.

Dense intersections: City roads average one intersection every 200–300 meters, increasing turning collision risks.

Parking difficulties: Temporary stops for loading and unloading increase the likelihood of reversing collisions or being scratched by other vehicles.

Data reference: According to statistics from a logistics industry association, the accident rate per 10,000 km for urban delivery vehicles is about 2.3 times that of long-haul trucks, with a higher proportion of accidents involving third-party injuries.

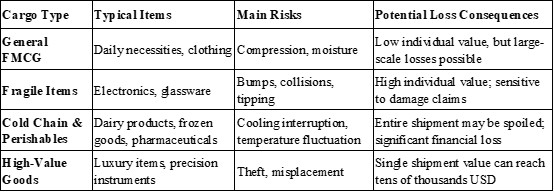

1.2 Cargo Risks

Urban deliveries involve diverse types of cargo, each with different risk profiles:

1.3 External Environment Risks

Theft and robbery: Cargo can be stolen during temporary stops, especially near logistics parks or markets.

Natural disasters: Heavy rain causing urban flooding, typhoons, or snowstorms may lead to vehicle submersion or cargo damage.

Regulatory differences: Different cities have varying regulations on freight vehicle access times, emissions standards, and restricted zones. Violating these rules may not only incur fines but also affect liability determination after accidents.

II. Insurance Type Analysis

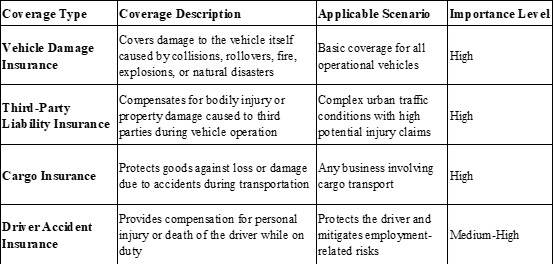

The insurance system for urban delivery vehicles consists of multiple types, each covering different risk exposures. The following tables outline core and optional coverages for reference.

2.1 Core Coverage

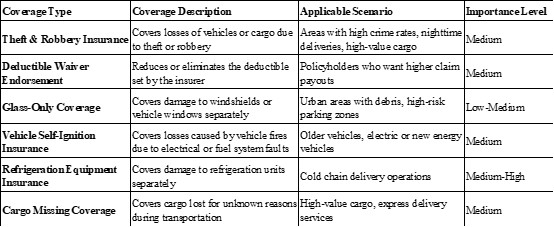

2.2 Extended and Optional Coverage

2.3 Differences Between Two Types of Cargo Coverage

In practice, companies often face a choice between “cargo transport insurance” and “logistics liability insurance,” which have different payout logic:

Cargo Transport Insurance: Protects the cargo owner's interests. After a claim, the insurer pays the cargo owner directly. If the logistics company has already compensated the cargo owner, a “transfer of rights letter” is required to receive reimbursement.

Logistics Liability Insurance: Protects the logistics company’s legal liability. The insurer pays the logistics company, which uses the funds to cover compensation owed to the cargo owner.

Recommendation: If the transport contract stipulates “carrier bears strict liability,” consider prioritizing logistics liability insurance, as its coverage aligns better with contractual obligations.

III. Coverage Limit Selection Strategy

Setting coverage limits too low may result in significant out-of-pocket costs after an accident; setting them too high increases unnecessary premiums. Reasonable limit selection should be based on risk-matching principles.

3.1 Third-Party Liability Coverage Limit: Refer to local compensation standards

The third-party liability limit should be based on the legal compensation standards of the accident location.

Regional references:

United States: High medical costs and prevalent litigation culture; limits over $1 million are common.

EU countries: High personal injury compensation standards; limits of €5 million or more are recommended.

China: In first-tier cities, death compensation is around ¥1–1.5 million; limits of ¥2–3 million are suggested, with operational vehicles possibly requiring more.

Urban delivery vehicles frequently enter commercial and residential areas, interacting with pedestrians and non-motorized vehicles. Increasing the third-party liability limit provides more comprehensive coverage with only limited premium increases.

3.2 Cargo Insurance Coverage Limit: Refer to highest single shipment value and monthly cumulative risk

Cargo insurance limits can consider two dimensions:

Single-shipment limit: Based on the highest value per order. For occasional high-value shipments, such as electronics, the limit should not be lower than the cargo value.

Cumulative limit: Based on a proportion of the total monthly cargo value. For high-frequency deliveries, even if individual shipments are not expensive, cumulative risk must be considered.

3.3 Vehicle Damage Coverage Limit: Based on actual vehicle value

Vehicle damage insurance limits are usually based on the purchase price of the vehicle, adjusted for depreciation by vehicle age. For older vehicles with lower residual value, consider lowering the vehicle damage limit and redirecting premium resources to liability and cargo insurance.

IV. Claims Experience and Risk Control

4.1 “Golden Process” for Claims Handling

After an accident, the following steps help ensure smooth claims:

1. On-site handling and evidence collection

Call emergency services immediately if there are injuries.

File a police report for official accident recognition; this is the core basis for claims.

Take photos of the scene: vehicle positions, collision points, brake marks, full environment, other vehicles, and personnel information.

Record witness contact information.

2. Timely reporting

Most policies require reporting within 48 hours of the incident.

Late reporting may prevent the insurer from assessing losses and affect compensation.

Recommend companies establish an internal policy of “reporting any accident immediately.”

