How to Choose the Most Cost-Effective Add-Ons for Cross-Province Driving Insurance in Canada?

——Understanding the Average Claims Processing Time for Accidents During a Canadian Cross-Province Road Trip

By Jonathan Parker | Updated on March 24, 2026 | 🕓12–15 minutes

Key Highlights

- Insurance coverage varies by province.

- Collision and comprehensive are essential.

- Rental and roadside assistance save money.

- Claims can be slow without proper evidence.

- Choose protection, not just low price.

Why You Need to Pay Attention to Add-Ons

Canada is vast, and cross-province road trips are a top choice for many families and travel enthusiasts. However, when driving across different provinces, your basic auto insurance may not cover all risks.

Automobile insurance regulations vary significantly across provinces in Canada. Ontario requires insurers to provide up to $2 million in medical and rehabilitation coverage, while Alberta’s basic coverage is relatively limited. When an accident occurs outside your familiar province, the claims process, liability determination, and even the coverage amounts available may differ greatly from your expectations.

A 2025 survey showed that 81% of Canadian drivers were satisfied with claims services, an 8-percentage-point increase from 2023. This indicates that the insurance industry is actively improving service quality—but the prerequisite is that you choose the right insurance products.

Core Concepts of Canadian Auto Insurance

Basic Insurance vs Add-Ons

In Canada, every province and territory mandates that drivers purchase certain basic insurance. Mandatory coverage typically includes:

Third-Party Liability: Covers damages or injuries caused to others due to your fault

Accident Benefits: Provides medical, rehabilitation, and income replacement benefits for you and passengers, regardless of fault

Direct Compensation for Property Damage (DCPD): In some provinces, if the other party is fully at fault, your insurer directly compensates for your vehicle damage

However, the scope and limits of mandatory coverage vary by province. For example, Ontario mandates accident benefits far higher than Alberta. This highlights the importance of add-ons—they fill gaps left by mandatory insurance, giving you more comprehensive protection when driving across provinces.

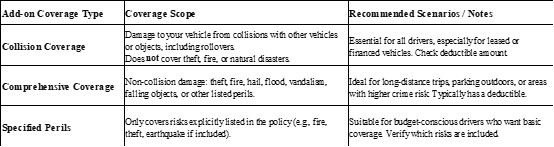

Core Add-On Types Explained

According to the Insurance Bureau of Canada, the following are common add-ons and their coverage:

Overview of Cross-Province Claims Process

The standard claims process includes:

Accident Occurs → On-Site Evidence Collection → Report Notification → Damage Assessment → Liability Determination → Claims Payment

Key Time Points:

Reporting Deadline: Most insurers require notification within 7 days of the accident

Evidence Collection: The first hour at the accident scene is crucial for collecting evidence

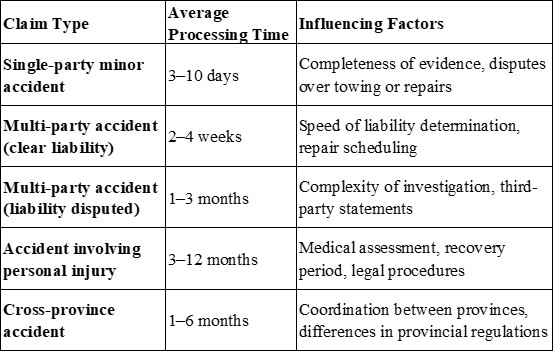

Claims Duration: Simple cases take days to weeks; complex cases may last several months

Core Section: Add-On Cost-Effectiveness Evaluation Framework

Based on the latest 2026 market data and industry trends

Which Add-Ons Are “Must-Have” for Cross-Province Driving?

[Essential]

1. Collision + Comprehensive Insurance Combo

This is the basic coverage for cross-province trips. Collision insurance covers possible collision accidents, while comprehensive insurance addresses non-collision risks such as weather and theft. For new or financed vehicles, this is usually required by the lender.

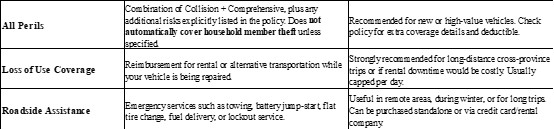

2. Rental/Replacement Vehicle Coverage

This add-on is often undervalued in cross-province driving. If your vehicle needs repair in another province without rental coverage:

You may pay $50–$100 CAD per day for a rental

Or be forced to pause your trip while waiting for repairs

Or have to continue your trip and handle claims afterward

Considering repair cycles can last 5–15 days, the return on investment for rental coverage is very high.

