Long-Haul Commercial Vehicle Insurance in Canada: Costs vs. Claims Processing Time

—— Analyzing Common Pitfalls and How to Avoid Them for Canadian Logistics Operations

By Michael Carter | Updated on March 31, 2026 | 🕓12–15 minutes

Key Highlights

- Why are commercial truck insurance premiums in Canada often higher than expected?

- What hidden clauses in policies can invalidate your coverage?

- How do cross-border operations impact insurance costs and risks?

- Why do claims take so long—and how can delays be reduced?

- What are the most common reasons for claim denials in real cases?

- How can logistics operators lower premiums without reducing coverage?

- What practical steps can improve claim approval speed and success rate?

At the end of 2023, I received an insurance policy file from Vancouver. The sender was my old friend Jason, who only left one sentence in the email: “Take a look and see if there’s anything wrong with this policy.”

It was a standard commercial vehicle comprehensive insurance policy, 47 pages thick. I spent one night carefully reading it and, at the end of the third addendum, found a line in small print:

"This policy does not cover any traffic accidents occurring east of Hope, British Columbia."

I took a screenshot and sent it to Jason. He was silent for ten minutes, then replied: “My truck goes east of Hope every week.”

This wasn’t the first time I had encountered such “hidden clauses” in policies. Over the past two years, in my capacity as an industry observer, I have systematically studied how long-haul commercial vehicle insurance works in Canada—not to sell insurance, but because too many friends have suffered losses in this field without understanding why.

I tracked seven real claim cases, interviewed five licensed insurance brokers, three insurance claims adjusters, and a dozen truck owners and drivers who had experienced major claims. This article is a summary of those observations.

Disclaimer: I am not an insurance professional and do not sell any insurance products. The cases in this article are based on real events, with some details obscured. This article does not constitute insurance advice; for specific matters, please consult a licensed professional.

Part One: Costs — Why Your Premium Is Always Higher Than Others

1.1 A Real Bill: New Immigrant Mr. Li’s First Year

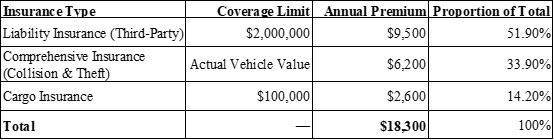

In the spring of 2023, a new immigrant Mr. Li from China bought a three-year-old Freightliner Cascadia in Vancouver for CAD 118,000. He planned to run short-haul trips from the Delta port to warehouses in Richmond.

He approached a Chinese-speaking insurance agent and received his first quote:

On the surface, it looked like a “standard” quote. But when I showed it to an underwriter with 12 years of experience, Mr. J, he pointed out three critical points that were overlooked:

Key Point 1: $2,000,000 third-party liability coverage is virtually useless for cross-border operations

“If Mr. Li only drives from Delta to Richmond, $2 million is sufficient. But if he takes a shipment to the U.S., this coverage is insufficient. An ordinary rear-end jury award in the U.S. averages $800,000 to $1.5 million. If serious injury is involved, it can easily exceed $2 million CAD. Many new immigrants are unaware of this until it’s too late.”

Key Point 2: Cargo insurance of $100,000 is calculated per “incident,” not per “truckload value”

“Mr. Li might transport a container of electronics worth $300,000, but the cargo insurance only covers $100,000. The remaining $200,000 is his responsibility. More importantly, cargo policies usually include a ‘co-insurance’ clause—if the cargo value exceeds the insured amount, the insurance company pays proportionally. For example, cargo valued at $300,000 with coverage of $100,000, in the event of total loss, the company only pays one-third. Many people never notice this when signing the contract.”

Key Point 3: The comprehensive deductible is set at $5,000 without clear disclosure

“The quote says ‘Comprehensive, deductible negotiable.’ The agent didn’t proactively mention the default was $5,000, and Mr. Li didn’t ask. This means losses under $5,000 are not covered at all. For a truck worth $118,000, small repairs—like replacing a bumper or a tail light—fall within this range and happen frequently.”

