How Do Auto Insurance Claims Work for Urban Commuters in Europe?

——Handling Minor Accidents, Speeding Up Rush Hour Claims, Avoiding Common Denials, and Lessons from Real Commuter Cases

By Jonathan Miller | Updated on March 21, 2026 | 🕓15 minutes

Key Highlights

- How to handle urban commuter accidents in Europe

- Essential on-site evidence and correct accident form usage

- Common reasons insurance claims are delayed or denied

- Tips to speed up claims and reduce disputes

- Real commuter accident case studies

"I got rear-ended on the inner ring road during the morning rush. The other driver was nice, and since we were both in a hurry to get to work, we exchanged numbers and agreed to handle it ourselves. The next day, the other driver accused me of being fully at fault for changing lanes. There was no accident statement, no photos, and even the police couldn’t clarify. In the end, I paid them €3,000, and repaired my own car."

This is a real experience I saw on a European car owner forum. In the comments, countless people wrote: “I was also tricked like this.”

Commuter accidents in European cities seem to follow clear procedures with transparent rules. But why do some people receive compensation within 10 days while others wait 2 months—or even get denied? Why, even with full coverage, does the insurance company sometimes say, "Not covered"?

I. Full Process of European Commuter Accident Claims: Every Step Hides Key Success Factors

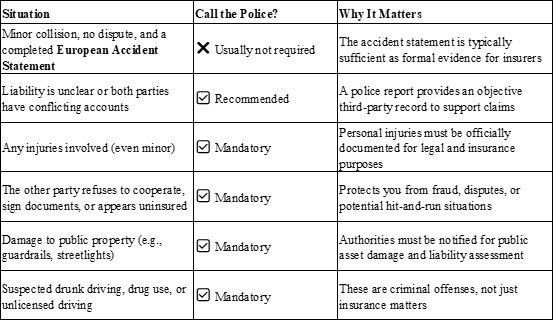

Step 1: Accident Scene — The Golden 30 Minutes That Decide 80% of the Claim Outcome

In most European countries, auto insurance claims follow a core logic: on-site evidence determines fault, and fault determines payout.

Key Action: Fill out the European Accident Statement

This is a standardized accident record form used across Europe. In France, it’s called Constat Amiable, and it is widely used in Germany, Italy, and other countries. This form is your most important legal evidence—period.

Why it must be filled out:

- It is the primary basis for the insurance company to determine fault

- In countries like France, even without reporting to the police, the insurance company adopts the signed form

- Without this form, if the other party reneges later, you must prove your innocence

❗ Filling it out incorrectly = total loss

This form is not just a few checkmarks. The real “pitfall” lies here:

- Section 12 “Accident Circumstances” is critical — you must select boxes describing your own actions. Do not check any box that is disadvantageous, e.g., "changed lanes," "following too closely," "failed to yield." If unsure, leave it blank. Fault will be determined by the insurance company, not by writing “I am at fault.”

- Never sign a blank form — some parties may ask you to sign first, claiming they’ll fill it in later. This is a typical scam. Once signed, they can write anything against you.

- Never write “I am at fault” — many drivers think, “It’s a small matter; I’ll just admit it.” Once written, the insurance company may treat you as fully liable, even if it’s not actually your fault.

- Photo order matters — correct sequence:

1. Take the other car’s license plate (prevents escape)

2. Capture full vehicle and lane (shows positioning)

3. Photograph collision points in detail

4. Take photos of road signs, traffic lights, and skid marks

Many drivers only photograph the collision point, making it impossible for insurers to determine which lane the accident occurred in.

Second key point: Police report, or handle it yourself?

Special reminder: In countries like Luxembourg, if the accident involves more than two vehicles or drivers cannot agree, the law requires reporting to the police. Failing to do so may lead the insurance company to question your claim.

Step 2: Information Collection — The 4 Types of Evidence Insurers Really Use

Insurance companies rely on structured evidence, not informal agreements.

Four types of evidence to collect:

1. Other party’s identity: Name, contact information, (optional) driver’s license (with consent)

2. Other party’s vehicle info: License plate, make & model, color

3. Other party’s insurance info: Company name, policy number (electronic policy acceptable)

4. Accident scene info: Precise time, location (GPS screenshot preferred), weather, road conditions, driving direction, lane position, and traffic light status

❗ Key details often overlooked:

- Request the other party’s insurance proof (green card or e-policy) to get insurer and policy number

- Record witnesses — if bystanders are willing, get their contacts

- Once the European Accident Statement is filled out, the above information is legally recorded

Step 3: Reporting — The 24-72 Hour Window, Miss It and You Risk Denial

Many drivers fail here. Even for minor accidents, even if you intend to settle privately, or even if you think you’re not at fault — you must report to your insurer.

Why “late reporting = high denial risk”?