[Highly Recommended]

3. Roadside Assistance

In Canada’s remote areas (e.g., northern highways, Rocky Mountain routes), a long-distance tow can cost hundreds or even over a thousand CAD. Annual fees for roadside assistance are usually $50–$100, making it highly cost-effective.

[Optional Based on Itinerary]

4. Personal Accident Insurance (PAI)

If your employer or credit card already provides sufficient personal accident coverage, this can be skipped. However, for self-employed individuals or travelers without employer coverage, it is recommended.

5. Glass/Tire Insurance

For winter trips or routes with many gravel roads, the value of this add-on increases significantly.

Evidence Section: Average Claims Duration and Real Case Analysis

According to the 2026 Rates.ca Auto Insurance Research Report, Canadian auto insurance claims satisfaction has rebounded to 81%, up 8 percentage points from 2023. This improvement is mainly due to insurers optimizing the claims process and applying new technologies.

Case 1: BC Resident, Ontario Accident Claim (37 Days)

William, a BC resident, drove his own car from Vancouver to Toronto to visit relatives. He was rear-ended on Ontario’s Highway 401, with severe rear-end damage; the other party was fully at fault.

Insurance Portfolio:

BC basic insurance (ICBC)

Add-ons: Collision, Comprehensive, Rental

Not purchased: Roadside Assistance

Claims Process:

Day 1: Reported the accident, took photos, contacted ICBC

Day 3: ICBC designated an Ontario repair shop for damage assessment

Day 7: Liability determined (other party fully at fault)

Day 12: Damage amount confirmed; repair shop indicated a 2-week wait for parts

Days 15–28: Rental coverage used for a replacement vehicle

Day 37: Vehicle repaired, claim closed

Total Claims Duration: 37 days

Rental Coverage Paid: $1,260 (21 days × $60/day)

Key Takeaway: Rental coverage played a critical role, preventing thousands in extra expenses.

Case 2: Alberta–Ontario Rear-End Accident (Liability Determination Took 4 Weeks)

Olivia drove from Calgary to Toronto and was rear-ended by an Ontario-plated vehicle. The accident itself was simple, but liability determination was prolonged due to cross-province coordination.

Insurance Portfolio:

Alberta basic insurance

Add-ons: Collision, Rental

Not purchased: Roadside Assistance

Claims Process:

Week 1: Reported accident; Alberta insurer required direct communication with Ontario insurer

Week 2: Ontario insurer started investigation, awaited police report

Week 3: Insurers negotiated liability percentages

Week 4: Liability determined (other party fully at fault), damage assessment began

Week 6: Vehicle repaired

Total Claims Duration: 6 weeks

Liability Determination: 4 weeks

In cross-province accidents, liability determination is the main time-consuming factor. The completeness of evidence directly affects efficiency.

Case 3: AI-Accelerated Claims (48 Hours)

Liam, a Montreal resident, had his vehicle damaged by a roadside advertising board.

Insurance Portfolio:

Desjardins Insurance

Add-ons: Comprehensive

Claims Process:

Liam uploaded accident photos via Desjardins’ Omni App

AI image recognition analyzed damage automatically

Claim paid within 48 hours, entirely without human adjusters

Total Claims Duration: 48 hours

Choosing insurers with digital claims capabilities can greatly shorten claims time. Desjardins currently automates 92% of simple auto claims.

In-Depth Analysis: Provincial Claims Differences

In Canada, auto insurance systems vary by province, which also affects cross-province claim efficiency.

British Columbia (BC): Public insurance model; ICBC offers standardized rates. Claims are relatively standardized, but cross-province coordination may require extra time.

Alberta: Private insurance market, competitive; plans to switch to a “care-first” no-fault system in 2027. Claims efficiency varies by insurer, so choosing one with a cross-province network is crucial.

Ontario: Private system; highest premiums nationwide (~$2,000/year). Complex liability rules require careful attention in cross-province accidents.

Quebec: Hybrid system; public personal injury coverage and private property insurance are managed separately. Claims for injury and property are independent.

Saskatchewan & Manitoba: Mainly public insurers; claims processes are standardized, but cross-province coordination still goes through the public system.

Key Legal Principles for Cross-Province Claims

1. Accident Location Principle

According to a 2025 Ontario court ruling (Zenith Insurance Company Ltd. v. Chubb Insurance Company of Canada), the province where the accident occurs determines which insurance laws apply. This means:

If an accident happens in Ontario, even if your policy is issued in Alberta, you may be entitled to Ontario accident benefits

Insurers cannot refuse claims citing “policy issued in another province”

2. Priority Rule

When multiple provincial insurers are involved, the priority rule determines which insurer pays first. In Ontario vs. Alberta cross-province accidents, Ontario courts clarified that Ontario priority rules apply if the accident occurs in Ontario.