Three months after purchasing the insurance, Mr. Li had a minor accident: he reversed into a container door and his own tail light. Total repair costs were $6,000, but the insurer only paid $1,000 (due to the $5,000 deductible). The cargo insurance did not cover the container itself (considered “equipment,” requiring separate equipment insurance). When renewing the next year, his premium increased by 22%. His actual loss was far more than just the $6,000 repair.

1.2 The Pricing Formula Insurance Companies Won’t Tell You

To understand how premiums are calculated, I met with Mr. J—an underwriter with 12 years of experience at a large Canadian insurer. We talked for three hours in a coffee shop in Burnaby.

Q: What are the most critical factors in determining premiums?

“Claims history accounts for about 45%. But many misunderstand—it’s not just whether you’ve had accidents, but three sets of data: frequency, severity, and liability proportion. One $100,000 major accident impacts more than three $5,000 minor accidents. Major accidents imply systemic operational issues: fatigue driving, poor vehicle maintenance, improper route selection.”

“Also, even if the accident is not your fault, reporting it affects premiums. Statistics show that those ‘hit by others’ have higher-than-average risk of future accidents. It’s not discrimination, it’s big data.”

Q: Why are premiums higher for cross-border operations?

“Weight is about 35%. Annual mileage of 100,000 km vs 200,000 km doesn’t double the premium; it’s about 1.5 times because fatigue risk increases exponentially. For U.S. routes, we add 15%–30% regional surcharge depending on the state.”

“Why? Let me show you some data: In 2023, U.S. jury awards for truck accidents over $10 million increased by 27% YoY. California, Texas, and Florida are high-risk. An accident in California can cost five times more than in Ontario. This risk must be reflected in premiums.”

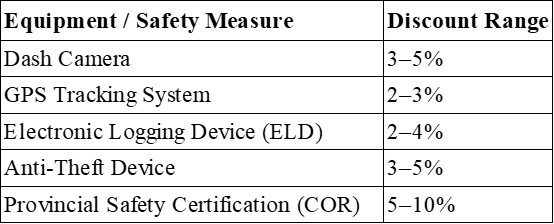

Q: What factors can reduce premiums?

“About 20%. Dashcams, electronic logs, GPS tracking, anti-theft devices, and provincial safety certifications (like COR) can all get discounts—but you must provide proof proactively. If you don’t say anything, they won’t ask or apply discounts.”

“I handled a case where a fleet had all safety equipment installed but didn’t report for three years. They overpaid $15,000 per year. Once I submitted the proof, premiums dropped 12%. The fleet owner yelled at his previous agent on the spot.”

Q: Do new immigrants or novice drivers always have high premiums?

“Not necessarily. We don’t discriminate, but we lack driving data. We check other indicators: employer, company safety record, vehicle age, installed safety equipment. Officially translated and notarized no-claims records from your home country can also help.”

“Honestly, new immigrants do pay higher premiums in the first three years—not discrimination, but statistics show higher accident rates initially. After three years of good records, premiums normalize.”

1.3 The “Hidden Tax” of Cross-Border Operations: A Fleet Owner’s Story

Mark (alias), operating a 15-truck fleet from Mississauga mainly on Toronto–Chicago routes, saw a 40% increase in insurance costs over three years.

“In 2019, premiums were about $12,000 per truck. In 2024, $17,500. Initially, I thought the insurer was unfair, but the real reason was the U.S.”

His 2023 claims report showed:

“One of our trucks rear-ended a pickup in suburban Chicago. Minor accident, the other driver was lightly injured. But they hired a lawyer specializing in truck accidents, suing us for ‘negligent driving,’ ‘poor maintenance,’ and ‘fatigue driving.’”

“The case lasted 14 months. We settled: $380,000 total; insurer paid $300,000, we paid $80,000 deductible. After this, the cross-border surcharge went from 15% to 35%.”

