Are There Significant Differences in Insurance Claims Standards Between Canadian and US Cross-Province Road Trips?

——Understanding the Key Variations in Claims Process and Coverage for Driving Across Provinces in Canada and the US

By Jonathan Parker | Updated on March 24, 2026 | 🕓18 minutes

Key Highlights

- Differences in Canadian provinces’ insurance systems and claims processes

- Key variations across U.S. states: fault vs. no-fault, coverage limits, medical payouts

- Cross-border (Canada–U.S.) claims: system switches, OPCF 44R, and medical cost considerations

- Practical pre-trip and post-accident recommendations

- Common pitfalls and FAQs for North American road travelers

From Vancouver to Toronto, from California to New York, and even across the border—does your car insurance really cover you?

Cross-border road trips are a dream for many travelers. Starting from Vancouver, you can drive south along Highway 5 and reach Seattle in just three hours; from Toronto, crossing the Rainbow Bridge brings you to Niagara Falls, New York. The nearly 9,000-kilometer border between Canada and the US makes cross-border driving a common experience for residents of both countries.

But when an accident happens, this romance can be shattered by a complex claims process.

“My Ontario policy was involved in an accident in BC—who should I claim through?”

“I bought the minimum coverage in California; is it enough in Nevada?”

“If a Canadian driver gets into an accident in the US, who pays the medical bills?”

These questions reveal a core confusion: are there significant differences in insurance claims standards for cross-province or cross-state road trips between Canada and the US?

The answer is: yes—and the differences are bigger than you might imagine.

However, the root cause of the difference is not the “border” but the “system.” The reason why claims standards vary between Canadian provinces, US states, and even between Canada and the US lies in:

- Canada: Provincial governments regulate insurance, resulting in large systemic differences—some provinces have government-run insurance monopolies, while others have competing private insurers.

- US: Similarly, each state regulates its own insurance, but 50 states mean 50 sets of rules, varying from liability determination to minimum coverage.

This means that “cross-province” or “cross-border” itself is not the problem; the real issue is “which system you are entering.”

1. Canada cross-province driving: entering a public insurance province from a private insurance province changes your claims window, rules, and even the significance of liability determination.

2. US cross-state driving: rules may appear uniform, but differences in coverage limits, fault/no-fault systems, and medical payment structures hide pitfalls.

3. Canada-US cross-border driving: legal recognition is high, but systemic differences in healthcare, litigation culture, and timelines present the real challenges.

When an accident happens, what should you do?

I. Canada Cross-Province Driving: System Switching Is the Biggest Challenge

Many people assume that car insurance rules are similar across Canadian provinces, but the truth is the opposite—when driving across provinces, you may enter a completely different insurance world. In Canada, car insurance is not “nationally unified” but regulated by each province, and the differences are far greater than most people imagine.

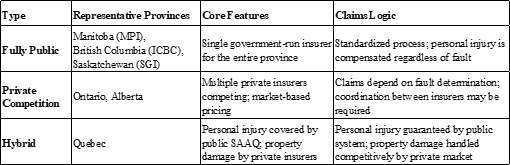

1.1 System Overview: Three Models, Three Experiences

Canada’s provincial car insurance systems mainly fall into three categories:

For example, Manitoba implements a fully public No-Fault system. All basic car insurance is provided by the Manitoba Public Insurance (MPI), and the claims logic is straightforward: personal injury compensation is guaranteed regardless of fault, without the need for litigation. The advantage of this model is certainty—you don’t need to worry about the other party’s insurer delaying payment, nor do you need a lawyer.

A car owner who moved from Ontario to Manitoba shared on Reddit:

“In Ontario, just comparing insurance companies took hours—the cheaper one was slow to settle, the faster one was expensive. In Manitoba, suddenly there’s only one insurer. Choice is limited, but it’s really convenient. Plus, premiums are much cheaper.”

In contrast, Ontario represents private insurance. It follows a fault-based system but provides mandatory Accident Benefits—medical and income loss compensation is paid upfront regardless of fault. This “hybrid model” is common among Canada’s private insurance provinces: no-fault personal injury coverage is combined with a fault-based property damage recovery mechanism.