3. Actual Coverage Principle

The 2025 BC Supreme Court case Courchesne v. Chau established that only actual coverage available can offset claims in cross-province cases. If coverage is denied in one province, it cannot be “assumed” to be approved.

High-Value Summary & Purchase Recommendations

Add-On Combinations for Different Trips:

[Short Provincial Trips]

✔ Basic insurance (mandatory) + Collision + Comprehensive

✘ Rental (optional, budget-dependent)

✘ Roadside Assistance (optional, but recommended)

[Long Cross-Province Trips (2+ Weeks)]

✔ Basic + Collision + Comprehensive (essential)

✔ Rental/Replacement Vehicle (essential for repairs in another province)

✔ Roadside Assistance (highly recommended)

✔ Personal Accident Insurance (based on personal coverage)

[Winter Cross-Province Trips]

✔ All above, plus:

✔ Glass/Tire coverage (for gravel, ice, and snow hazards)

✔ Ensure comprehensive covers hail and storm damage

[Budget-Conscious Travelers]

Prioritize:

1. Collision + Comprehensive (basic coverage)

2. Rental/Replacement (avoids high local rental fees)

3. Roadside Assistance (single tow may exceed annual premium)

Core Principle: Coverage Scope ≠ Low Price

After Ontario’s 2026 insurance reform, many previously mandatory benefits (e.g., income replacement, care coverage) became optional.

Lower premiums may mean less coverage

Before cross-province travel, ensure your coverage is sufficient

Focus on what you can actually access during out-of-province accidents, not just price

Pre-Trip Checklist for Cross-Province Driving

□ Call Your Insurer

Inform your broker/insurance company of your cross-province plan

Confirm policy validity across Canada

Ask whether temporary add-ons are needed

□ Confirm Claims Channels

Record insurer’s 24-hour claims hotline

Save electronic policy on your phone

Check if the insurer supports app-based claims

□ Check Existing Coverage

Confirm rental/replacement coverage

Verify roadside assistance tow distance limit

Understand deductible amounts (adjust before departure if needed)

□ Prepare Emergency Tools

Keep reflective triangles, first aid kit in the car

Keep your phone charged

Prepare a paper copy of insurance information

Practical Tools: Provincial Insurance Regulatory Websites

Ontario – Regulatory Authority: FSRA – Website: [fsrao.ca](https://www.fsrao.ca)

Alberta – Regulatory Authority: Alberta Insurance – Website: [alberta.ca/insurance](https://www.alberta.ca/insurance)

British Columbia (BC) – Regulatory Authority: ICBC – Website: [icbc.com](https://www.icbc.com)

Quebec – Regulatory Authority: AMF – Website: [lautorite.qc.ca](https://www.lautorite.qc.ca)

The insurance market, products, prices, and policies are constantly changing. Before making major insurance decisions, always confirm the latest information with a licensed insurance broker and choose the plan that best suits your personal needs. Safe travels!

References

1. Insurance Bureau of Canada. (2025). Overview of auto insurance in Canada. Retrieved from [https://www.ibc.ca]

2. Rates.ca. (2026). Canadian auto insurance research report. Retrieved from [https://www.rates.ca]

3. Zenith Insurance Company Ltd. v. Chubb Insurance Company of Canada, 2025 ONCA 132 (Ontario Court of Appeal).

4. Courchesne v. Chau, 2025 BCSC 210 (British Columbia Supreme Court).

5. Desjardins Insurance. (2026). Omni App digital claims automation. Retrieved from [https://www.desjardins.com]

6. Government of Canada. (2026). Insurance regulations by province. Retrieved from [https://www.canada.ca]

About the Author

Jonathan Parker is a North American insurance and legal consultant with over 12 years of experience in auto insurance and cross-border claims management. Jonathan has advised private clients, legal firms, and travel agencies on cross-province and international driving insurance, specializing in practical solutions for Canadian and U.S. road travelers.

Editorial Transparency Statement

This article was prepared to provide accurate, up-to-date information regarding Canadian auto insurance and cross-province coverage. All data sources cited are authentic and traceable. The author has no direct affiliation with any insurance company mentioned, ensuring unbiased analysis. Recommendations are based on regulatory frameworks, real case studies, and industry research, with a focus on helping readers make informed decisions for safe and cost-effective cross-province driving.

Disclaimer

The information in this article should not be considered professional insurance, legal, or financial advice. Insurance coverage, exclusions, and eligibility vary widely depending on the provider, jurisdiction, and individual circumstances.

Recommended for you