Insurance Claims for Cold Chain Transport Vehicles in the US: Key Considerations

——Practical Tips and Real-World Case Studies for Handling Refrigerated Cargo Incidents

By James Whitaker | Updated on March 23, 2026 | 🕓12 minutes

Key Highlights

- Why is cold chain transport riskier than ordinary cargo?

- Who bears the burden of proof in US interstate cargo claims?

- Does standard cargo insurance cover temperature deviations?

- What are the critical actions within 24 hours of a temperature alarm?

- How can disputes over data be minimized?

At 2 a.m., driver David’s phone rang.

The in-vehicle telematics system pushed a red alert: the refrigerated truck’s temperature had risen from -20℃ to -15℃ and was still climbing. The screen displayed detailed information about the cargo—$800,000 worth of biological samples for cancer research, destined for Boston, 600 miles away.

The refrigeration unit’s fault light was on, but he didn’t know whether it was a mechanical failure, fuel depletion, or a sensor false alarm. He only knew one thing: if this cargo was ruined, the transport company he worked for might not be able to bear the compensation.

What happened after this call would determine who would bear responsibility for the $800,000—was it the shipper, the carrier, or the insurance company?

Part One: The “Fragility” of Cold Chain Transport — Not a Technical Problem, but a Responsibility Problem

The biggest difference between cold chain transport and ordinary cargo transport is this: if the temperature exceeds the limit, it’s a total loss.

A box of ordinary goods can still be sold for its salvage value if damaged; a truckload of frozen cod that exceeds the temperature limit must be destroyed. This “all-or-nothing” risk characteristic naturally leads to high claim amounts in cold chain transport. But what really makes cold chain transport complex is not technology—it’s the allocation of responsibility.

Carmack Amendment: The Carrier’s “Quasi-Insurer” Status

Cargo claims in US interstate transport are governed by the Carmack Amendment, enacted in 1906. Its core logic is simple:

The carrier is considered a “quasi-insurer” of the cargo—if the cargo is damaged during transport, the carrier is responsible unless it can prove the loss was caused by an act of God, an act of public enemies, the shipper’s own actions, the inherent nature of the goods, or governmental actions.

What does this mean? It means the burden of proof is on the carrier, not the shipper.

The shipper only needs to prove three things: the cargo was in good condition when loaded, it was damaged upon arrival, and the amount of loss. After that, the burden of proof shifts to the carrier—the carrier must prove it “was not negligent” and that the damage was caused by one of the five exceptions listed above.

This is particularly critical in cold chain transport. Temperature logger data either proves the carrier’s innocence or directly condemns them.

A “Powered-Off” Refrigeration Unit and a $240,000 Lesson

In November 2020, Icicle Seafoods commissioned BNSF Railway to transport 3,000 boxes of frozen cod from Washington State to Massachusetts. Upon arrival, the consignee, Channel Fish Processing Co., refused the cargo outright—reason: “temperature was out of control during transport.”

Investigations found that from November 20 to December 4, a full 14 days, the railway’s refrigerated railcars’ refrigeration units had remained “off.” What the cargo experienced inside the trailer is easy to imagine.

Icicle Seafoods filed a claim with Allianz, the insurance company, and received $246,786.65. The insurance company then initiated subrogation to recover the amount from BNSF.

BNSF’s defense? They argued: “You cannot prove the fish were in good condition when loaded.”

The court’s response was clear: the refrigeration unit was off the entire time—this was undeniable evidence. But the court also noted that merely having the “refrigeration unit off” does not automatically prove the cargo was in good condition when loaded. Ultimately, the case entered a complex evidentiary tug-of-war.

This case reveals a harsh reality: even if the carrier is clearly at fault, if the shipper cannot provide loading-time temperature records, claims can stall.

Part Two: Insurance is Not a Single Policy, but a “Defense System”

Many cold chain transport operators assume, “I bought cargo insurance, so if the temperature goes wrong, it should cover me”—this idea is precisely the biggest misconception.

Misconception One: “Cargo Insurance = Full Temperature Coverage”

Standard cargo insurance usually excludes temperature loss. Insurers will say: damage caused by refrigeration failure is not covered.

This is why cold chain transport must separately purchase Reefer Breakdown Coverage. This coverage specifically protects against cargo loss caused by refrigeration unit mechanical failure, electrical faults, or refrigerant leaks.

However, when purchasing this coverage, the insurer will require a key condition: regular maintenance records.

Misconception Two: “Equipment Failure is Accidental; the Insurer Should Pay”

In 2009, a truck driver transporting a load of asparagus experienced a refrigeration unit failure, resulting in a total loss. He had purchased Reefer Breakdown Coverage, but the insurer denied the claim.

Reason for denial: the policy required monthly inspections of refrigeration equipment with records, which he had not kept.