1.2 Claims Process Details: Reporting Windows Determine Experience

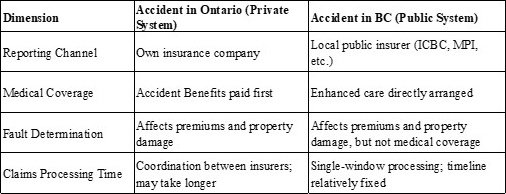

Case 1: Ontario resident has an accident in BC

Suppose you drive from Toronto to Vancouver along Highway 97 and get rear-ended. Your Ontario policy is with a private insurer with a $1 million coverage limit. The claims process would be as follows:

Step 1: On-site handling

- Report to police (BC requires reporting if damage exceeds CAD 1,000)

- Exchange information: driver’s license, insurance, license plate

- Take photos: wide shots, vehicle damage, injuries

- Look for witnesses

Step 2: Claim filing

- In BC, you must file through ICBC (BC’s government insurer), not your Ontario insurer

- Follow ICBC instructions via the Dial-a-Claim hotline (1-800-910-4222)

- Vehicle assessment is done through ICBC’s designated repair channels; you submit vehicle info and photos for remote review

Step 3: Medical compensation

- BC’s Enhanced Care system allows ICBC to directly arrange medical and rehabilitation services

- Even if you are at fault, ICBC pays for medical expenses, rehab, and income loss upfront

- Liability determination does not delay personal injury payment

Step 4: Vehicle damage

- ICBC determines fault based on investigation

- If the other party is fully at fault, ICBC pays for your repairs first and then recovers from your Ontario insurer

- If you are fully or partially at fault, ICBC coordinates with your Ontario insurer to allocate costs according to BC rules

Key differences summarized:

1.3 Medical Compensation Mechanism: Accident Benefits Are Key

Canadian provinces have Accident Benefits, the biggest advantage of the Canadian system. In Ontario, coverage includes:

- Medical and rehabilitation expenses: up to CAD 65,000 (non-catastrophic) or CAD 1,000,000 (catastrophic)

- Caregiver expenses: up to CAD 36,000 (non-catastrophic) or CAD 1,000,000 (catastrophic)

- Income replacement: up to CAD 400 per week (70% of pre-tax income)

- Housekeeping services: up to CAD 250 per week

Crucially, Accident Benefits do not depend on fault. Even if you are fully at fault, these benefits are available.

Case 2: Ontario resident has an accident in Nunavut

A real appellate court case involved an Ontario resident seriously injured in Nunavut. She drove a government-plated vehicle insured by Travelers, but also had a personal Ontario-plated car insured by CAA.

Question: Which insurance provides Accident Benefits?

Ontario’s benefits are more generous than Nunavut’s. The court ruled that she could choose Ontario benefits under the CAA policy, since the policy covered North America and Ontario had the closest connection to the case (residence, vehicle registration).

Key takeaways:

1. Your Canadian policy usually covers all of North America—you don’t need extra insurance

2. Amount payable depends on policy terms—benefits vary by insurer and province

3. If you have multiple vehicles/policies, you may choose the more generous benefit—a lesser-known rights strategy

1.4 Special Issues in Public Insurance Provinces

Entering a public insurance province brings special rules:

Manitoba (MPI):

- Out-of-province vehicles must claim through MPI

- MPI pays first, then recovers from your out-of-province insurer

- If MPI finds you at fault, your record may affect future premiums in Manitoba

Quebec (SAAQ):

- Personal injury covered by SAAQ, property damage by private insurance

- Out-of-province drivers get SAAQ coverage for injuries but property damage is handled by their own insurer

- Coverage is broad—drivers, passengers, pedestrians, and cyclists

1.5 Risk Summary

Key risks for Canada cross-province driving:

1. Claims window switching:

- Moving from private to public province requires reporting to the public insurer

- Unawareness may delay claims or be considered “failure to report”

2. Medical benefits differences:

- Each province has different coverage limits

- Ontario has a higher threshold for catastrophic injury and more generous benefits

3. Inconsistent impact of liability determination:

- No-Fault provinces (BC, MB) don’t tie injury compensation to fault

- Fault provinces (ON, AB) do affect compensation for non-Accident Benefits

4. Premium record risk:

- Being at fault in a public province can increase future premiums

II. US Cross-State Driving: Appears Unified but Hides Pitfalls

US car insurance seems more uniform—private insurers, state regulation—but legal differences between states can surprise you. Each of the 50 states has its own rules: liability systems, minimum coverage, medical payment structures, and statutes of limitations.