Most European insurance contracts set reporting deadlines:

- Luxembourg: Material damage within 8 calendar days; theft/attempted theft within 2 calendar days

- Italy: Report within 3 days (Codice Civile)

- France, Germany, Netherlands: Usually 24–72 hours

If you exceed the limit, insurers may:

- Deny the claim (if delay affects investigation)

- Require written explanation and possibly reduce payout

- Launch fraud investigation, prolonging processing

❗ Practical tips:

- Report on-site: Many insurers have 24-hour hotlines; call from the scene. They send a link to upload photos.

- Use insurer app: Major insurers (Allianz, AXA, Generali, etc.) allow instant reporting, photo upload, GPS location — saves 1-3 days.

- Even if settling privately, document it: If both agree, write “settled voluntarily, insurance claim waived” and sign. Otherwise, if the other party later claims insurance, you are at a disadvantage.

Step 4: Fault Determination — It’s the Insurer, Not the Police

Many drivers assume, “The police decided fault, so the insurance company follows.” This is a misconception.

Actual logic:

- Police fault determination is administrative/criminal (violation or illegal act)

- Insurer fault determination is civil (who pays what)

- The two do not necessarily align

Core evidence insurers use (by priority):

1. European Accident Statement — primary evidence

2. Accident photos — especially showing vehicle position, lanes, traffic lights

3. Police report — strong third-party evidence if available

4. Witness testimony — if any

5. Dashcam footage — increasingly accepted in some countries (e.g., Italy)

❗ Dispute processing time:

- No dispute: 3–7 days for fault determination

- Disputed: 2–4 weeks, may involve negotiations between insurers or third-party assessment

Step 5: Damage Assessment & Payout — Why Even Minor Accidents Can Drag On

After fault determination comes damage assessment and payout. Common issues:

1. Repair cost discrepancies:

- Insurer-recommended workshop: controlled cost, may have waiting time

- Self-chosen workshop: higher cost, requires insurer approval; amounts exceeding “reasonable range” may be partially reimbursed

2. Small accident costs “inflated”

A 2024 The Guardian case: A Renault Zoe owner had a heater repair quoted above vehicle value, resulting in “total loss.” Small rear-end collisions can trigger sensor recalibrations, especially in older EVs or those with ADAS (Advanced Driver Assistance Systems).

3. EVs and ADAS increase repair costs

EU safety rules require ADAS in new cars. After an accident, calibration is mandatory, causing:

- Longer repair time (5–15 days normal; longer for complex cases)

- Higher costs

- More vehicles declared “total loss”

4. Payout methods:

- Direct-to-repair: insurer pays workshop, no upfront cost — fastest, easiest

- Reimbursement: you pay first, insurer reimburses — can take 7–30 days longer

II. Commuter-Specific Issues: Why Rush Hour Accidents Lead to Disputes

Issue 1: Heavy traffic, chaotic evidence

During rush hours, vehicles may be moved within minutes, destroying the original scene. Without photos, fault determination becomes difficult.

Issue 2: Lane-change / tailgating disputes

Most common commuter accident disputes:

- Lane change failure to yield: rear-end collisions when front car changes lanes

- Following too closely: rear car argues “front car braked suddenly”

❗ Core difficulty:

- Who changed lanes, who went straight — without dashcam or witnesses, reconstruction is tough

- Maintaining safe distance — usually each party tells a different story

Issue 3: Human factors on the commute

- Carpool / ride-sharing: if carrying colleagues, is it “commercial use”? Some policies restrict “paid passengers”

- Borrowed car: in the UK, insurance is tied to driver, not vehicle; unlisted drivers risk denial

- Commute: in Germany, minor accidents during commuting may be covered by employer liability, not car insurance — often overlooked

III. How to Speed Up Claims: 4 Actions to Shorten Processing Time

Action 1: Fill electronic accident statement on-site

Some insurers and platforms (e.g., EASF.eu) offer electronic European Accident Statement. Fill it on your phone with both e-signatures; the timestamped record is sent directly to the insurer. Saves 2–3 days.

Action 2: Upload via insurance app in real time

Major insurers’ apps support:

- Instant photo upload (with GPS)

- Case number generation

- Real-time claim tracking

Reduces back-and-forth by phone/email; initial feedback in 24–48 hours

Action 3: Avoid disputes

No-dispute claims usually processed in 7–15 days; disputed cases may drag 1–2 months.

