Renting a Car in the Schengen Area vs. Using Your Own Vehicle: What’s the Difference in Cross-Border Insurance?

——Understanding the Key Differences Between Rental Car Insurance and Personal Auto Insurance for European Road Trips

By James Thornton | Updated on March 24, 2026 | 🕓15–20 minutes

Key Highlights

- Core Concepts: Rental Car Insurance vs. Personal Auto Insurance

- Cross-Border Coverage Differences

- Claims Process: Rental vs. Personal Vehicle

- Cost Comparison: Short-Term vs. Long-Term Driving

- Risk Management: Deductibles & Exclusions

- Convenience & Flexibility: Rental vs. Own Vehicle

- License Legality and Insurance Validity

- Practical Tips: Parking, Fuel, Speed Limits, and Rental Decisions

- Recommended Strategies for Different Travelers

Last summer, my friend Noah had a “nightmare” while driving in Europe. He rented a car in Spain, planning to drive all the way to France. On the highway near Barcelona, his side mirror was scraped by a truck. At the time, he wasn’t worried—after all, he had purchased the CDW (Collision Damage Waiver) recommended by the rental company.

However, when returning the car, the rental company told him: the insurance was invalid, and he had to pay €1,800 for repairs out of pocket. The reason was simple: he drove the car outside Spain without written permission from the rental company.

“I thought the Schengen Area had no border checks, so insurance should automatically cover cross-border travel!” Noah’s confusion is a common misconception among many European road-trippers.

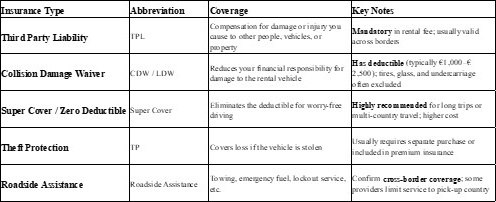

1. Core Concepts: Two Completely Different Insurance Logics

1.1 Rental Car Insurance: Package Coverage, Terms Rule Everything

In Europe, rental car insurance usually comes as a “package.” Basic coverage is often included in the rental price, while more comprehensive protection requires an additional fee.

1.2 Personal Auto Insurance: Coverage Based on Vehicle Registration

If you drive your own car (or a long-term leased vehicle) into the Schengen Area, a different set of rules applies.

Core Legal Basis: EU Directive 2009/103/EC stipulates that vehicles registered in the EU have their third-party liability insurance automatically valid in all member states. Your license plate serves as proof of insurance.

1.3 Quick Comparison Table of Core Differences

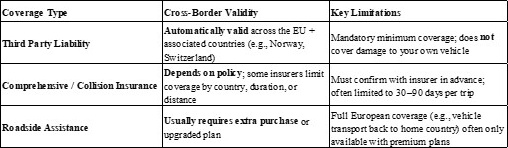

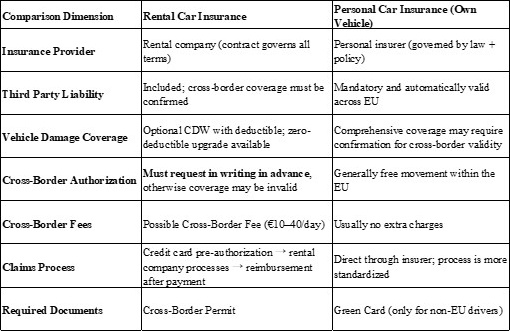

2. In-Depth Comparison: Six Key Dimensions

Dimension 1: Cross-Border Coverage – Rentals Have “No-Go Zones,” Personal Cars Are Freer

Rental Cars: Which countries are off-limits?

Rental companies’ cross-border permissions are not universal. The following countries/regions are usually prohibited or strictly restricted:

- Strictly prohibited: Albania, Bosnia & Herzegovina, Serbia, North Macedonia, Ukraine, Belarus, Russia

- Restricted entry: Turkey, Bulgaria, Romania (special permission and extra fees required)

- High-value vehicles: BMW, Audi, and other luxury cars are often prohibited from leaving the country

Real Case: At AVIS Slovakia, driving to Albania, Serbia, or other Eastern European countries is explicitly forbidden. If an accident occurs in these areas, all insurance coverage is immediately voided.