2.1 System Overview: 50 States, 50 Rules

The US has no federal car insurance standard. Each state sets:

- Minimum liability coverage: California $15,000/person, Alaska $50,000/person

- Fault system: Fault vs No-Fault

- Medical payment rules: PIP, MedPay, or pure liability

- Statutes of limitations: 1–6 years depending on state

Key protection for out-of-state driving: Out-of-State Coverage Clause

- Your policy automatically meets the minimum coverage of the state you enter

- Example: California minimum $15k; driving in Nevada (minimum $25k) → coverage adjusts to $25k

- Caveat: “minimum coverage” may still be insufficient for serious accidents

2.2 Fault vs No-Fault

Fault States (Tort States):

- Examples: CA, NV, TX, FL (partial)

- Claim from at-fault party

- High litigation, lawyers involved, longer claims, high compensation potential

No-Fault States:

- Examples: NY, FL, MI, NJ

- PIP pays medical expenses regardless of fault

- Faster claims, limited litigation, PIP coverage often low

Key difference: crossing from fault to no-fault state requires adjusting to a different claims logic.

Case 3: NJ resident in NY accident

- NJ policy, accident in NY

- Insurer denied claim, citing NY’s no-fault arbitration

- NY court applied “center of gravity” principle: NJ resident, NJ registered vehicle, NJ insurer → NJ law applies

2.3 Deemer Statutes

No-Fault states have Deemer Statutes:

- Example: NJ Deemer Statute gives maximum $250k PIP if your insurer is licensed in NJ, even if policy issued in CA

- Pitfall: if you opted out of PIP, Deemer protection may not apply

2.4 Medical and Payment Differences: PIP, MedPay, Liability

- PIP: No-fault states, covers medical, income loss, caregiver; limits vary (FL minimum $10k)

- MedPay: optional in fault states, low coverage, only medical

- Liability: covers victim, requires fault determination

Key: No-fault states → PIP pays first; fault states → must establish liability first

Case 4: CA driver in NV accident

- CA minimum $15k, NV minimum $25k, other party at fault

- NV fault, medical bills exceed $25k

- If UIM coverage included → claim difference from own insurer

- Otherwise → pay excess out-of-pocket or sue

2.5 Statute of Limitations Pitfall

- TN/KY: 1 year

- CA/NV: 2 years

- NY: 3 years

- FL: 4 years

- ME: 6 years

Risk: misunderstanding deadlines may lose claims rights

2.6 Risk Summary

US cross-state driving risks:

1. Minimum coverage differences → may be insufficient

2. Liability system switching → affects claims and upfront medical payments

3. Uncontrollable medical costs → PIP often insufficient

4. Litigation risk → high lawyer involvement even if not at fault

5. Statute pitfalls → varies by accident location

III. Canada-US Cross-Border Driving: System Switching Is the True Test

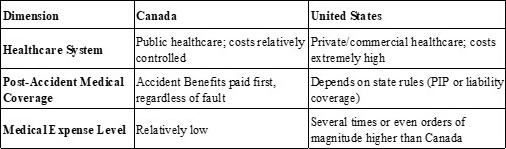

Cross-border may seem complex, but legally policies usually recognize each other. Real complexity is execution: healthcare, legal, and insurance systems differ.

3.1 Coverage: Usually No Extra Insurance Needed

- Canadian policies cover the US; US policies cover Canada

- Confirm with insurer whether proof (e.g., Canada Non-Resident Card) is required

3.2 Core Principle: Follow Accident Location Rules

- Accident in US → follow US state law

- Accident in Canada → follow Canadian provincial law

Coverage rules depend entirely on location despite North American-wide policy coverage.

3.3 Medical Compensation Differences: System Switching Core Issue

Case 5: Canadian driver injured in US

- Insurance only covers part of US hospital costs

- Some procedures deemed “over-treatment” in Canada

- Expert testimony and cost comparisons needed for full recovery

Case 6: US driver injured in Quebec

- SAAQ provides emergency medical care to all accident victims

- Property damage handled by US insurer

3.4 OPCF 44R: Key Protection for Canadians in US

- Covers gaps if US party underinsured

- Example: Ontario policy $1M, Florida accident, other party at fault, PIP $10k → OPCF 44R claims remaining $90k

- Requirements: gap coverage (not uninsured), litigation still needed, venue flexible, statute of limitations by accident location