Mark now requires extra training for all U.S.-bound drivers:

- Differences in U.S. state traffic regulations

- How to handle “accident lawyers”

- How to preserve evidence at the scene to avoid legal pitfalls

“I now spend $15,000 annually on safety training, but it’s a small price compared to rising insurance costs.”

Part Two: Claims Processing — You Are Waiting for More Than Money

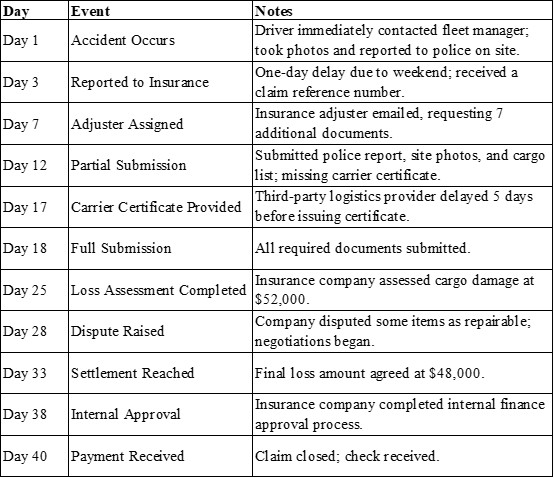

2.1 Real Timeline of a Claim: Hongda Logistics’ 40-Day Nightmare

In March 2024, I tracked a cargo damage claim for a small Vancouver logistics company, pseudonymously called Hongda Logistics.

A trailer on BC Highway 5 was rear-ended, partially damaging electronics worth CAD 80,000. Liability was clear—the other party was at fault. The policy was comprehensive, so Hongda had to claim with its own insurer first, which then subrogated the other party.

Timeline:

Over 40 days, actual losses exceeded $48,000 cargo value:

- Warehousing fees: $1,800

- Trailer and temporary parking: $1,200

- Replacement vehicle rental (40 days): $9,600

- Lost future client contracts due to delays: ~$30,000

- Manager spent 60+ hours handling the claim: ~$5,000 management cost

Total hidden loss: ~$47,600 (excluding cargo loss)

Hongda’s owner said:

“If the claim had been resolved in 20 days, we could have kept the client. 40 days, everything’s gone. Insurance claims speed isn’t just about money—it’s survival.”

2.2 Claims Adjuster Confession: Why Your Case Is Always Delayed

I spoke with Ms. S, a claims adjuster with 8 years handling commercial vehicle claims. Each year, she processes over 200 cases.

Reporting stage (Days 1–7):

“Many owners think reporting is enough. But we need to verify policy validity, coverage, and whether an on-site investigation is needed. If documentation is incomplete, we email for supplements. Two-way communication can take 2–3 days.”

“Worst case: the owner claims ‘all documents are ready,’ but there are only three photos, no license plates, no close-ups of cargo damage. We must request more info, which looks like dragging time, but it’s owner-prepared.”

Investigation & Liability (Days 7–28):

“If third-party injury or unclear liability is involved, or a criminal investigation (e.g., DUI), this stage can be very long. I’ve seen police reports take six weeks. Remote areas add delays; BC and northern ON might require hundreds of km travel for adjusters.”

Damage Assessment (Days 18–33):

“This is the most disputed step. Owners want replacement, we suggest repair. For third-party assessors, scheduling takes time. I handled a $200,000 electronics claim; our expert saw 70% repairable. Took two months to agree.”

Tips to Accelerate Claims:

1. Submit all documentation at once, especially carrier-issued damage certificates.

2. Follow up proactively but not daily—every three days is ideal.

3. Use an experienced insurance broker to intervene at critical points.

2.3 A “Lightning Fast Claim” Case

Summer 2024, Alberta fleet received a payout within 11 days after cargo damage.

“Golden 24 Hours” Process (by Operations Manager, Mr. T):

- 0–2 hours: Driver photographs accident (≥3 angles), uploads to cloud with GPS & timestamp, emergency call within 15 mins.

