How Insurance Claims Work After an Accident in Shared Mobility Vehicles

—— Ride-Hailing, Car-Sharing, and Micromobility Explained

By Jonathan Reed | Updated on March 24, 2026 | 🕓18–22 minutes

Key Highlights

- How does the status of a ride-hailing app affect insurance coverage?

- What are the key differences between primary and secondary insurance in car-sharing platforms like Turo?

- Why might micromobility platforms refuse to pay for injuries, even when you are the victim?

- What documents are essential for filing a claim in each type of shared mobility accident?

- How do cross-border incidents impact insurance claims and coverage limits?

In the spring of 2024, Carlos Campos in Miami received a phone call that changed his life. He was informed that a wrongful death lawsuit for his daughter, who had died in a backing accident two years earlier at the age of six, had been dismissed by the Florida Third District Court of Appeal. The reason was simple: at the time of the accident, the Uber driver’s app was not active.

In the same year, on the other side of the planet in Melbourne, Australia, 60-year-old university scholar Julia Miller was struggling with a medical bill of AUD 25,000. She had been walking on the sidewalk when she was hit by a Lime e-scooter, resulting in fractures to her shoulder and elbow, necrosis in her ankle, and blood clots in her leg—hospitalized for 12 days. But the scooter company Lime told her: “Sorry, we don’t cover this.”

Meanwhile, in Texas, a Turo rental user named John (alias) encountered a deer collision in Idaho—the car was towed, airbags deployed—but when he filed a claim with his insurer Progressive, he received a rejection letter stating: “Vehicles under personal vehicle sharing plans are not covered.”

Three incidents, three shared mobility methods, three completely different outcomes.

This is not a coincidence. It is the new reality everyone must face in the era of shared mobility: the type of tool you use determines which set of insurance rules applies to you.

Chapter 1: Ride-Hailing — When “App Status” Becomes a Million-Dollar Boundary

Case Review: Campos v. Uber

One day in 2017, an Uber driver in Florida, Castillo, was running personal errands—driving his daughter to his ex-wife’s house. While reversing, his six-year-old daughter ran behind the car and was hit, resulting in her death.

Two years later, the executor of the child’s estate, Campos, filed a wrongful death lawsuit against Castillo and Uber. The core argument was that Castillo might have been logged into Uber on another phone at the time, meaning he could have been “working for Uber” when the accident occurred.

Uber checked internal records, showing that Castillo had not logged into the Uber app for over five months before the accident.

The Florida Third District Court of Appeal made a clear ruling: for Uber to be held liable under employer responsibility, it must be proven that the driver was “working within the scope of employment” at the time of the accident. Since the Uber app was not active, the driver was conducting personal business—Uber bore no liability.

This case reveals the core truth of ride-hailing claims: everything depends on app status.

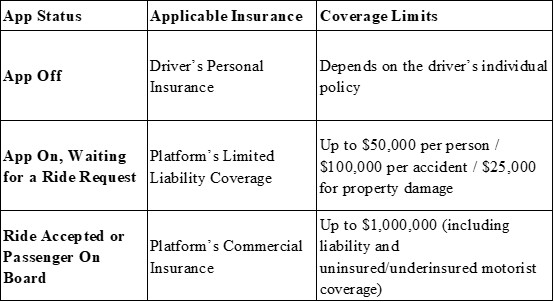

In-Depth Analysis: Uber and Lyft’s Three-Layer Insurance Structure

In states like California, Uber and Lyft operate with tiered insurance that triggers based on app activity:

Notice: the $1,000,000 coverage only activates when the driver is in “ride accepted” or “with passenger” status. If you are rear-ended as a passenger while the driver is merely waiting for a ride request, you can only claim up to $50,000 for bodily injury—not $1,000,000.

A Real Claim Negotiation Case

A passenger in San Diego was injured in a ride-hailing accident when the Uber driver was side-swiped by a speeding car. Uber initially denied coverage, stating the “app was inactive.” After a lawyer intervened, using app logs and dashcam data to prove the driver was indeed transporting a passenger, the settlement increased from $30,000 to $200,000.

Document Logic: One Extra Layer of “Platform Evidence”

The core documents for ride-hailing claims differ from traditional car accidents:

1. App status evidence: trip screenshots, GPS timestamps, app logs—this is the “key” that triggers platform insurance.

2. Police report: records the accident time for comparison with trip times.

3. Medical records: especially soft tissue injuries (like whiplash) which may not show on X-rays and are often disputed.

4. Driver and other vehicle information: including insurance policy numbers.

Risk Points: Why Ride-Hailing Claims Are Prone to Failure

Point 1: Status Disputes

Platforms may claim “not on a trip at the time.” Countermeasure: immediately screenshot trip records and GPS timestamps. Uber and Lyft digital logs can be obtained through legal procedures.