3.5 Cross-Border Statute Pitfalls

US state statutes of limitation apply even for Canadian OPCF 44R claims → must act quickly

3.6 Collision Coverage Risk

- Ontario DCPD: covers non-fault damage even without collision coverage

- US states generally lack DCPD

- If accident in US and you lack collision coverage → out-of-pocket first, lengthy recovery from at-fault party

Tip: Confirm collision coverage before cross-border trip

IV. Practical Tips and Avoiding Pitfalls

4.1 Before Departure

1. Confirm policy coverage → call insurer, verify US/Canada coverage, documents, collision coverage

2. Include OPCF 44R (for Canadians) → protects against underinsured US drivers

3. Increase coverage → recommended minimum $1M liability

4. Learn destination rules → US fault/no-fault, Canadian public/private system, local statutes

5. Print policy and insurance card → keep handy, note 24-hour claims hotline

4.2 Immediately After Accident

1. Call police → required in most states/provinces, retain report number

2. Take photos → scene, damage, injuries, road conditions

3. Record info → names, contacts, insurer, license plates, witnesses

4. Don’t admit fault → until insurer contacted, sign nothing, accept no money

5. Seek medical attention → even minor injuries, keep receipts and records

4.3 Medical Handling

- Canadian drivers in US: seek care, record costs, contact Canadian insurer, maintain documentation, consider returning for long-term treatment

- US drivers in Canada: emergency care provided, contact provincial insurer (ICBC, SAAQ), do not sign anything until insurer contacted

FAQ

Q1: Is my Canadian policy valid in the US?

A: Most cover the US; confirm with insurer and whether a Non-Resident Card is needed

Q2: Who pays medical costs in the US?

A: No-fault states → PIP pays first; fault states → other party liability; Canadians can claim Accident Benefits simultaneously

Q3: Ontario policy, accident in BC → who to claim through?

A: Through ICBC; ICBC coordinates with Ontario insurer; Enhanced Care covers medical

Q4: US states with low coverage → what to do?

A: Ensure OPCF 44R included to claim difference up to your limit

Q5: Need extra cross-border insurance?

A: Usually not, but confirm collision coverage

Q6: Can I sue in no-fault state?

A: Yes, if injury exceeds threshold; otherwise rely on PIP

Q7: Canadian Accident Benefits valid in US?

A: Generally yes, but payout depends on policy and “Canadian usual medical standards”

Disclaimer: Information is for reference only and does not constitute legal or insurance advice. Consult your policy and professional counsel for specifics.

References

1. Insurance Bureau of Canada. (2022). Automobile insurance in Canada: Understanding interprovincial coverage. Retrieved from [https://www.ibc.ca]

2. ICBC. (2023). Enhanced Care & claims process for out-of-province drivers. Vancouver, BC: Insurance Corporation of British Columbia.

3. New Jersey Department of Banking and Insurance. (2021). Deemer Statute and auto insurance coverage. Trenton, NJ.

4. Travelers Insurance. (2022). Canada Non-Resident coverage and accident benefits. Retrieved from [https://www.travelers.com]

5. SAAQ. (2023). Québec procedures for out-of-province and foreign drivers. Québec City, QC: Société de l’assurance automobile du Québec.

6. U.S. Department of Transportation. (2022). State motor vehicle insurance regulations and minimum coverage requirements. Washington, DC.

7. American Association of Motor Vehicle Administrators (AAMVA). (2022). Cross-border and out-of-state auto insurance considerations. Alexandria, VA.

About the Author

Jonathan Parker is a North American insurance and legal consultant with over 12 years of experience in auto insurance and cross-border claims management. Jonathan has advised private clients, legal firms, and travel agencies on cross-province and international driving insurance, specializing in practical solutions for Canadian and U.S. road travelers.

Editorial Transparency Statement

This article was prepared using publicly available information, legal case studies, and official insurance guidelines from Canadian provinces and U.S. states. All sources are traceable and cited above. While the author is a professional in the insurance industry, the content is intended for general informational purposes only and should not be considered formal legal or insurance advice. Readers are encouraged to consult their own insurance providers and legal professionals for guidance specific to their circumstances.

Disclaimer

The information in this article should not be considered professional insurance, legal, or financial advice. Insurance coverage, exclusions, and eligibility vary widely depending on the provider, jurisdiction, and individual circumstances.

Recommended for you