3. Damage assessment and repairs

Confirm whether the policy allows repairs at non-approved shops.

Some policies specify approved repair centers to control costs; using others may result in insufficient coverage.

Keep all repair receipts and invoices.

4.2 Risk Control and Insurance Synergy

Insurance transfers risk, while risk control reduces accident probability. Combining both produces better outcomes. Effective measures include:

Driver safety training to raise awareness and standardize driving behavior.

Regular vehicle maintenance to reduce mechanical failures.

Onboard monitoring systems to track driving behavior and provide accident evidence.

GPS driving records to reconstruct accidents and prevent fraudulent claims.

Some insurers offer premium discounts for fleets equipped with standard active safety systems (ADAS, Driver Status Monitoring), reducing costs directly.

V. Case Studies

The following cases are sourced from real international claims and industry reports, covering North America, Europe, and Asia. They aim to highlight key experiences and lessons in urban delivery vehicle insurance selection.

Case 1: U.S. Delivery Driver — $25,000 “Insurance Blind Spot”

Karen Soileau in Louisiana used her personal car to deliver food for Uber Eats. After a rear-end collision, the insurer denied the claim due to “no coverage for delivery-related business,” leaving $25,000 in repair costs unpaid.

Personal auto insurance does not cover any commercial delivery activities, even while “waiting for orders.” Delivery work requires Rideshare/Delivery Endorsement; otherwise, personal insurance will not cover accidents during commercial use.

Case 2: Wisconsin Legal Precedent — “App On” Does Not Equal “Delivering”

A DoorDash driver, after completing an order, drove to a busy area awaiting the next assignment and collided with another vehicle, injuring a passenger. Personal insurance denied the claim due to “related to delivery business,” and platform insurance only covered “actively delivering.”

Court ruling: overturned insurer’s stance, ruling that “app on but no active order” should still be covered by personal insurance. Ambiguous contract disclaimers can be invalidated by courts; “grey period” coverage is a high-risk area for disputes.

Case 3: EU Cross-Border Transport — Evidence Determines Claim Success

Battery products shipped from Asia to Germany were damaged by storm-induced water ingress in containers. The cargo owner had transport insurance, and the claims team provided:

Photos documenting packaging failure

Electronic data proving the weather event

Packing lists confirming cargo value

Result: full compensation, settled in 32 days.

Cross-border cargo claims hinge on complete evidence—photos, data, and documentation are all necessary. Reporting within 24–48 hours is the industry standard.

Case 4: Canada Subrogation — Importance of Carrier Liability Insurance

A multimodal shipment from China to Toronto was involved in a traffic accident in Ontario, destroying 156 cargo items with losses exceeding $500,000. After cargo insurance compensated the owner, the insurer exercised subrogation rights against the logistics provider.

The provider argued they were only a “transport agent” and that under Canadian law, liability was limited to CAD 4.41 per kilogram.

Arbitration: the logistics provider was deemed a full multimodal operator, responsible for the entire cargo loss. Foreign legal limits did not apply because they were not transparently disclosed in the contract, and the shipper did not declare value.

Lesson: Insurance claims do not equal the end of liability. Carriers without adequate liability coverage may face subrogation. Declaring cargo value is crucial to bypass foreign legal limits.

The above cases point to a common conclusion: urban delivery insurance cannot stop at “buying a policy.” It must match the business model, operational scenario, and legal environment, supported by continuous risk management.

Global Principles

Regardless of country or region, the following principles are universal:

Vehicle usage must be accurately disclosed — the premium difference between commercial and non-commercial is far less than the loss from denied claims.

Third-party liability limits should be high — premium increases are limited, but risk coverage improves significantly.

Cargo vs. liability insurance choice should match contracts — understand payout differences and choose coverage consistent with contractual obligations.

Deductibles should match risk tolerance — trade predictable small out-of-pocket risk for premium savings.

Insurance and risk control should operate synergistically — onboard monitoring and driver training are both management tools and effective cost-control measures.

References

1. Lizbeth Hernandez Ramirez v. Voyager Indemnity Insurance Company, No. 2024AP000786 (Wis. Ct. App. Mar. 10, 2026).

2. Khan v. Delivery Hero Food Hong Kong Ltd, [2025] HKCFI 4030 (CFI).

3. WBRZ. (2026, March 17). Delivery driver blindsided by 'ride-share' insurance policy, on the hook for $25K repair bill. WBRZ News.

4. Insurance Business America. (2026, March 11). Wisconsin court rejects insurer's gig delivery exclusion as ambiguous. Insurance Business Magazine.

5. Boase Cohen & Collins. (2025, October 2). Court ruling delivers food for thought. BC&C News.

About the Author:

David Whitman, Insurance & Logistics Analyst, London, UK. David is an industry practitioner specializing in commercial vehicle insurance and urban logistics risk management, with over 12 years of experience advising European and North American delivery fleets. He has published multiple reports on insurance claims trends, risk mitigation strategies, and cross-border freight insurance best practices.

Editorial Transparency Statement

This article is based on publicly available information, industry reports, and legal case references. No insurance company or product is promoted. All recommendations are intended for educational and informational purposes. Any examples provided are for illustrative purposes only and do not constitute specific advice or endorsements.

Disclaimers

This content is compiled from industry-standard experience and publicly available information and does not constitute specific legal or insurance advice. Always read insurance policy terms carefully and make decisions based on your actual business circumstances.

All information for reference only and does not advertise, promote, or sell insurance products.

Recommended for you