Point 2: Multiple Insurers Passing the Buck

Platforms may require the driver’s personal insurance to pay first; if denied, the platform may delay or deny coverage. Countermeasure: notify all parties concurrently—don’t wait for one to respond before starting another.

Point 3: Multiple Passengers Splitting Limits

If four passengers are injured, the $1,000,000 policy limit is shared. Countermeasure: get legal or insurance representation early to avoid your share being diluted.

Point 4: Soft Tissue Injury Disputes

Whiplash and other soft tissue injuries are invisible on X-rays; insurers often downplay compensation. Countermeasure: seek immediate medical care and maintain continuous documentation.

Chapter 2: Car-Sharing — When “I thought insurance covered me” Becomes the Most Expensive Words

Case Review: Turo Renter’s Nightmare

A Texas user rented a car on Turo in Idaho and hit a deer, causing severe damage and airbag deployment. Filing a claim with Progressive, he received:

“Your policy includes an exclusion: vehicles used in personal vehicle sharing plans are not covered.”

Ironically, before filing the claim, Progressive’s online agent had assured him that coverage would extend to vehicles rented via Turo, Zipcar, or other car-sharing services. Written policy terms overrode the agent’s statement. The user ultimately had to cover the costs himself—or hire a lawyer to challenge the denial.

In-Depth Analysis: Turo Insurance “Secondary” Trap

Turo’s protection plans are secondary insurance.

What is secondary insurance? Your personal auto insurance pays first; Turo only covers the excess.

Implications:

a) If your personal insurance excludes shared vehicles (common), Turo’s secondary insurance may never activate.

b) Even if your personal insurance covers, claims can raise your premiums.

c) Coverage gaps may leave you personally responsible for portions between your primary policy exclusion and Turo’s limits.

Risk Points: Five Hidden Car-Sharing Traps

1. Secondary Insurance Misunderstanding: Believing “platform insurance” is sufficient may leave you unprotected.

2. Not Purchasing Zero Deductible: Basic plans often have high deductibles—accidents may cost thousands out-of-pocket.

3. No Photo Evidence: Without timestamped photos at pickup, any new damage at return may be charged to you.

4. Cross-Region Use: Many platforms limit operating areas; driving outside voids coverage.

5. Violating Terms: Smoking fines $150–$500, pets $150–$500, late return fees—platform decides unilaterally; appeals rarely succeed.

Chapter 3: Micromobility — When “Platform Won’t Pay” Becomes the Default

Case Review: Julia Miller’s AUD 25,000 Bill

On April 1, 2022, in Melbourne, Australia, 60-year-old scholar Julia Miller was walking along a side road near the William Barak Bridge with her son and partner.

Suddenly, a Lime e-scooter collided with her. Hospitalized for 12 days, diagnoses included:

1. Fractured shoulder

2. Fractured elbow

3. Sprained left ankle

4. Right ankle hematoma developing into necrosis

5. Leg blood clots

Medical bill: AUD 25,000.

The scooter operator was a 20-year-old woman. Police issued two fines: no helmet and improper use, totaling over AUD 400.

Would Lime cover it?

Answer: No.

Because the rider violated traffic rules, Lime’s insurance invoked the exemption clause. Julia’s lawyer Alice Robinson called it “junk insurance”—the rider violated rules, the victim pays.

Additional Examples

In 2019, Lime user Hayley Adamson in Brisbane suffered:

- Jaw fracture

- Seven teeth broken

- Mandible fracture

- Suspected spinal fracture

Dental bills totaled AUD 14,000; Lime offered nearly AUD 10,000 only if a confidentiality agreement was signed—essentially a “settlement” not compensation. Lime’s press release emphasized “help” for riders, not “compensation.”

In-Depth Analysis: Micromobility Insurance Reality

Platform insurance vs user expectation:

- Platform coverage: usually third-party liability—covers rider’s harm to others, not rider’s own injury.

- User intuition: “The platform should ensure my safety.”

Document priorities differ:

a) Medical records: ER notes, bills, diagnosis reports (core evidence)

b) Usage records: App ride logs, timestamps, route

c) Device malfunction evidence: photos, app error logs, third-party inspection (hard to collect)

d) Third-party information: if collision involved others, record info and liability

Risk Points: Three Common Misconceptions

1. “Platform will pay” → often false; platform insurance covers your liability to others, not your injuries.

2. “If I didn’t violate rules, I’m covered” → false; violations by riders may void coverage even for injured pedestrians.

3. “No immediate medical record → can skip treatment” → false; no records = no claim possibility.

Micromobility claims logic: don’t rely on the platform. Check personal health, accident, or travel insurance first.

Chapter 4: International Perspective — When Shared Mobility Crosses Borders

For frequent cross-border travelers, shared mobility insurance issues become more complex.