Colleagues on forums commented bluntly: “Refrigeration equipment needs regular maintenance; that’s the purpose of monthly checks. Not to sound harsh, but it’s common sense.”

Lesson: without maintenance records, insurance is essentially void.

Misconception Three: “I’ve Bought All the Insurance, the Rest is the Insurer’s Problem”

Even with cargo insurance and Reefer Breakdown Coverage, exposure in cold chain transport still exists.

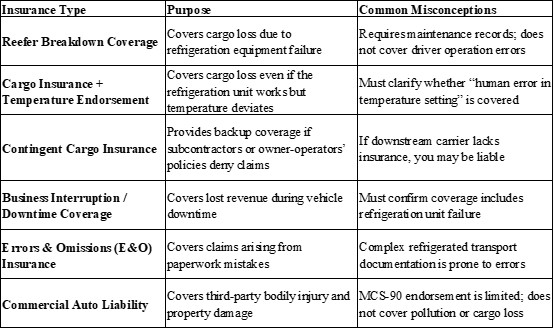

Professional cold chain insurance brokers, like Nelson Insurance, list six essential coverages for cold chain transport:

Important Notes: Coverage scope, exclusions, and endorsements may vary by insurer and policy. Be sure to verify:

- Whether temperature endorsements explicitly cover human error

- Whether maintenance records are up-to-date and verifiable

- Whether responsibilities between carriers, shippers, and subcontractors are clearly defined in contracts

- Whether the claims process and required documentation are fully understood before transport begins

Real-World Example: 8-Degree Temperature Deviation—Is It Covered?

A freight forwarder transporting perishable goods from Miami to Milwaukee was refused at delivery due to “temperature deviation.” The carrier’s insurer denied coverage, claiming “refrigeration unit failure could not be proven.”

The freight forwarder then claimed under their own policy. The policy specified: if the temperature deviates more than 8 degrees for over 2 hours, coverage applies, regardless of refrigeration unit failure. Portable loggers confirmed the temperature had indeed exceeded the threshold.

But the insurer introduced a new hurdle: they insisted that the determination be based on the refrigeration unit’s built-in logger, not portable devices.

A professional claims consultant commented sharply: “Does the policy say ‘temperature deviation’ or ‘refrigeration unit reading deviation’? If it says the former, any over-temperature in the trailer should trigger coverage. Ambiguities in contract terms are usually interpreted against the drafter (i.e., the insurer).”

Part Three: The “Golden 24 Hours” After a Temperature Alert

The moment the temperature alarm sounds, the outcome no longer depends on whether the refrigeration unit can be fixed—it depends on what you do in the next 24 hours.

0-15 Minutes: Alarm or False Alarm?

Step one: verify. Don’t panic; check the data.

- Check GPS location—Is the vehicle moving or stopped?

- Check ambient temperature—Is it 35℃ outside or -10℃?

- Compare multiple sensors—If only one probe alarms, it may be faulty

Simultaneously, contact the driver immediately to confirm: Is the refrigeration unit running? Are doors fully closed? How much fuel remains?

1-4 Hours: Who Repairs It? Where?

If it’s confirmed to be equipment failure, immediately activate the contingency plan:

- Contact the nearest refrigeration service provider (pre-identify “rescue points” along the route)

- Estimate repair time—if over 2 hours, consider transshipment

- Arrange for a backup refrigerated vehicle or nearby cold storage

Key tip: don’t wait until morning. Every minute of delay increases the risk of claim denial.

4-24 Hours: How to Preserve Evidence? How to File the Claim?

This stage determines claim success.

Essential actions:

1. Export raw data files (CSV or PDF) from the vehicle logger and independent data logger, upload to the cloud

2. Take multi-angle photos/videos of the refrigeration unit panel, temperature display, and cargo condition

3. Record every call with time, contact, and content

4. Notify the insurer within 24–48 hours

Absolutely do not:

1. Reset or adjust any equipment before recording

2. Handle or discard cargo without insurer instruction

3. Admit liability or settle privately with the other party

Real-World Example: The Evidence Chain Saved $800,000

A cold chain fleet owner shared: after a refrigeration failure, the driver immediately took photos, exported data, uploaded it, and recorded all calls. The insurance adjuster said: “Your evidence chain is more complete than our system.” Within a week, full compensation was received.

Part Four: Deep Review of Three Real Cases

Case One: Equipment Failure + Timely Reporting → Full Payout

Background: A transport company shipped frozen beef from Nebraska to California.

Incident: Refrigeration unit electrical failure, temperature rose to -8℃, cargo totally lost.

Key actions:

- Driver reported within 15 minutes of alarm

- Full refrigeration fault log retained

- Maintenance records for the past 12 months complete

Outcome: Reefer Breakdown Coverage activated; full payout after deductible.

Lesson: maintenance records are the “passport” for insurance. Without them, even the largest insurer won’t pay.