Personal Car: EU travel is largely unrestricted

EU law clearly states: vehicles registered in the EU or associated countries (Norway, Switzerland, Iceland, Liechtenstein, etc.) have third-party liability automatically covering all member states. No documents are required at the border—your license plate is proof of insurance.

Note: If you plan to stay in the EU for more than 6 months, you must register your vehicle locally and purchase local insurance, otherwise foreign insurance becomes invalid.

Dimension 2: Claims Process – Rental Cars “Prepay, Then Claim,” Personal Cars “Direct Settlement”

Case 1: Rental Company Insurance Nightmare

Xiao Li, a Chinese tourist with a Chinese driver’s license and IDP, rented a car at Munich Airport, Germany, planning to drive through Austria, Italy, and Switzerland for 12 days. He rented from Sixt, purchased CDW with a €1,000 deductible, and did not buy zero-deductible coverage.

On day 5 in Innsbruck, Austria, he accidentally scraped a pillar in a narrow underground parking lot. The scratch was about 20 cm on the rear door, not affecting the paint or driving.

Three correct actions he took:

1. Photographed the damage – close-ups and scene panorama

2. Contacted the rental company – reported the incident to customer service

3. Kept all receipts and records – rental contract, insurance terms, call logs

Key mistake: He thought the minor scratch wasn’t serious and did not report to local police or fill out a European Accident Statement.

Returning the car on day 12, the rental staff assessed:

- Repair cost estimate: €850

- Loss of Use fee: 3 days × €89/day = €267

- Administrative fee: €50

- Total: €1,167

With a €1,000 CDW deductible, his credit card was pre-authorized for €1,000. Upon returning home, he faced a 3-month claims battle. His credit card insurance required a police report, but Sixt delayed providing detailed documentation. Ultimately, only €459 was reimbursed; €541 was paid out of pocket.

Spending €150 extra for zero-deductible coverage or reporting to the local police would have avoided months of hassle.

Case 2: Third-Party Supplemental Insurance Smooth Experience

A traveler rented a car in Hungary and purchased RentalCover, a UK-based supplemental insurance company. Although unfamiliar with the company, the coverage was comprehensive and cheaper than the rental company’s own insurance.

Coverage highlights:

- Full reimbursement of self-pay costs

- Theft, fire, vandalism, windshields, towing, tires, headlights, keys, roof and undercarriage

- Any single- or multi-car accident depending on the policy

- Damage caused by animals, water, or weather

- Covers credit card fees, administrative fees, and rental company charges

The traveler returned the car after hours, leaving the key in a Drop Box. The next day, the rental company claimed a €164 repair/admin fee for a windshield chip.

Claims Process:

1. Enter policy details on RentalCover website

2. Submit incident description and upload documents (license, passport, rental contract, receipts, car damage report)

3. Identity verification via passport and license

Result:

- May 11: Claim submitted

- May 12: Approval email

- May 13: Payment received (€176 USD equivalent)

All within 72 hours, no phone calls, no additional documents, no hassle.

3: Cost Analysis – Short-Term Rental vs. Long-Term Personal Driving

Short-Term Travelers (7–14 days)

Example: Mid-size car in Germany for one week.

- Base insurance included CDW with €1,000 deductible

- Cross-border coverage for 2–3 countries: additional €70 (€10/day)

- Deposit freeze: €1,500–2,000

- Total cost: €370 (with €1,000 deductible risk)

Zero-deductible coverage: extra €140 (€20/day), deposit reduced to €300–500, total €510.

Recommendation: Short-term travelers should purchase zero-deductible coverage or third-party supplemental insurance to avoid potential thousands in repair costs.

Long-Term Travelers (1–3 months)

Long-term rental with full coverage: €1,500–2,500/month

- Flexible, new car, can return at different locations

- Limitations: expensive, cross-border restrictions apply

Personal car with local insurance: €50–150/month

- Much lower cost, full freedom, no cross-border restrictions

- Drawback: must handle vehicle import, registration, paperwork

4: Risk Control – Deductibles and “Black Hole Clauses”

Rental Insurance “Black Hole Clauses”

Even with CDW, typically not covered:

❌ Tires (punctures, blowouts)

❌ Windshields and windows

❌ Roof and undercarriage

❌ Personal belongings inside car

❌ Loss of Use fees

Solution: Buy zero-deductible full coverage or third-party supplemental insurance (like RentalCover).