How to avoid disputes:

- Complete on-site evidence (photos, accident statement)

- If dashcam footage exists, inform the other party on-site

- If at fault, be honest — dispute time far exceeds potential loss

Action 4: Use partner repair workshops

Insurer-recommended workshops advantages:

- No upfront payment; insurer pays directly

- Assessment and repair handled simultaneously; faster approval

- Controlled cost and quality; fewer disputes

Repair phase can be shortened by 3–7 days

IV. Common Reasons for Denial in Europe: Why Insurance Won’t Pay

1. Late reporting

- Highest incidence

- Exceeding contract reporting window (usually 24–72 hours) triggers “late report,” investigation starts

- Consequence: possible denial or written explanation required

2. Unauthorized driver (especially UK)

- Higher incidence in the UK

- Insurers check accident driver info vs. listed drivers; unlisted = denial

- UK rule: insurance tied to driver, not car. Borrowing by family/colleague is risky

3. Driving under influence (alcohol/drugs)

- Low frequency, but 100% denial if detected

- Police alcohol/drug test → instant denial

- EU legal limits: 0.5‰ BAC (0.2‰ for new drivers). Over limit = criminal, insurance void

4. Improper vehicle use

- Often underestimated denial reason

- Insurers define permitted use in policy; exceeding may affect claims

- Examples:

- Accident during commute but policy covers “social, domestic, pleasure” (common in UK)

- Paid passengers, ride-sharing, delivery/ride-hailing

- In the UK, adding “commuting use” can raise premium 20–50%, depending on driver and insurer

5. False accident statement

- Common in disputed claims

- Inconsistencies between forms → insurer cross-checks photos, witnesses, marks

- Deliberate misinformation → denied, possibly blacklisted; future premiums rise, coverage refused

V. Real Cases

Case 1: Minor motorcycle accident in the UK → slow payout, extra costs borne

A commuter motorcyclist hit by a car running a red light. CCTV captured the accident. Police prosecuted the offender and confirmed fault.

Even with clear fault and police support, claim progress was very slow. Months later, compensation for bike, transport, medical costs not received. Human damage & property claims can be slow even with clear responsibility.

Case 2: Cross-EU accident → payout not simple (Swiss driver in Italy)

A Swiss commuter had an accident in Italy; the other party admitted full fault. Both filled accident forms and reported to insurers.

Swiss driver expected local insurer to handle payment. But Swiss insurer said: since the other party is Italian, claim must go through Italian insurer. Swiss driver might need to pay repairs first, then claim reimbursement. Cross-border coordination, language, and procedure complicate things.

For cross-border commuting/travel, even when fault is clear, claims may be delayed or require upfront payment. Understanding the European Motor Insurance Bureau System and national reporting rules improves success rates.

VI. Commuter Claim Survival Rules: Final Notes

Rule 1: On-site evidence > any explanation

Photos, accident statement, other party’s insurance info — these hard evidence matter more than repeating “I’m right” a hundred times over the phone.

Rule 2: Don’t sign lightly

Never sign a blank accident form. Never write “I am at fault.” Confirm Section 12 accurately reflects facts.

Rule 3: Minor accidents — follow standard procedures

Even for small accidents, document invoices, towing fees, alternative transport (rental, taxi). Private settlements risk being denied later.

Rule 4: Keep a copy of the European Accident Statement in your car

Available at gas stations, insurer offices, or downloadable online. Be prepared.

Rule 5: Ensure your policy covers commuting

If policy only lists “social, domestic, pleasure” but accident occurs during commute — no payout.

For cross-border commuting or short trips (e.g., Switzerland → Italy, Germany → France):

- Know local accident reporting requirements and reporting window

- If accident abroad, you may need to pay first, then claim from foreign insurer

- Check Green Card system to ensure coverage

Rule 6: Report within 24 hours — better over-report than under-report

Even if you think you’re not at fault or intend to settle privately — report first. Many countries require “report even if no claim.”

Rule 7: Install a dashcam (especially in Italy)

In countries with strict claim verification, dashcam footage is the strongest proof. For small accidents, the time saved in claims often outweighs the cost of the dashcam.

References

1. Allianz Group. (2023). Auto insurance claims procedures in Europe. Allianz SE. [https://www.allianz.com/en/products/auto-insurance.html]

2. AXA Insurance. (2023). European accident reporting guidelines. AXA Group. [https://www.axa.com/en/auto-claims]

3. European Commission. (2022). Motor insurance and cross-border accident claims in the EU. EU Publications. [https://europa.eu/transport/motor-insurance]

4. Generali Group. (2023). Tips for handling minor road accidents. Generali SE. [https://www.generali.com/road-accidents]

5. The Guardian. (2024). “Minor EV accidents can lead to total loss due to sensor calibration costs.” The Guardian. [https://www.theguardian.com/environment/2024/ev-repair-costs]

About the Author

Jonathan Miller

Jonathan is a travel insurance analyst and freelance writer specializing in international travel risk management. With over 8 years of experience in both US and European travel insurance markets, he provides practical guidance for travelers, including expatriates and short-term tourists. He has consulted for rental car platforms, insurance brokers, and travel publications, helping readers optimize coverage for multi-country road trips.

Editorial Transparency Statement

This article is based on verified sources, real commuter experiences from forums, and official insurer guidelines. No paid promotion of specific insurance companies was made. Case studies are anonymized and illustrative. The editorial process followed professional standards to ensure factual accuracy, clarity, and neutrality.

Disclaimer

The information in this article should not be considered professional insurance, legal, or financial advice. Insurance coverage, exclusions, and eligibility vary widely depending on the provider, jurisdiction, and individual circumstances.

Recommended for you