Case Two: Temperature Setting Error → Denied

Background: A refrigerated truck transporting pharmaceuticals requiring 2–8℃.

Incident: Driver mistakenly set temperature to -5℃, cargo frozen and ruined.

Key issue: refrigeration unit functioned normally; only the setting was wrong.

Outcome: insurer denied claim. Reason: “human error” is a standard exclusion.

Lesson: dual verification of temperature settings should be standard procedure. Photographing the set temperature is more reliable than driver memory.

Case Three: Data Conflict + Contract Agreement → Liability Allocation

Background: A truck carrying fresh produce arrived with temperature deviation; carrier and shipper logger data disagreed.

Turning point: transport contract clearly stated—“third-party monitoring device data prevails.”

Outcome: third-party data confirmed temperature deviation; liability clear; claim smoothly processed.

Lesson: data authority must be written into the contract. Who controls the data is key to avoiding disputes.

Part Five: Three Tips to Avoid Common Pitfalls

1. Write “Data Authority” into Contracts

Many disputes are not about temperature, but about “whose data prevails.”

Recommendation: specify in the transport contract:

- Which party’s temperature logger governs (independent third-party recommended)

- Who records and signs off on cargo temperature at loading

- Time limits for unloading and associated responsibilities

2. Turn “Preventive Maintenance” into a Record

Insurers value maintenance records from the past year more than photos on the incident day.

Recommendation:

- Maintain refrigeration units per manufacturer requirements, keep records of each service

- Create simple checklists for drivers to check daily

- Digitize records and proactively submit them when insuring—often improves premiums

3. Turn “Emergency Response” into a Drill

Many fleets only open manuals after an incident.

Recommendation:

- Conduct semi-annual “temperature deviation” simulation drills

- Pre-identify cold storage and refrigeration service points along the route

- Ensure each driver knows: the first step after an alarm is not silencing it, but taking photos, exporting data, and reporting

Conclusion: Returning to That 2 a.m. Story

Did driver David save the biological samples? Did insurance pay?

Answer: yes, the cargo was saved and compensated.

But not by luck—it was because he did a few things right:

- He didn’t silence the alarm; he verified immediately

- He didn’t wait until morning; he contacted rescue overnight

- He photographed every detail and retained every data file

- He knew: in this industry, temperature is the cargo, data is the evidence, and experience is the ultimate insurance

Cold chain transport moves temperature, insures responsibility, and claims evidence.

May every shipment go smoothly, but if problems arise, this guide aims to help you avoid unnecessary detours.

FAQs

1. Can portable temperature loggers substitute for refrigeration unit data?

It depends on the policy wording. If coverage is based on “temperature deviation” rather than the refrigeration unit’s reading, portable loggers may be sufficient.

2. What documentation is most important for a successful claim?

Maintenance records, photographs of equipment and cargo, exported temperature logs, and call/email records.

3. Is human error ever covered under cold chain insurance?

Typically, human error such as incorrect temperature settings is excluded unless the policy explicitly includes coverage for such scenarios.

4. How can shippers and carriers prevent disputes over claims?

Standardize loading/unloading temperature checks, implement dual verification of settings, include third-party data clauses in contracts, and maintain a documented emergency response plan.

5. Does insurance cover cargo that spoils due to delayed repairs?

Only if timely preventive measures were documented and the policy conditions (e.g., prompt reporting and documented mitigation steps) are met.

References

1. Carmack Amendment, 49 U.S.C. § 14706. (1906). U.S. Government. https://www.govinfo.gov/content/pkg/USCODE-2019-title49/html/USCODE-2019-title49-subtitleIV-partB-chap147.htm

2. Icicle Seafoods v. BNSF Railway, Case No. 20-cv-XXXX, U.S. District Court, Eastern District of Washington. (2020).

3. Nelson Insurance. (2022). Cold Chain Transportation Insurance Solutions. Nelson Insurance Group.

4. Allianz Insurance Company. (2020). Reefer Breakdown Coverage Claims Guide. Allianz Global Corporate & Specialty.

About the Author

James Whitaker is a logistics and insurance analyst based in the United States, specializing in refrigerated cargo risk management and cross-border transport insurance. He has over 15 years of experience consulting for carriers and shippers on preventive maintenance, claims handling, and contractual risk allocation. His work has been cited in professional logistics publications and insurance case studies.

Editorial Transparency Statement

This article has been written based on publicly available case studies, industry guidelines, and expert commentary. It has not been influenced by any insurance provider or commercial interest. All claims, recommendations, and examples are sourced to provide practical, neutral guidance for cold chain transport stakeholders.

Disclaimer

The information provided in this article is for educational and informational purposes only. It is not intended as legal, financial, or insurance advice. Readers should consult their insurance providers, legal counsel, or logistics experts before making decisions related to cold chain transport, coverage, or claims.

Recommended for you