Credit Card Insurance:

- Must pay full rental with the card

- Often excludes third-party liability

- Coverage limited (30–45 days)

- Some countries/models excluded (Ireland, Italy, luxury cars)

- Reimbursement “after-the-fact,” must prepay costs

Personal Insurance Risks:

Some policies only cover 150 km abroad, or only minimal third-party liability overseas. Always confirm in writing before departure.

5: Convenience & Flexibility – Rental “Easy but Restricted,” Personal Car “Free but Complex”

Rental Car

Pros:

- Convenient pickup/return (airports, train stations)

- New car, reliable condition

- Full coverage allows “key handover” convenience

Cons:

- Cross-border travel requires pre-approval

- One-way drop-off fees high (€50–200, up to €300–1,000 cross-border)

- Deposit freeze (€500–2,000)

Personal Car

Pros:

- True freedom

- No cross-border restrictions or fees

- Lower cost for long-term travel

Cons:

- Need international driving permit, green card, etc.

- Vehicle registration, insurance, inspection require planning

- Non-EU plates may require border insurance

Freeway speed limits europe

6: Driver’s License Legality – Hidden Threshold for Insurance Validity

Before insurance, ask: is your license recognized by the rental or insurance company?

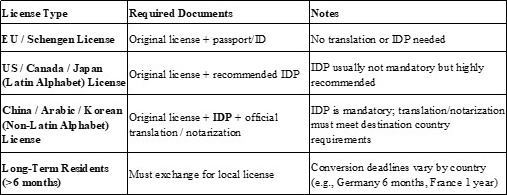

1. EU/Schengen Licenses

- Fully mutually recognized

- No notarization, translation, or IDP needed

- Rental company requires license + passport/ID

Example: German license valid in France, Italy, Spain; French license valid in Germany, Netherlands, etc.

2. Non-EU Licenses (US, China, Canada, etc.)

Three main hurdles:

Hurdle 1: Validity period – generally 3–6 months

Hurdle 2: Language & format – non-Latin licenses require:

- IDP (1-year validity, must carry original license)

- Official translation for some countries (Italy, Spain)

Hurdle 3: Country-specific rules – Spain: translation/notarization; Italy: notarized translation; France: IDP sufficient; Germany: IDP or official translation.

3. Rental Company Practices

- International chains (Avis, Hertz, Europcar): standardized, accept IDP + license

- Local companies: stricter, may reject non-EU licenses

- Chinese licenses: IDP + notarized translation usually required

4. Why License Affects Insurance

Insurance companies first check:

- Is the license valid?

- Within allowed driving period?

- Required translation/IDP present?

If not, insurance can be void, leaving you responsible for all damages.

Pre-Departure Checklist

3. Practical Recommendations: Strategies for Different Travelers

Strategy A: Short-Term Travelers (7–30 days)

Recommendation: Rental car + third-party supplemental insurance (e.g., RentalCover) or zero-deductible coverage

Steps:

1. Choose major brands (Hertz, Avis, Europcar)

2. Pre-purchase supplemental insurance online (cheaper than desk)

3. Confirm cross-border plan in writing; obtain Cross-Border Permit

4. Pay with primary driver’s credit card (sufficient limit)

Tips: Check toll systems and mandatory equipment (winter tires).

Strategy B: Long-Term Cross-Border Travelers (1–6 months)

Recommendation: Personal car + international insurance

Steps:

1. Confirm vehicle registration: EU plate > non-EU green card > others

2. Contact insurance 6 weeks ahead:

- Full coverage across all destinations?

- Any time limits?

- Green card required (for non-EU)?

3. Carry: registration, insurance, IDP

Tips: Stay under 6 months in EU without local registration; non-EU plates need border insurance.

Strategy C: Digital Nomads / Over 6 Months Stay

Recommendation: Purchase or lease locally

Steps:

1. Register vehicle locally

2. Buy local insurance (using No-Claim Bonus if available)

3. Or long-term rental (1–12 months), usually international coverage included

4. On-Road Practical Tips: Parking, Fuel, Speed Limits & Rental Decisions

Insurance covers “accidents,” but many costs arise from unfamiliar local rules.