- 2–12 hours: Carrier issues damage certificate in 4 hours, vehicle to pre-approved shop.

- 12–24 hours: All materials submitted via broker; insurer assigns adjuster within 24 hours, preliminary assessment within 48 hours.

- Days 3–11: Adjuster completes damage assessment in 3 days; finance issues payment in 5 days; check arrives by Day 11.

Key Takeaways:

- Standardized procedures with manuals; drivers follow steps without thinking.

- Maintain good carrier relationships; cooperation is critical.

- Choose an effective insurance broker; proactive intervention speeds process.

Part Three: Traps — Seven Real Cases I Have Witnessed

Case 1: Private Auto Used for Business (Mr. Zhang’s SUV)

- Employee uses private SUV for company deliveries.

- Collision occurs; investigation reveals car used for commercial purposes.

- Private insurance denies coverage; owner pays $12,500; insurance canceled.

Solution: Use commercial insurance for all vehicles or Hired & Non-Owned Auto (HNOA) rider ($1,500–$3,000/year for CAD 1–2 million liability).

Case 2: Cargo Insurance “Word Games” (Mr. Wang’s Valves)

- Imported industrial valves (CAD 120,000) damaged during unloading.

- FOB terms: buyer assumes risk after loading; seller’s basic marine insurance doesn’t cover unloading.

- Loss: CAD 38,000 borne by buyer.

Solution: High-value cargo should purchase All Risks insurance; clarify exclusions; verify policy coverage.

Case 3: “Ghost Drivers” on Fleet Policy (Mr. G, 8-truck fleet)

- Temporary drivers not listed on authorized drivers.

- Accident occurs; insurer denies third-party liability.

- Owner pays $47,000; policy canceled; new policy 35% higher.

Solution: Maintain driver list; update within 3 days; verify MVR; consider flexible fleet insurance.

Case 4: EV Insurance Blind Spot (Vancouver Green Logistics)

- Two electric trucks; insurer first refuses coverage, then quotes 60% higher than diesel; third agrees with 30% battery deductible.

- High battery replacement costs; insufficient repair network.

Solution: Confirm insurer coverage, request manufacturer maintenance data, purchase EV-specific riders.

Case 5: Leased Driver Liability Hole (Richmond Fleet)

- Drivers bring own vehicles; company lacks HNOA coverage.

- Accident injures pedestrian; legal liability extends to fleet.

- Fleet uses CAD 200,000 commercial liability plus CAD 50,000 legal fees.

Solution: Require driver insurance verification; purchase HNOA rider; add fleet as Additional Insured.

Case 6: Safety Tech Discount Blind Spot (Ottawa Cold Chain Fleet)

- Fleet equipped with dashcams and GPS; previous broker didn’t ask, discount unclaimed.

- New broker applies 8% discount, saving $4,200/year.

Solution: Proactively submit safety equipment list before renewal.

Part Four: Strategies — Smart Practices I’ve Seen

4.1 Using “Safety Score” to Lower Premiums (London, ON)

- 12-truck fleet submits annual safety report with:

Zero-accident years highlighted

Quarterly safety training records

Vehicle maintenance records

Random dashcam reviews

Result: Renewal increases 40% lower than industry average.

4.2 Using “Annual Insurance Bidding” to Lower Premiums (Toronto, 20-truck fleet)

- Invite 5 insurers for quotes every three years

- Submit 3 years of safety and claims history

- Require breakdown of discounts and claims service commitments

- First bid reduced rate by 12%, revealing previous “loyalty tax”

Preparation Steps:

1. Begin preparation three months in advance, organize safety records and claims history from the past three years.

2. Contact 5–6 insurance companies through the broker and issue the tender.

3. After receiving quotes, compare not only the premium but also discount items and claims service commitments.

4. Choose the insurer that provides the most comprehensive value, not necessarily the lowest price.

Appendix: Quick Self-Check Checklist

If you are operating or planning to enter the long-haul logistics industry, it is recommended to use this checklist every six months for an “insurance health check”:

Policy Basics

〇 All vehicles used for commercial transport are listed on the commercial policy

〇 Coverage for cross-border operations is no less than CAD 5,000,000

〇 Cargo insurance coverage meets at least 120% of the highest single shipment value

〇 HNOA endorsement purchased (if using non-owned vehicles)

Driver Management

〇 All drivers are listed on the policy’s authorized driver roster

〇 New drivers are added to the policy within 3 days of joining

〇 Leased drivers provide proof of personal commercial insurance and list the fleet as an additional insured

Safety & Discounts

〇 All installed safety equipment (dashcams, GPS, ELD, anti-theft devices) has been reported to the insurer

〇 Provincial safety certifications (e.g., COR) have been reported to the insurer

〇 Conduct an insurance tender every 3 years, comparing at least 3 insurers

Claims Preparedness

〇 Established a 24-hour post-incident response procedure

〇 All drivers are aware of the requirements to “take photos on site, obtain carrier proof, and report to the insurer within 24 hours”

〇 Maintain a claims tracking sheet recording the time, contact person, and commitment milestones for each communication

FAQs

1. What is the minimum recommended liability coverage for cross-border trucking?

While CAD 2 million may be sufficient for local operations, cross-border trucking—especially into the United States—often requires at least CAD 5 million or higher due to significantly larger liability awards.

2. Does cargo insurance automatically cover the full value of goods?

No. Many cargo policies are based on “per occurrence” limits and may include co-insurance clauses. If underinsured, payouts may be reduced proportionally.

3. Why can claims take more than 30 days even when liability is clear?

Delays often occur due to incomplete documentation, third-party involvement, damage assessment disputes, or waiting for official reports (e.g., police findings).

4. How often should I review or rebid my insurance policy?

It is recommended to conduct a full review annually and a competitive bidding process every 2–3 years.

5. What is HNOA insurance and when is it necessary?

Hired and Non-Owned Auto (HNOA) insurance covers liability when using vehicles not owned by the company, such as employee-owned or leased vehicles.

References

1. Insurance Bureau of Canada. (2023). Commercial vehicle insurance in Canada: Industry overview and risk trends. [https://www.ibc.ca]

2. Canadian Trucking Alliance. (2024). Safety, compliance, and risk management in trucking operations. [https://www.truckingalliance.ca]

3. Transport Canada. (2022). Commercial vehicle safety and cross-border transportation statistics. [https://tc.canada.ca]

4. Federal Motor Carrier Safety Administration. (2023). Large truck crash causation study and safety data. [https://www.fmcsa.dot.gov]

5. National Safety Council. (2024). Injury facts: Motor vehicle crash trends and costs. [https://www.nsc.org]

About the Author

Michael Carter has worked in the Canadian logistics industry for many years and is now an independent writer focusing on risk management and operational efficiency in the North American transportation sector.

He specializes in analyzing risk management, insurance structures, and operational efficiency in North American freight and logistics systems. His work is based on real-world case studies, industry interviews, and first-hand operational insights rather than theoretical models.

Editorial Transparency Statement

This article is based on a combination of real-world case observations, interviews with licensed insurance brokers and claims adjusters, and analysis of industry practices in Canada’s commercial transportation sector.

All case studies referenced are derived from actual events, with identifying details modified to protect privacy. The purpose of this content is educational—to help logistics operators better understand insurance costs, risks, and claims processes.

No insurance products are sold or promoted in this article, and no compensation has been received from insurance providers or related entities.

Disclaimer

This article is for informational purposes only and does not constitute legal, financial, or insurance advice.

Insurance policies vary significantly by provider, jurisdiction, and individual circumstances. Readers should consult licensed insurance professionals, legal advisors, or relevant regulatory authorities before making any decisions related to coverage, claims, or risk management.

Recommended for you