USA: Three-layer insurance is clear, but enforcement varies

- California: app status determines insurance tier.

- Foreign tourists may face slow claims, taking months or years.

Australia: Micromobility “violation exemption” trap

- Julia’s case exposed a loophole: any rider violation voids platform coverage.

- Experts call for a real pedestrian protection insurance mechanism.

China: “Nature of Use” disputes in ride-sharing

- Courts consider order frequency, routes, cost-sharing to determine if vehicles “change purpose.”

- 2022 case: driver Xiao Zhang rear-ended on highway, 1 passenger dead, 1 injured; paid 970,000 CNY then claimed insurance.

- Insurer refused: “vehicle changed business use.”

- Court ruled: average <2 orders/day, reasonable routes, vehicle purpose not changed → insurer must pay 300,000 CNY.

- Conclusion: real ride-sharing protected; pseudo-commercial ride-sharing penalized.

Cross-Border Car-Sharing: Three Traps

1. Driver license: most platforms require local + international license; non-compliance voids coverage.

2. Operating area: driving outside specified region = no coverage.

3. Credit card insurance: many exclude shared/car-sharing vehicles.

Chapter 5: Post-Accident Decision Guide — Who to Contact?

No matter the country or mobility tool, you can quickly determine the next steps after an accident:

Step 1: Identify Your Mode

- Someone drives, you are a passenger → Ride-hailing channel

- You drive, vehicle rented by hour/day → Car-sharing channel

- You ride/skim scooter/bike → Micromobility channel

Step 2: Take Corresponding Action

Ride-Hailing:

- Call police + report via app

- Screenshot trip logs + GPS timestamps immediately

- Collect driver name, license plate, insurer info

- Notify platform and all relevant insurers simultaneously

- Consult lawyer before accepting compensation for bodily injuries

Car-Sharing:

- Notify platform within 24 hours

- Retrieve timestamped pickup photos (if any)

- Review rental contract to confirm insurance plan

- Understand deductible and cost structure

- If dispute arises, do not accept unilateral platform determination

Micromobility:

- Call police (if others involved) + app report

- Seek immediate medical care; preserve all medical records

- Confirm personal health/accident/travel insurance coverage

- Don’t wait for platform “to pay”—often won’t

- If equipment malfunction suspected, photograph brakes, scooter body, app error

Shared Mobility: Convenience and Boundaries

Over the past decade, shared mobility has transformed urban transport. It brings convenience but also redefines the boundary between mobility and responsibility.

When we unlock a scooter, tap to book a ride, or swipe to rent a car, we engage with a complex legal and insurance ecosystem. Its logic does not always align with our intuitive sense that “service providers should be responsible.”

Understanding these differences is not to find “who pays” after an accident, but to know what rules you face before using these tools.

Every trip is a choice. And behind every choice, a set of rules quietly operates. Knowing them is the prerequisite for coexisting safely with shared mobility.

References

1. West Coast Trial Lawyers. Who Pays in a Lyft or Uber Crash in California? 2025.

2. Tokmakov, Sergei. Turo Terms of Service Review. ToS Watchdog, 2026.

3. Westgarth, Georgia. ‘I was doing nothing wrong’: Woman left with $25k medical bill after eScooter crashed into her. Nine News, 2022.

4. Taylor, Warren, Weidner, Hancock & Barnes. Uber Liability Turns on Whether Driver Was Logged Into Uber App At Time of Accident. 2025.

5. Tokmakov, Sergei. Car Sharing Platform Terms Reviews. ToS Watchdog, 2026.

6. 7NEWS. Injured Lime Scooter rider says she was offered money for medical bills. 2019.

7. Hagens Berman. Tesla & Rideshare Incident Claims. 2025.

8. Avvo. Can I challenge a Claim Denial decision from my Progressive Auto Insurance? 2025.

About the Author

Jonathan Reed

Jonathan Reed is an insurance and transportation industry analyst with over 12 years of experience covering vehicle insurance, ride-sharing, and emerging mobility platforms. He has consulted for mobility startups in North America and Europe, providing insights into risk management and claims optimization.

Editorial Transparency Statement

This article has been independently researched and compiled based on publicly available case studies, platform insurance policies, and court rulings. It is designed to provide factual information and practical guidance for readers and does not involve promotion or sale of any insurance products. All interpretations and recommendations are made in good faith to inform readers of potential risks and procedures in shared mobility insurance claims.

Disclaimer

The content of this article is for informational purposes only and should not be considered legal, financial, or insurance advice. Readers should consult their insurance providers, legal counsel, or relevant authorities for guidance tailored to their specific circumstances. The author and publisher are not responsible for any decisions made or actions taken based on the information provided in this article.

Recommended for you