4.1 Pickup & Return: Two Common Pitfalls

Pickup:

- Airport: go to counter, submit documents, collect parking garage key

- Door-to-door delivery: check legal parking at handover point

Return: Full Tank Policy

- “Full-to-full” standard; failure may cost 1.5–2x market fuel price + service fee

- Keep receipt

Fines:

- Credit card pre-authorized for any fines + admin fee (€20–50)

- On-the-spot payment possible; always request official receipt

4.2 Fuel Guide: Diesel or Gasoline? Wrong Fuel May Void Insurance

Self-service and attended stations exist. Fatal error: wrong fuel type → engine damage, often excluded from rental insurance.

Three key steps:

1. Check fuel type on cap

2. Confirm fuel gun color (diesel: black/yellow, gasoline: green)

3. Ask staff if unsure

Price differences: Cheapest: Andorra, Poland, Hungary; Medium: Germany, France, Spain; Most expensive: Netherlands, Italy, Norway, Greece

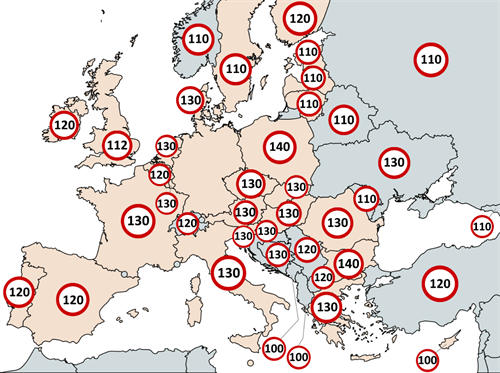

4.3 Speed Limits & Fines: Cameras Everywhere

City: usually 50 km/h, residential/school zones 30 km/h.

Suburbs: 70–100 km/h.

Highways: 110–130 km/h; some German sections unrestricted. Rain/snow: reduce by ~20 km/h.

Rental insurance may deny claims for serious overspeed (>50% over limit).

Fine handling: rental company charges credit card + admin fee.

4.4 Rental Decision: Not Everywhere is Suitable for Driving

Ask yourself:

1. Road conditions – mountains, narrow roads, gravel, snow

2. Traffic rules – right-of-way, red-light turns, tolls, vignettes

3. Booking vs. driver name – must match credit card and actual driver

4.5 Official Website vs. Third-Party Platforms

Third-party “full coverage” ≠ rental company’s desk full coverage. Check if it covers tires, glass, undercarriage, Loss of Use.

4.6 Common Exclusions

- Driving on prohibited roads (gravel, off-road, closed areas)

- Water damage (engine flooded)

- Wrong fuel

- Illegal behavior (DUI, drugs, fatigue, overspeed >50%)

- Driving in prohibited countries without permission

- Invalid license or missing IDP/translation

Tip: Spend an hour before departure checking insurance terms, driver’s license, cross-border permissions, and traffic rules to avoid nightmare claims.

Drive safely and enjoy Europe!

References

1. European Commission. (2009). Directive 2009/103/EC on insurance against civil liability in respect of the use of motor vehicles. Official Journal of the European Union.

2. RentalCover. (2024). Cross-border car rental insurance guide. Retrieved from [https://www.rentalcover.com](https://www.rentalcover.com)

3. Sixt SE. (2023). Terms and conditions for cross-border rentals. Retrieved from [https://www.sixt.com](https://www.sixt.com)

4. European Commission. (2022). Driving in the EU: Rules and insurance requirements. Retrieved from [https://ec.europa.eu/transport](https://ec.europa.eu/transport)

5. International Driving Permit (IDP) Guidelines. (2023). IDP requirements for non-EU travelers in Europe. International Automobile Federation.

About the Author

James Thornton is an experienced automotive insurance consultant and travel writer based in the UK. He has over 10 years of experience advising international travelers on cross-border driving and vehicle insurance.

Editorial Transparency Statement

This article was written based on personal experiences, industry-standard insurance guidelines, and verified information from rental companies and European Union regulations. No financial or sponsorship incentives from rental or insurance companies influenced the content. All recommendations are provided solely to inform and guide travelers about insurance choices and practical considerations for European road trips.

Disclaimer

The information in this article should not be considered professional insurance, legal, or financial advice. Insurance coverage, exclusions, and eligibility vary widely depending on the provider, jurisdiction, and individual circumstances.

Recommended for you